- Filing a claim and submitting a proof of loss are two completely different steps in the insurance process.

- A proof of loss is a formal, sworn statement detailing the exact amount you are claiming and the evidence supporting it.

- Not every claim requires this form, but if your insurer requests it, it becomes a mandatory procedural hurdle.

- The 60-day clock starts when the insurer requests the form, not when the damage occurred.

- Missing the deadline can result in a complete claim denial.

- A missing signature or an absent notary stamp is the most common reason these forms are immediately rejected on a technicality.

The Formal Document That Catches Homeowners Off Guard

In my years of reviewing property claims from both sides of the desk, I have seen thousands of homeowners breathe a sigh of relief right after they make their initial claim phone call. They assume the heavy lifting is done. They think the adjuster will show up, write an estimate, and mail a check. Then, a few weeks into the process, a formal letter arrives demanding a “Sworn Statement in Proof of Loss.” Panic usually sets in immediately.

If you are reading this, you likely just received one of these requests. The language is intimidating, the form looks like a legal affidavit, and there is usually a strict deadline attached to it. As a claims writer, I want to clarify right away that receiving this request does not mean you are in trouble or that your insurer suspects fraud. It is simply a highly rigid procedural step that shifts the burden of proof from the adjuster’s desk back to yours.

Understanding what this document is, why insurance companies use it, and how to fill it out without making critical errors is vital. A simple missed signature or a misunderstood deadline on this single piece of paper can derail months of hard work on your claim.

What Is a Proof of Loss (And How It Differs From Your Initial Claim)

The most common mistake I see homeowners make is confusing the act of filing a claim with the act of proving a loss. To protect your claim position, you need to treat these as two entirely separate events.

When you first call your insurance company after a tree falls on your roof or a pipe bursts, you are simply notifying them that a covered peril has occurred. You are opening the file. If you are unsure about the initial steps of opening a file, you can review our guide on the correct way to file a home insurance claim. That initial notification is just the beginning.

The proof of loss form is a formal, legally binding document submitted later in the process. It is your official declaration to the insurance company stating exactly what was damaged, how it was damaged, and the precise dollar amount you are claiming to fix it. While the initial phone call says “I have damage,” the proof of loss says “Under penalty of perjury, here is the exact financial scope of my damage.”

I recently reviewed a file where a homeowner thought their contractor’s repair estimate served as their proof of loss. They emailed the PDF to the adjuster and considered the matter closed. Forty days later, they received a warning letter that their claim was at risk of denial because the official sworn form had never been returned. A contractor’s estimate is supporting evidence, but it never replaces the formal sworn statement.

When and Why Insurers Request It

You might be wondering why your neighbor never had to fill out one of these forms for their minor fence repair. The truth is, insurers do not request a formal proof of loss for every single claim. For minor, straightforward damage, the adjuster’s inspection and estimate are often enough to trigger a settlement.

Insurers typically trigger the proof of loss requirement in specific scenarios where the financial stakes are high or the details are complicated. For instance, if your kitchen suffers minor water damage and the adjuster agrees with your plumber’s $3,000 estimate on the spot, you probably will not see this form. However, if a hurricane rips off half your roof and causes $80,000 in interior damage, involving multiple contractors and a dispute over code upgrades, the insurer will almost certainly demand a sworn proof of loss to lock in your official demand before issuing a major check.

Adjusters will also send the form if they feel the negotiation is dragging out and they want to force the homeowner to commit to a final number. To see where this document fits into the broader timeline of your recovery, I recommend mapping out how home insurance claims actually work from start to finish. Once you receive the request letter, knowing exactly what to put on the page becomes your primary focus.

What You Must Include in the Form

When the form arrives, it usually consists of one or two pages with several blank fields. Leaving any applicable field blank gives the insurer an easy procedural reason to reject it. While policies vary, standard forms generally require the same core information.

- The Date and Cause of Loss: You must state exactly when the damage occurred and what caused it. Be factual and brief.

- Your Interest in the Property: This confirms you are the owner and lists any mortgage companies or lienholders who also have a financial interest in the house.

- The Claimed Amount: This is the most critical line. You must state the specific dollar amount you are demanding from the insurance company to make you whole.

- Supporting Documentation: The form itself is just a summary page. It must be backed up by evidence, which usually includes contractor estimates, inventory sheets, mitigation invoices, and photographs.

💡 Pro Tip: Never guess the numbers just to get the paperwork off your desk. Knowing exactly what evidence to gather beforehand is crucial, which is why following a strict home insurance claim documentation checklist from day one makes filling out this form much easier.

Even if you gather every perfect piece of evidence and calculate your demand down to the penny, the form can still be rejected if you miss one critical step at the very bottom of the page.

The Sworn Statement and Notarization Trap

One of the most frequent points of failure I witness happens right on the signature line. A proof of loss is not just a standard form you sign like a delivery receipt. It is a sworn statement.

Most standard property insurance policies explicitly require the proof of loss to be signed under oath and notarized. This means you must sign the document in the physical presence of a licensed notary public who stamps it to verify your identity and your oath.

If you mail in a perfectly calculated, fully documented proof of loss but forget to have it notarized, the insurer will reject it. They will reject it simply because the document is technically defective, forcing you to start the submission process over and burning valuable time on the clock.

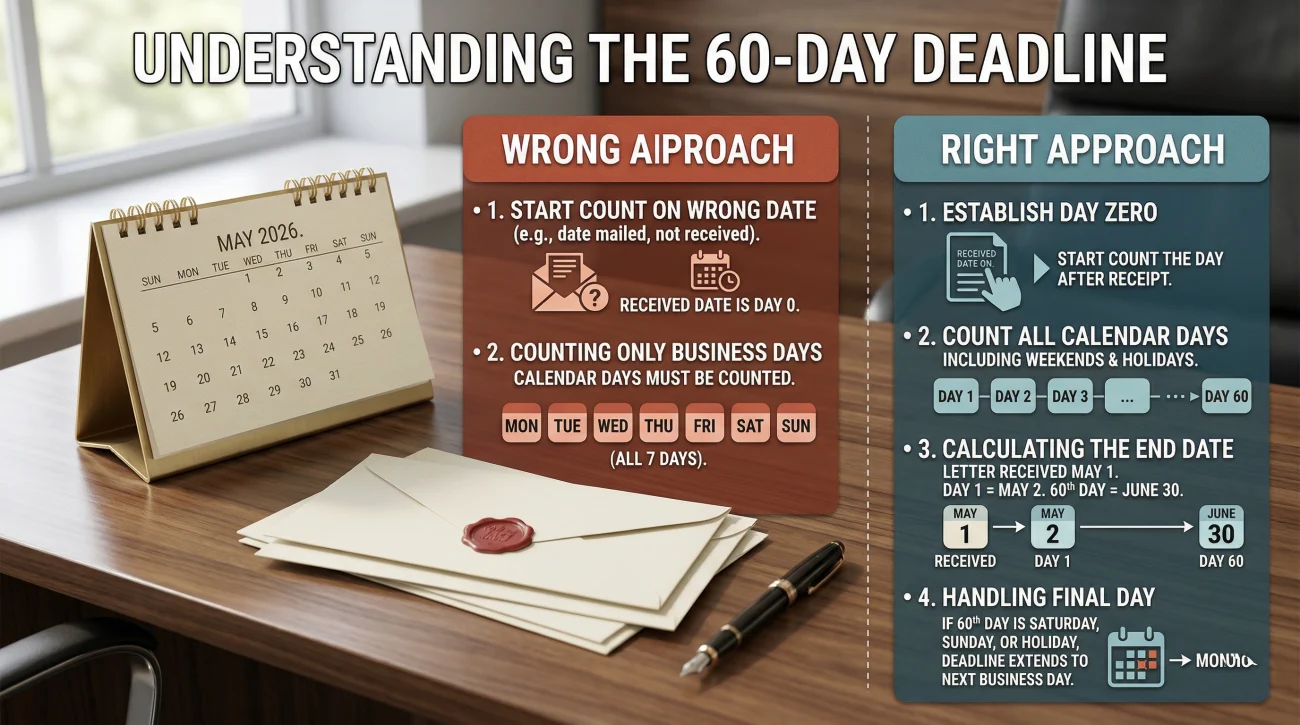

Understanding the 60-Day Deadline Mechanics

If there is one thing you take away from this guide, let it be how the deadline clock works. Almost all standard policies require you to return the completed, signed, and notarized proof of loss within 60 days. But 60 days from when?

Believing you have 60 days from the date the storm hit your house to submit all your final paperwork.

Understanding that the 60-day clock typically starts ticking on the exact day the insurance company formally requests the proof of loss and provides you with the blank form.

Check your specific policy documents to confirm your timeline, but the “60 days from request” rule is the industry standard. This deadline is rigid. If you miss it, the insurer can close your file and deny your claim entirely for non-compliance, regardless of how severe your property damage is.

How to Request an Extension

Often, 60 days is simply not enough time to get multiple contractor bids, complete a massive personal property inventory, and coordinate with specialists. If the deadline is two weeks away and you are still waiting on your roofer’s final Xactimate report, you must ask for an extension in writing before the clock runs out.

Dear [Adjuster Name],

I am writing regarding the Proof of Loss form requested on [Date]. We are diligently working to gather all required documentation, but we are still awaiting finalized scope estimates from our independent contractors due to current local scheduling delays.

To ensure we provide a complete and accurate sworn statement, I am formally requesting a 30-day extension to the Proof of Loss deadline, moving the due date to [New Date]. Please confirm your approval of this extension in writing by [Date].

Thank you,

[Your Name]

Never rely on a verbal “don’t worry about it” from an adjuster over the phone. If the extension is not granted in writing, assume the original deadline still stands.

Common Reasons for Form Rejection

When an insurer rejects a proof of loss, they must tell you exactly why it is deficient. Rejections usually fall into two categories: procedural errors or dispute of scope. Procedural errors are entirely preventable.

| Error Type | What Happens in the Real World |

|---|---|

| Missing Notary Stamp | Form is returned immediately as defective. You must reprint, resign in front of a notary, and resubmit. |

| Vague “To Be Determined” Amounts | Writing “TBD” on the total amount line invalidates the form. Insurers require a firm dollar demand. |

| Lack of Supporting Evidence | Demanding $40,000 without attaching the corresponding contractor estimates causes rejection for lack of proof. |

| Incorrect Policy Limits | Claiming an amount that exceeds your stated coverage limits on your declarations page. |

Keep in mind that repeated rejections for minor technicalities can sometimes be a strategy to exhaust the homeowner. If you find your forms being returned over and over for moving goalposts, you might be facing intentional stalling. Recognizing these patterns early is crucial, which is why I advise homeowners to familiarize themselves with common home insurance claim adjuster tactics.

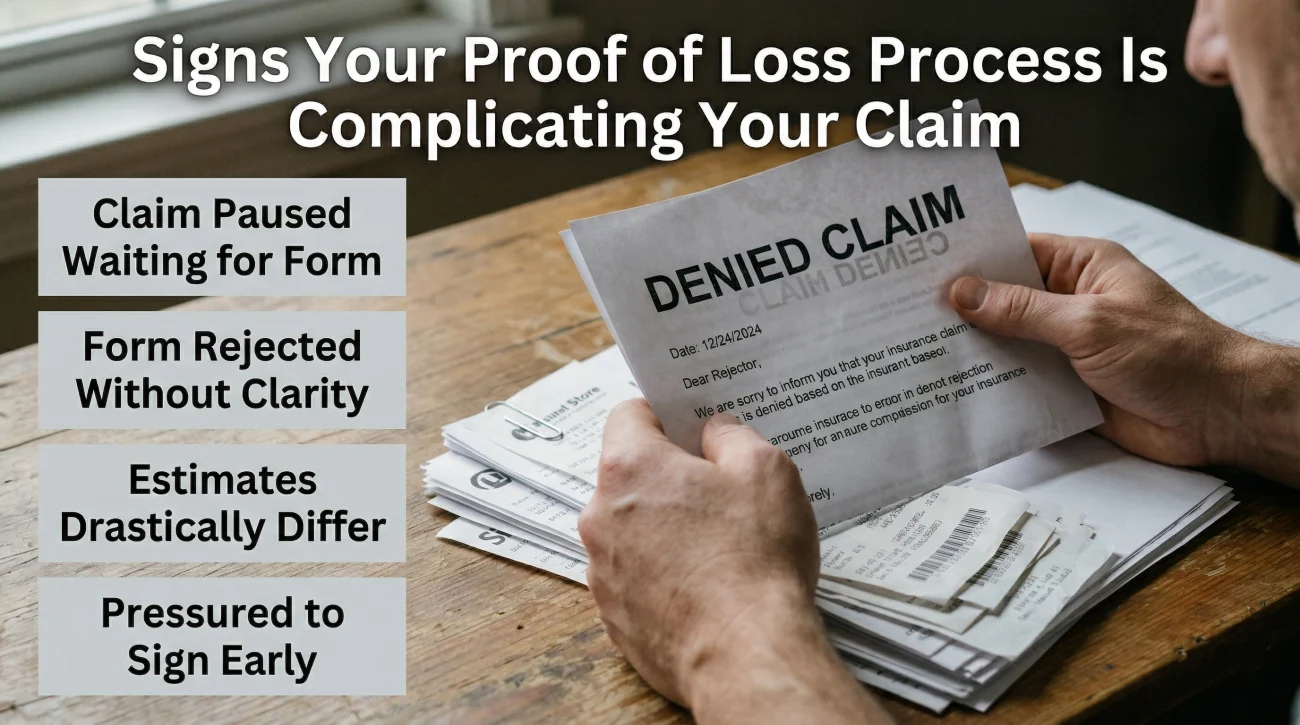

Signs Your Proof of Loss Process Is Complicating Your Claim

Procedural requirements like this one are where claims frequently stall or fall apart entirely. If you are experiencing any of the following situations, the paperwork phase has crossed over into a claim risk:

- You submitted hundreds of photos and receipts, but the adjuster just told you your claim is paused because a formal proof of loss was never received.

- Your form was rejected by the desk adjuster, but their letter did not clearly explain what was deficient or how to fix it.

- The 60-day deadline is approaching, and your insurance company’s estimate is thousands of dollars lower than your contractor’s quote, leaving you unsure of which number to swear to.

- You felt pressured to sign the form early to get an advance payment, listing an amount that you now know does not cover the hidden damage your contractor just found.

These situations create a tremendous amount of anxiety. The most dangerous scenario is when a homeowner signs a form for a low amount simply because they feel they lack the evidence to ask for more. If your contractor’s number is drastically different from the insurer’s number, you are facing a scope gap. Understanding why this happens is the first step to fixing it, which we cover in detail in our guide on what it means when your claim estimate is too low.

The Final Step Before You Sign

The dollar amount you list on your proof of loss form is your formal, legal claim position. Because it is a sworn statement, you must be absolutely confident in your numbers before signing.

You do not have to navigate this final hurdle alone. If the deadline is looming and you are unsure if your documentation fully captures your policy entitlements, getting professional eyes on the file changes the dynamic. You can arrange a free claim review from a licensed public adjuster to ensure your scope is accurate before you sign any sworn statement.

❓ FAQ

📝 What exactly is a proof of loss form?

It is a formal, legally binding document requested by your insurance company where you swear under oath to the exact details and dollar amount of the damage you are claiming.

⏳ What is the deadline to submit the proof of loss, and when does it start?

While some policies differ, the industry standard gives you 60 days to submit the completed form. Crucially, this countdown almost always begins on the day the insurance company formally requests the document, not the date your property was damaged.

📋 Do I need to include a personal property inventory with the form?

If your claim involves damaged belongings, yes. You will typically need to attach a detailed room-by-room inventory sheet as supporting documentation for the total amount claimed.

📑 Does my proof of loss have to be notarized?

Yes, in the vast majority of cases. Because it acts as an affidavit, insurers typically require a licensed notary public to witness your signature and stamp the document.

💵 What dollar amount do I put on the form?

You should list the total exact amount it will cost to repair or replace your damaged property, backed up by independent contractor estimates, inventory lists, and material quotes.

❌ Can my insurance company reject my proof of loss?

Yes. They frequently reject forms for procedural errors such as missing a notary stamp, leaving required fields blank, or failing to attach the required supporting documentation.

If your policy requires a proof of loss but the adjuster hasn’t sent one, you should formally request the blank document in writing via email to protect your timeline.

🛑 What happens if I miss the deadline?

Missing the strict submission deadline is considered a breach of your policy conditions and gives the insurance company strong procedural grounds to delay or completely deny your claim.

✍️ Can I ask for an extension if I need more time?

Yes, you can request an extension if you are still waiting on contractor estimates. However, you must ask for it before the original deadline expires and secure the approval in writing.

🏗️ Is the contractor’s estimate the same as a proof of loss?

No. A contractor’s estimate is the supporting evidence used to justify your numbers. The proof of loss is the official legal form that summarizes your demand to the insurer.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.