- Standard homeowners insurance almost never covers foundation damage caused by settling, soil movement, or natural wear over time.

- Adjusters typically deny these claims citing “earth movement” or “hydrostatic pressure” exclusions.

- Coverage only applies in extremely narrow, specific exceptions, such as sudden structural collapse, damage from a covered event like a massive burst pipe, or specific sinkhole/mine subsidence endorsements.

The Hard Truth About Foundation Claims

Foundation damage is one of the most expensive and stressful repairs a homeowner can face. When cracks appear or floors start to slant, the immediate instinct is to look to your insurance policy for help. I have sat across from homeowners who are holding a $30,000 repair estimate, praying their policy will step in. I always have to deliver the exact same difficult message.

In the vast majority of cases, homeowners insurance does not cover foundation damage. The answer is almost always no.

Understanding why your policy responds this way is crucial. It saves you from the frustration of filing a doomed claim, which goes on your record even if it pays out nothing. Insurers draw a very strict line between sudden accidents and gradual maintenance issues. Because the foundation is literally in the dirt, it is subject to geological forces and time, two things standard property policies intentionally exclude.

I review denied claims every single week. When I see a file labeled ‘foundation crack,’ I already know the denial letter will cite earth movement or settling before I even open the PDF. Adjusters are trained to look for long-term soil issues the moment they step into a basement.

This guide is not here to give you false hope. Instead, I want to walk you through exactly how insurance companies view foundation issues, what specific words they use to deny these claims, and the very narrow exceptions where coverage actually does apply.

The Core Rule: Sudden Events vs. Gradual Wear

To understand why foundation repair is excluded, you have to understand the fundamental premise of property insurance. Homeowners insurance is designed to cover sudden, accidental, and unforeseen events. A tree falling on your roof is sudden. A kitchen fire is accidental.

Foundation damage rarely happens overnight. It is almost always the result of a gradual process. Soil expands and contracts with weather changes over years. Roots slowly push against concrete. Water pressure builds up outside basement walls over decades. Insurance companies classify all of these slow-moving forces as maintenance issues or geological risks, not sudden accidental damage.

Assuming that because the foundation crack appeared suddenly to you, the insurance company will classify it as a sudden event.

Understanding that the adjuster will look at the physical cause of the crack, which is usually years of underlying soil pressure, making it a gradual event in their eyes.

If you want a broader view of how your policy distinguishes between covered perils and excluded events, you should review our complete guide on what homeowners insurance actually covers. That foundational knowledge is critical before you even think about calling your agent.

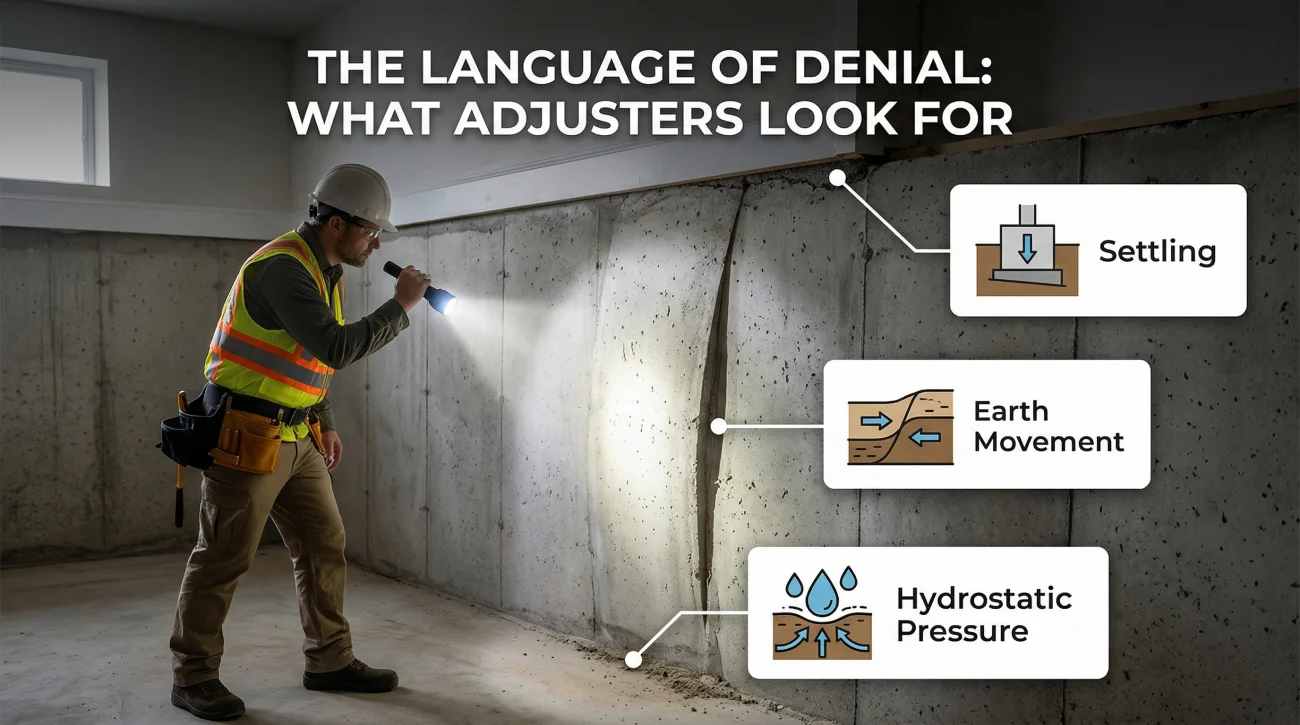

The Specific Language Adjusters Use to Deny Foundation Claims

If you file a claim for a cracked or settling foundation, the insurance company will send an adjuster, and possibly a structural engineer, to inspect your property. They are looking for specific conditions that trigger policy exclusions. Here are the most common reasons you will see printed on a denial letter.

Earth Movement and Settling

Almost every standard policy contains a standard “earth movement” exclusion. This means damage caused by earthquakes, landslides, mudflows, or the normal shifting of the ground is not covered. If your foundation cracks because the dirt beneath it naturally compacted over ten years, the adjuster will cite this exclusion immediately.

Hydrostatic Pressure

This is an industry term you will likely encounter if you have basement walls bowing inward. Hydrostatic pressure happens when the soil outside your foundation becomes saturated with water. The water makes the soil heavy, and it exerts immense, constant pressure against your concrete walls. Because this moisture accumulation happens outside the home and builds up gradually, it falls firmly under policy exclusions.

Tree Root Encroachment

Large trees planted too close to a house will eventually send roots searching for moisture. Those roots can lift concrete slabs and crack basement walls. Insurance companies view landscaping choices and the resulting root growth as a homeowner maintenance responsibility. Damage caused by roots is uniformly denied.

Improper Drainage

If your gutters dump water right next to your foundation, or your yard slopes toward your house instead of away from it, water will pool. Over time, this erodes the supporting soil. If an adjuster notes poor drainage on your property, they will write the report stating that your failure to maintain proper water runoff caused the foundation to fail.

📌 Note: Filing a claim for a normal foundation crack is risky. You will likely receive a swift denial, but the claim itself will still be recorded on your CLUE (Comprehensive Loss Underwriting Exchange) report, which can impact your future insurance rates.

The Narrow Exceptions: When Foundation Damage Might Be Covered

I mentioned that the answer is almost always no. But “almost” leaves room for a few highly specific scenarios. In my operational experience, I have only seen foundation claims paid when the facts align perfectly with one of these strict exceptions.

| Scenario | Insurance Response | Why? |

|---|---|---|

| House slowly settles over 10 years | Denied | Gradual wear, earth movement exclusion. |

| Tree roots crack the concrete slab | Denied | Maintenance issue, preventable by homeowner. |

| Sudden burst pipe washes away soil under slab | Potentially Covered | Direct result of a covered sudden event. |

| Florida home falls into a confirmed sinkhole | Covered (with proper endorsement) | State-specific legal requirement and endorsement. |

| House in historical mining area suffers structural damage | Covered (with proper endorsement) | Mine subsidence endorsement applies. |

Sudden and Accidental Collapse

Some policies offer coverage for “collapse,” but you must read the fine print carefully. In insurance terms, a collapse does not mean a wall is leaning or bowing. It usually means the structure has abruptly fallen down or caved in, rendering the building completely uninhabitable. If a covered peril causes a sudden, catastrophic collapse of a structural component, you may have an avenue for coverage. A slow sag over five years will not trigger this clause.

Direct Result of a Sudden Covered Event

This is the most realistic exception, though still rare. If a sudden, covered event directly causes foundation damage, the policy may respond. For example, if a massive internal plumbing pipe bursts under your concrete slab, and the sheer volume of sudden rushing water aggressively washes away the supporting dirt, causing the slab to crack. In this scenario, the foundation damage is collateral damage from a sudden, covered water event.

The required formula for coverage: Identify the sudden event + Document the immediate structural change + Confirm the adjuster inspects the sequence of events.

Mine Subsidence

If you live in a state with a heavy history of underground coal or clay mining, the ground beneath your home may eventually give way as old mine shafts collapse. Standard homeowners policies strictly exclude this. However, in states like Pennsylvania, Illinois, and Ohio, you can purchase a specific “mine subsidence” policy or endorsement. If you have this coverage and your foundation is damaged by a confirmed mine collapse, the claim is typically covered up to the endorsement’s limit.

Sinkhole Coverage

If you live in Florida, Tennessee, Alabama, Missouri, Kentucky, or Pennsylvania (which carries dual risks for both sinkholes and mine subsidence), sinkholes are a known geological hazard. Standard policies still exclude earth movement, but some states require insurers to offer optional sinkhole coverage or catastrophic ground cover collapse endorsements. If you purchased this specific add-on, and a verified sinkhole swallows part of your property, your foundation damage is covered under those specific terms.

The Basement Flooding Confusion

Many homeowners confuse foundation damage with water damage because the two often happen together. When it rains heavily, and water seeps through the cracks in your basement walls, homeowners often try to file a water damage claim.

This rarely works out the way people hope. Water entering your home through the foundation from the outside is classified as groundwater seepage. Standard policies do not cover groundwater seepage. Furthermore, they do not consider it a flood unless it meets the strict federal definition of a flood event affecting multiple properties.

If you are dealing with water in your basement, the source of the water dictates everything. For a detailed breakdown of how adjusters classify these events, read our guide on whether homeowners insurance covers water damage, which deeply explains the sudden versus gradual rule regarding moisture.

What to Do When You Discover Foundation Issues

Because foundation repair is almost always an out-of-pocket maintenance cost, your first step is usually finding a reputable repair contractor, not calling your insurance agent. Filing a claim for a standard settling crack will likely result in a swift denial while needlessly adding a claim inquiry to your insurance history.

However, if your foundation damage appeared immediately following a sudden, covered event—like an explosion, a major plumbing rupture, or a catastrophic impact—your focus must be on documenting the timeline.

- 📷 Photograph the exact source of the sudden event (e.g., the broken pipe, the impact zone).

- 📏 Photograph the structural damage immediately to prove it occurred simultaneously.

When discussing the issue with the insurance company, the distinction is critical: you are not filing a “foundation claim”—you are filing a claim for a sudden water or impact event that resulted in collateral structural damage. Keeping the focus on the sudden covered event is the only way the coverage question remains open.

Signs Your Foundation Claim Denial May Be Wrong

While most foundation denials are technically correct under the policy language, insurance companies do make mistakes. Sometimes, adjusters default to a standard “earth movement” denial without actually investigating the sequence of events. If you fall into one of the narrow exceptions, you have to be ready to push back.

In my experience, the gap usually comes from the adjuster making assumptions about the timeline without evidence.

Key Point: If a sudden covered event clearly caused your foundation to fail, but the adjuster’s report characterizes the damage as “long-standing wear and tear,” you have a coverage dispute on your hands.

Look out for these specific red flags in your claim process:

- Your foundation was perfectly fine until a major, sudden covered event occurred on your property, but the denial letter ignores that event entirely.

- The insurance company denied the claim based on “improper drainage” without ever sending someone to actually inspect your yard’s grading.

- You live in an area prone to sinkholes, you carry the specific catastrophic ground cover collapse endorsement, but the insurer is trying to classify the event as standard earth settling to avoid paying out.

- The adjuster cited an exclusion in their denial letter that does not actually exist in your specific policy document. If you are unsure how to check this, review our comprehensive list of standard home insurance exclusions.

Foundation damage is a matter of strict coverage interpretation, not just a disagreement over repair prices. If coverage genuinely does not apply, no professional can force the insurer to pay. However, if your damage clearly followed a sudden covered event and the insurer is wrongly applying a gradual maintenance exclusion, you need legal leverage.

If you believe a covered event caused your structural damage and the insurer refuses to acknowledge it, a consultation with a property claim attorney can clarify whether the carrier is misapplying their own contract.

Final Thoughts on Foundation Coverage

Understanding this coverage gap is especially important before you purchase a home. Because standard insurance will not save you from a crumbling foundation, investing in a thorough, independent structural inspection prior to closing is one of the smartest financial decisions you can make.

For current homeowners, it is incredibly frustrating to pay insurance premiums for years only to discover that the very bedrock of your home is not protected. But knowing the reality of foundation exclusions allows you to make better decisions. It stops you from filing unnecessary claims that only serve to raise your rates, and it forces you to prioritize regular home maintenance.

Keep the water away from your house, monitor your large trees, and understand that standard policies protect you from the sudden and unexpected, not the slow passage of time.

❓ FAQ

🏚️ Does homeowners insurance cover foundation repair?

In almost all cases, no. Standard policies exclude foundation damage caused by settling, earth movement, or gradual pressure. It is only covered in very rare exceptions involving a sudden, catastrophic covered event.

💧 Does homeowners insurance cover basement flooding from foundation cracks?

No. Water entering through foundation cracks is classified as groundwater seepage, which is excluded from standard policies. You are responsible for sealing the cracks and managing exterior drainage.

🌳 Will my insurance pay if tree roots ruin my foundation?

No. Insurers consider damage caused by tree roots to be a gradual maintenance issue. Monitoring landscaping and root growth is considered the homeowner’s responsibility.

🌧️ Is a settling foundation covered after heavy rain?

No. Adjusters will categorize this as hydrostatic pressure or earth movement caused by soil saturation. Both are standard exclusions in almost all homeowners policies.

💥 What happens if a burst pipe ruins my foundation?

This is one of the rare exceptions. If a sudden, covered pipe burst washes out the soil and directly causes the foundation to crack, the policy may cover the resulting structural damage.

🕳️ Do I need separate insurance for sinkholes?

Yes. If you live in a high-risk area like Florida, standard policies exclude earth movement. You must purchase a specific sinkhole or catastrophic ground cover collapse endorsement.

⛏️ Does homeowners insurance cover mine subsidence?

Standard policies strictly exclude it. However, if your home is in a state with a history of underground mining (such as Pennsylvania or Illinois), you can purchase a specific mine subsidence endorsement.

🛑 Why did my insurance deny my foundation claim?

The most common reasons are the “earth movement” exclusion, “hydrostatic pressure” exclusion, or the determination that the damage was caused by long-term gradual wear rather than a sudden accident.

🏗️ Does insurance cover a collapsed foundation?

It depends on your policy’s definition of collapse. If the home abruptly caves in due to a covered peril, it might be covered. If it slowly sags or bows over years, it will be denied.

⚖️ Can I fight a foundation claim denial?

You can only fight it successfully if you can prove the adjuster misapplied the policy—for example, if they ignored that a sudden, covered event was the direct cause of the structural failure.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.