- Xactimate is the industry standard software used by insurance adjusters to calculate property damage repair costs.

- The software relies on a regional database of historical average prices, which often lags behind current, real world contractor rates.

- A difference between your insurance offer and your contractor’s quote is usually caused by a “scope gap” (missing repair items) rather than just a “pricing gap”.

- Xactimate estimates frequently undervalue complex items like matching materials, restricted access costs, code upgrades, and contractor overhead.

The Initial Shock of a Low Insurance Estimate

I have sat at countless kitchen tables with homeowners who are staring blankly at a twenty page PDF from their insurance company. The document is filled with cryptic codes, precise measurements, and decimal points. But the only number that really stands out is the total at the bottom. Often, it is thousands of dollars lower than the repair quote their local contractor just handed them.

If you are in this situation, your contractor or adjuster has probably mentioned a specific piece of software. You might be wondering what is Xactimate, and why does it feel like this program is dictating the fate of your home?

When you are navigating the complete home insurance claim process, receiving the initial estimate is a critical turning point. The gap between what your insurer offers and what your contractor demands is not an accident. It is the result of how property damage claims are calculated today.

In my field experience, the biggest source of anxiety for a homeowner is feeling like they have to negotiate with a computer algorithm. But once you understand how the software works, you stop arguing about pennies and start focusing on the actual scope of damage.

This guide is written to help you understand the mechanics of this estimating software, why its numbers almost always come in lower than a real world contractor bid, and what that gap means for your settlement.

What Exactly Is Xactimate?

Xactimate is a specialized software platform used by insurance adjusters, restoration companies, and builders to generate line item estimates for property damage. Think of it as a massive, highly detailed digital catalog for construction repairs.

It was developed by a company called Verisk Analytics and has become the undisputed industry standard. The vast majority of residential property insurance claims in the United States are estimated using this exact system.

How It Breaks Down Your House

Instead of looking at a flooded kitchen and estimating a lump sum of fifteen thousand dollars, Xactimate requires the user to break the room down into granular components. Every single action has a specific code and a corresponding price.

Action Code: WTR (Water Damage)

Item Code: DRY (Drywall)

Activity: Tear out and bag drywall – up to 4 feet

Unit: Square Foot (SF)

Price per Unit: $X.XX

The software calculates the cost of materials, labor, and the equipment needed to perform that specific task based on the dimensions the adjuster entered into the system. It removes emotion and guesswork from the equation, providing a uniform way to calculate costs.

However, this uniformity is exactly where the friction begins. A house is not a standardized product, and repairing a damaged home is rarely as straightforward as clicking a button on a computer screen.

How Xactimate Determines Repair Prices

To understand why your estimate looks the way it does, you have to understand where the software gets its numbers. Xactimate does not pull live prices from your local hardware store, nor does it ask local contractors what they are charging today.

Instead, the software uses a regional price database built on survey data collected from material suppliers and contractors. These prices represent historical median pricing. The software aims for the middle of the road, assuming standard market conditions and standard labor rates for your zip code over the previous months.

It does not account for the fact that the specific contractor you want to hire might have higher overhead, better skilled tradesmen, or a premium service model.

⚠️ Warning: The database represents average historical costs, not a guaranteed price that any specific contractor is legally obligated to accept for your repair project.

Why the Software Estimate Is Usually Lower Than Your Contractor

It is incredibly common to receive an adjuster estimate that falls thousands of dollars short of a professional contractor quote. While many homeowners assume the insurance company is intentionally lowballing them, the discrepancy is often a structural limitation of how the software interacts with reality.

The Time Lag During Demand Spikes

Because the database relies on historical surveys, it cannot instantly react to sudden shifts in the market. In a perfectly stable economy, this lag might only represent a minor difference. But in the real world of property damage, conditions are rarely stable.

If a severe storm hits your city, the demand for shingles skyrockets and local labor rates double overnight because contractors are working overtime. Your local builder has to pay those premium prices today. However, the software will not reflect those post storm price spikes until weeks or months later.

| Factor | Contractor Reality | Software Assumption |

|---|---|---|

| Material Costs | Based on today’s invoice from the supplier. | Based on a monthly regional average. |

| Labor Rates | Based on availability and current demand. | Based on standard historical wages. |

| Job Timeline | Accounts for current supply chain delays. | Assumes materials are readily available. |

Contractors price a job based on the actual risks and costs of doing the work right now. The software prices a job in a sterile environment where materials are perfectly accessible and laborers work at average speeds. This disconnect between a sterile software environment and the messy reality of construction creates two distinct types of discrepancies in your paperwork.

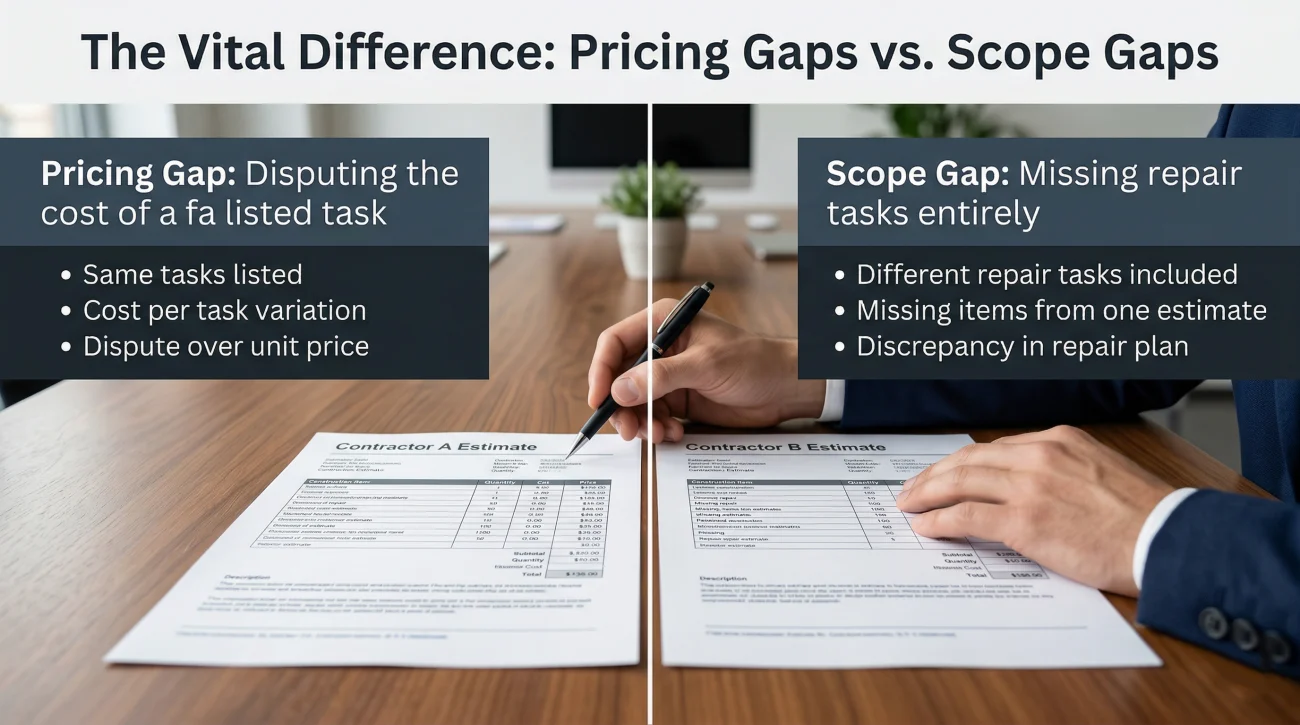

The Vital Difference: Pricing Gaps vs. Scope Gaps

When reviewing your documents, the most important diagnostic step you can take is determining why the numbers are different. In my experience reviewing claims, homeowners waste weeks arguing about the wrong thing.

The difference between your insurance offer and your contractor’s quote almost always comes down to two distinct categories: a pricing gap or a scope gap.

Both estimates list the exact same repair task, but they attach a different dollar value to it. For example, the software says painting the wall costs $300, and your contractor says it costs $450.

The contractor’s estimate includes repair tasks that the software estimate completely ignores. For example, your contractor includes replacing the soaked subfloor, but the adjuster’s estimate only pays for the top layer of flooring.

Many people get hyper focused on arguing over the price per square foot of drywall. This is usually a losing battle. Insurance companies are highly resistant to changing the unit prices generated by their software because doing so undermines their entire system.

Scope gaps are where the real discrepancies lie. A software estimate is only as good as the information the adjuster inputs. If the adjuster failed to notice that the water wicked up the walls, they will not input the line items for drywall removal, insulation replacement, and anti microbial treatments. Those line items are simply missing.

If you suspect major items have been left out of your paperwork entirely, you are dealing with a scope issue. You can learn more about diagnosing this in our guide explaining why a home insurance claim estimate is too low.

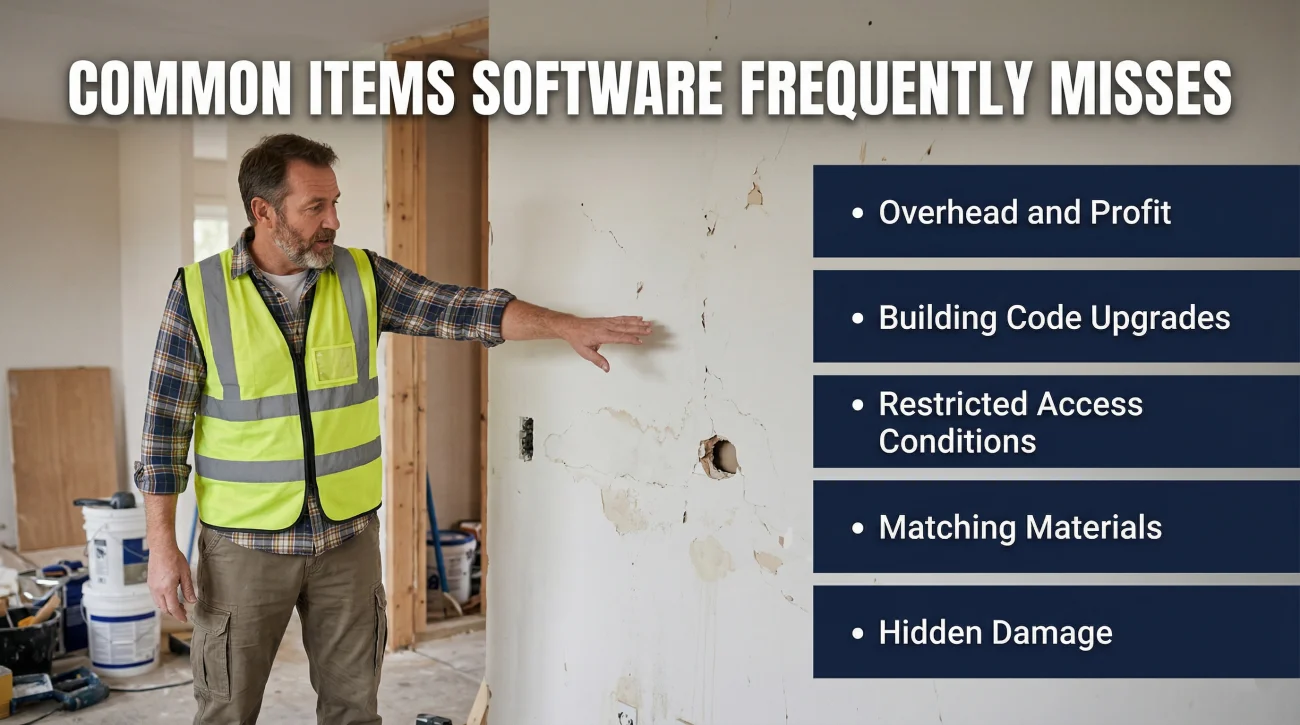

Common Items the Software Frequently Misses or Undervalues

Because the software relies on the user to manually select every necessary repair step, items that require on site judgment are frequently overlooked. Here are the most common areas where software estimates fall short of reality.

Overhead and Profit (O&P)

General contractors do not work for free. They charge for the time it takes to coordinate plumbers, electricians, and carpenters. This coordination fee is standard in the construction industry and is known as Overhead and Profit. Often, an adjuster will generate an estimate that completely omits O&P line items, assuming the homeowner will act as their own project manager.

Building Code Upgrades

If your house is older, the way it was originally built may no longer meet current city ordinances. If a fire destroys a room, your contractor must rebuild it to modern electrical and structural codes. Adjusters frequently omit these required upgrades from their initial software scopes. Whether your specific policy provides financial coverage for code upgrades is a separate issue, but from a pure estimating standpoint, leaving these real contractor costs out of the software creates an immediate scope gap.

Restricted Access Conditions

The standard line item for removing debris assumes the worker can easily toss materials into a dumpster parked in the driveway. But what if your home is on a steep hill, or you live on the fourth floor of a condominium? Contractors charge extra for restricted access because it takes more labor hours. The software often defaults to standard, easy access conditions.

I regularly see adjusters use standard debris removal codes for third floor condos with no elevator. A contractor has to pay laborers to carry tear out materials down three flights of stairs by hand, but the software assumes a dumpster is sitting right outside the window.

Matching and Continuous Surfaces

If water ruins three feet of your custom hardwood floors, the software might only generate a price to replace those three feet. In reality, a contractor cannot buy a patch of discontinued flooring that perfectly matches the sun faded finish of your existing room. The scope often needs to include replacing the entire continuous floor to return your home to its pre loss condition.

Hidden and Underlying Damage

Estimates are generated based on a visual inspection. The adjuster enters what they can see. They cannot see the mold growing behind the cabinets, the rusted pipe fittings inside the wall, or the damaged decking beneath the roof shingles. These hidden items will not exist in the software output until a contractor performs selective demolition and documents them.

Signs Your Settlement Was Built on an Incomplete Xactimate Scope

All of the gaps described above share a common result: a settlement offer that does not cover the actual cost of repairs. The confusion usually peaks when you realize your claim might be stalling because the paperwork does not reflect the reality of the damage.

Here are common red flags that the software estimate you received is fundamentally incomplete:

- Your contractor’s quote is significantly higher, and the gap is spread across entire rooms, not just a disagreement over the price of a single material.

- You notice standard overhead and profit percentages are entirely absent from the final pages of the insurer’s document.

- Your contractor identified complex structural damage, but the insurer’s estimate reads like a generic painting and patching invoice.

- Your contractor has stopped work because they are refusing to accept the insurer’s pricing for specialized labor.

When you encounter these roadblocks, the solution is rarely to complain about the software itself. The software is just a tool. The problem is that the tool was not used to build a complete picture of your loss.

Bridging the Gap Professionally

Knowing what this estimating platform is helps explain why the numbers look different, but it does not fix your settlement. This is where professional representation changes the dynamic.

A licensed public adjuster uses the exact same software as the insurance company. They speak the same language, use the same codes, and understand exactly how to input restricted access, code upgrades, and continuous matching requirements into the system. Instead of you trying to explain construction realities to a desk adjuster, consider getting a free claim review from a licensed public adjuster to accurately rebuild your scope within the platform the insurer trusts.

Final Thoughts on Navigating Software Estimates

The introduction of standardized estimating software changed the insurance industry forever. It brought speed and consistency to a chaotic process. However, it also created a system where the unique, messy realities of a damaged home are forced into rigid digital boxes.

💡 Pro Tip: Never assume the first document you receive from your insurer is the final answer. It is merely the opening offer based on a visual inspection and median pricing data.

The goal is not to beat the software at its own game. The goal is to ensure the software is fed the correct, complete data about your loss. When every necessary repair step is accurately coded into the system, the resulting settlement will reflect the true cost of restoring your home.

❓ FAQ

🤖 What exactly is Xactimate?

It is the industry standard software used by most property insurance companies to calculate the cost of repairs for a claim, breaking down every task into specific line items for materials and labor.

💻 Can I download the software to write my own estimate?

While you can theoretically purchase a subscription, the software is highly complex, expensive, and designed for industry professionals. It is generally not practical or cost effective for a homeowner to use it for a single claim.

📉 Why is the insurance estimate so much lower than my contractor’s quote?

The software relies on historical average pricing that often lags behind current market rates. Additionally, adjusters frequently omit complex line items (a scope gap) that your contractor knows are necessary to complete the job.

📝 Do all insurance companies use this specific software?

Not all, but most major property insurance carriers in the United States use it or a very similar competitor platform to standardize their claims processing.

🔄 How often does the software update its material prices?

The pricing database is typically updated monthly for different geographic regions. However, this means it cannot instantly react to sudden price spikes caused by severe local weather events or supply chain issues.

🏗️ Does the software automatically include contractor overhead and profit?

No. Overhead and Profit (O&P) must be manually applied by the person writing the estimate. Adjusters frequently leave this setting off unless the homeowner or their representative specifically demands it.

⚖️ Is the software estimate legally binding for my final settlement?

No, the initial software estimate is just the insurance company’s opening assessment of the damage. It is a negotiable document, especially if you can prove that necessary repair steps were left out.

🗣️ How do I argue with a computerized estimate?

Focus on finding the missing repair tasks (the scope gaps) and providing contractor documentation that proves those steps are required, rather than disputing the database’s unit prices.

🕵️♀️ What does a scope gap mean in an insurance claim?

A scope gap means the adjuster’s estimate completely missed or ignored a category of damage that actually exists, such as water behind a wall or necessary building code upgrades.

📄 Can my contractor submit their own line item estimate?

Yes. Experienced contractors often use the same software to write their own detailed estimate, which they then submit to the insurance company as a supplement to request additional funds.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.