- Insurance adjusters are trained professionals representing the financial interests of the insurance company, not your personal financial interests.

- Common claim tactics include offering extremely fast (but low) settlements, strategically delaying communication to wear you down, and using recorded statements to frame facts favorably for the insurer.

- Adjusters often minimize scope by only documenting surface-level, visible damage while ignoring underlying structural issues.

- Understanding the psychology behind these strategies is the first step; however, countering them effectively usually requires having your own professional representation to match their expertise and force a fair evaluation.

Recognizing the Game When You Are in the Middle of It

If you are reading this, chances are you are in the middle of a property damage claim, and something feels slightly off. Maybe the adjuster was surprisingly quick to offer a check, or perhaps your emails are suddenly going unanswered. You might be searching for “home insurance claim adjuster secret tactics” because you want validation that you are not just being paranoid.

I can tell you right now: you are not being paranoid. I have sat across from insurance adjusters on hundreds of claims, reviewing their scope documents, their line-item estimates, and their denial letters. The experience of feeling like the process is subtly working against you is extremely common.

However, I want to reframe how we look at this. In my experience, these are rarely “evil” tactics executed by malicious people. Adjusters are simply corporate employees executing a highly optimized business process. Their job is to settle claims quickly and mitigate the financial loss for the insurance company. The strategies they use are rooted in human psychology and standardized training.

In this guide, I will walk you through exactly what these strategies look like in the real world, why they are so effective against everyday homeowners, and how recognizing the pattern changes the entire dynamic of your claim.

Key Point: You do not need to learn how to aggressively fight an adjuster. You simply need to recognize when a standard industry tactic is being applied to your file, so you can make informed decisions about when to escalate the matter to a professional.

The Fundamental Reality: Who Does the Adjuster Actually Work For?

Before we look at specific behaviors, we have to establish the baseline dynamic of an insurance claim. When a pipe bursts or a tree falls on your roof, the insurance company sends an adjuster to evaluate the damage. Because they are wearing a polo shirt with the insurance company’s logo and acting polite, many homeowners unconsciously assume this person is there to act as their personal advocate.

This is the first and most critical misunderstanding in the claims process. The adjuster works for the carrier. Their performance metrics, their training, and their ongoing employment rely on their ability to enforce policy limits, apply depreciation accurately, and prevent overpayment.

There are generally two types of adjusters the company might send: “staff adjusters” (direct employees of the insurance company) and “independent adjusters” (contractors hired by the insurance company during busy periods). Despite the name, independent adjusters are still paid by the insurance carrier. If you want to understand the exact differences in how the different types of adjusters operate and who signs their paychecks, it is vital to know that neither of these professionals represents your financial interests.

Once you accept that this is a business negotiation rather than a customer service interaction, the tactics they use start to make perfect logical sense.

The Critical Window Before the Adjuster Arrives

Before we even look at the tactics used during the settlement phase, I need to talk about the time between filing your claim and the moment the adjuster knocks on your door. This window is where many homeowners unknowingly compromise their own payout.

I always tell my clients that the adjuster is assessing the scene exactly as it looks when they arrive. If you have cleaned up the water, thrown away the burst pipe, or let a contractor tear out the wet drywall without taking extensive photos first, you have just made the adjuster’s job much easier. They can only pay for what they can prove is damaged.

Taking aggressive, detailed photographs of the damage immediately after it happens is the single best defense against the scope minimization tactics we are about to discuss.

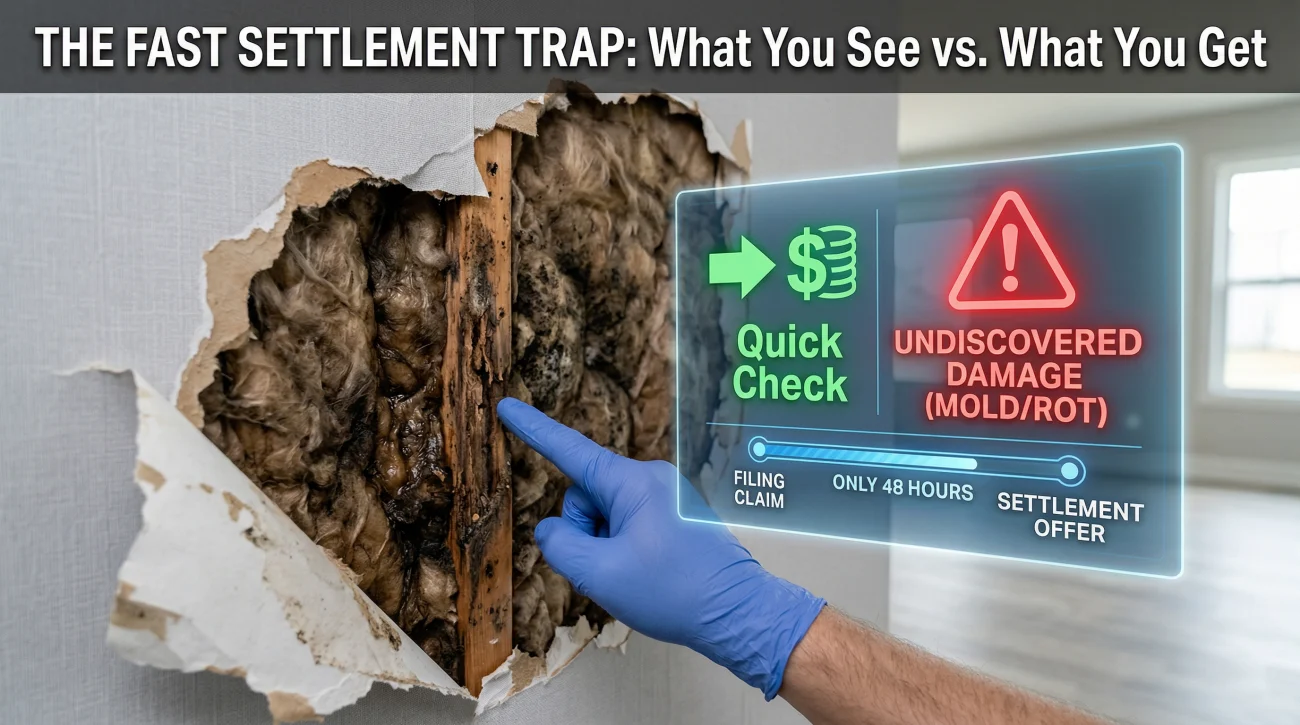

Tactic 1: The “Fast but Final” Settlement Offer

One of the most effective ways an insurance company minimizes a claim is through speed. You file a claim for significant water damage. The adjuster arrives the next day, spends 45 minutes walking through your house with an iPad, and within 48 hours, you have a settlement offer and a check in your hand.

To a stressed homeowner whose living room is currently torn apart, this feels like incredible customer service. In reality, the “fast settlement” is a well-known method of limiting the scope of loss.

When I review files where homeowners feel they were severely underpaid, the pattern is remarkably consistent: the adjuster wrote an estimate on the spot and issued payment before any walls were opened up or any independent contractors had assessed the hidden damage.

Why this tactic works psychologically:

Homeowners want resolution. The disruption of property damage causes immense anxiety, and a check represents a path back to normalcy. Adjusters know that undiscovered damage (like moisture trapped in a subfloor or smoke behind drywall) gets exponentially more expensive to fix over time. By putting money in your hand before an independent contractor can look beneath the surface, the adjuster effectively closes the psychological loop. Once you accept the money and start minor repairs, reopening the claim for unseen damages becomes a steep uphill battle.

Warning: Accepting a fast check does not always legally close your claim, but it creates immense operational friction if you need to ask for more money later, as the carrier will argue you already agreed to the initial scope of repairs.

Tactic 2: Strategic Delays and “Information Fatigue”

The exact opposite of the fast offer is the strategic delay. I typically see this tactic deployed when a claim is exceptionally large, or when a homeowner starts pushing back against a low initial estimate.

You might experience this as a sudden drop in communication. Your emails go unanswered for a week. When the adjuster finally replies, they do not answer your question; instead, they request a document you have already submitted. Then, your file gets randomly reassigned to a “desk adjuster” in another state who needs to “get up to speed” on your claim.

Why this tactic works psychologically:

This relies on “information fatigue” and financial pressure. As weeks turn into months, your temporary repairs might be failing, or you might be floating the cost of a hotel on your own credit cards. Financial pressure increases the likelihood that you will eventually accept a lowball offer just to make the ordeal end. For context on what a normal timeline looks like, you should review the entire lifecycle of a standard claim process so you know when a delay is legitimate versus intentional.

Sample Documentation Note for Delays:

If you are caught in this cycle, do not express anger on the phone. Document it neutrally via email.

Tactic 3: The Recorded Statement Trap

Shortly after you file a claim, the desk adjuster may call you and casually ask, “Do you mind if I record this conversation just for our files so I get the details right?”

In my experience, this is rarely about getting the details right for your benefit. The recorded statement is an evidence-gathering expedition. The adjuster is trained to listen for specific keywords and phrasing that can trigger policy exclusions. They are not trying to catch you in a lie; they are trying to frame the facts of the loss in a way that minimizes the carrier’s liability.

For example, if you say, “The roof has been leaking a little bit for a while, but this storm really opened it up,” the adjuster will likely highlight the phrase “for a while.” This single conversational misstep can trigger a denial based on “deferred maintenance,” which is a standard exclusion in almost all policies.

If you want to protect your claim, knowing exactly what phrases to avoid saying during an adjuster inspection is critical before you ever pick up the phone.

Why this tactic works psychologically:

We are socially conditioned to be helpful and conversational. When someone asks a casual question, we tend to fill the silence, sometimes guessing or estimating details we are not entirely sure about. The adjuster leverages this natural conversational rhythm to get you on the record making assumptions that benefit their denial guidelines.

Answering conversational, open-ended questions with speculation. (“I think the pipe might have been rusty for years.”)

Sticking strictly to the chronological facts of the sudden event. (“I walked into the kitchen at 8 AM and saw water actively flowing from the cabinet.”)

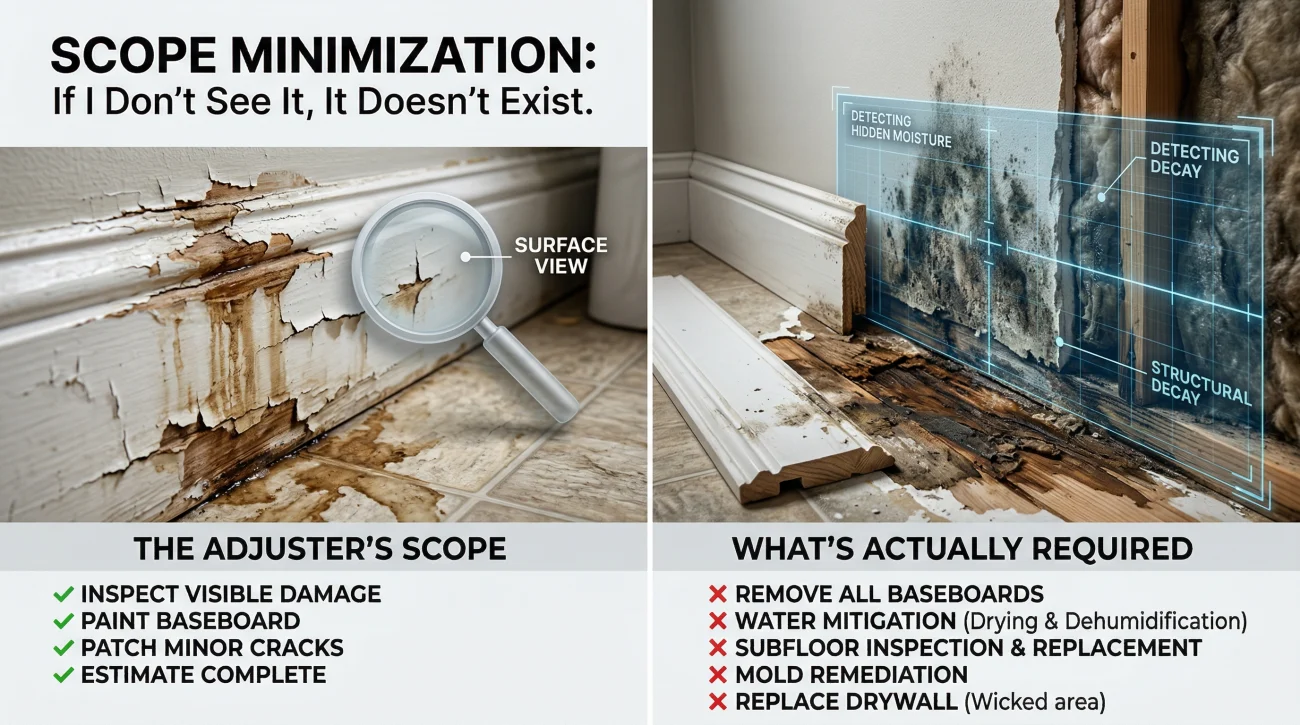

Tactic 4: Scope Minimization (The “If I Don’t See It, It Doesn’t Exist” Rule)

The “scope of loss” is the master document that dictates your payout. It lists every piece of baseboard, every gallon of paint, and every hour of labor required to fix your home.

When I walk a property with an insurance scope in hand, the most pervasive tactic I see is scope minimization. Adjusters are generally trained to document only what is visibly, immediately damaged on the surface at the time of their inspection. They are not going to lift your carpets to check the subfloor. They are not going to pull off baseboards to check for water wicking into the drywall. They are not going to climb into a cramped attic to trace a roof leak to its origin.

If the damage is not documented in the scope, it will not be paid for in the settlement. Period.

Why this works psychologically:

I find that most homeowners do not know how to read an Xactimate estimate (the software adjusters use). They see a 15-page document filled with line items and assume it is comprehensive because it looks highly detailed. They do not realize what is missing until their contractor starts the work and halts production because there is no budget for the concealed issues.

| Damage Type | What the Adjuster Typically Scopes | What is Actually Required (Often Omitted) |

|---|---|---|

| Water Leak in Kitchen | Replacing visible wet flooring and painting the baseboards. | Moisture mitigation, drying equipment, replacing ruined subfloor, addressing lower-cabinet damage. |

| Kitchen Fire | Replacing burned cabinets and cleaning the immediate area. | HVAC duct cleaning for soot, sealing walls to prevent smoke odor, structural testing. |

| Wind / Roof Damage | Patching the missing shingles. | Replacing underlayment, matching shingle dye lots, addressing water intrusion in the attic. |

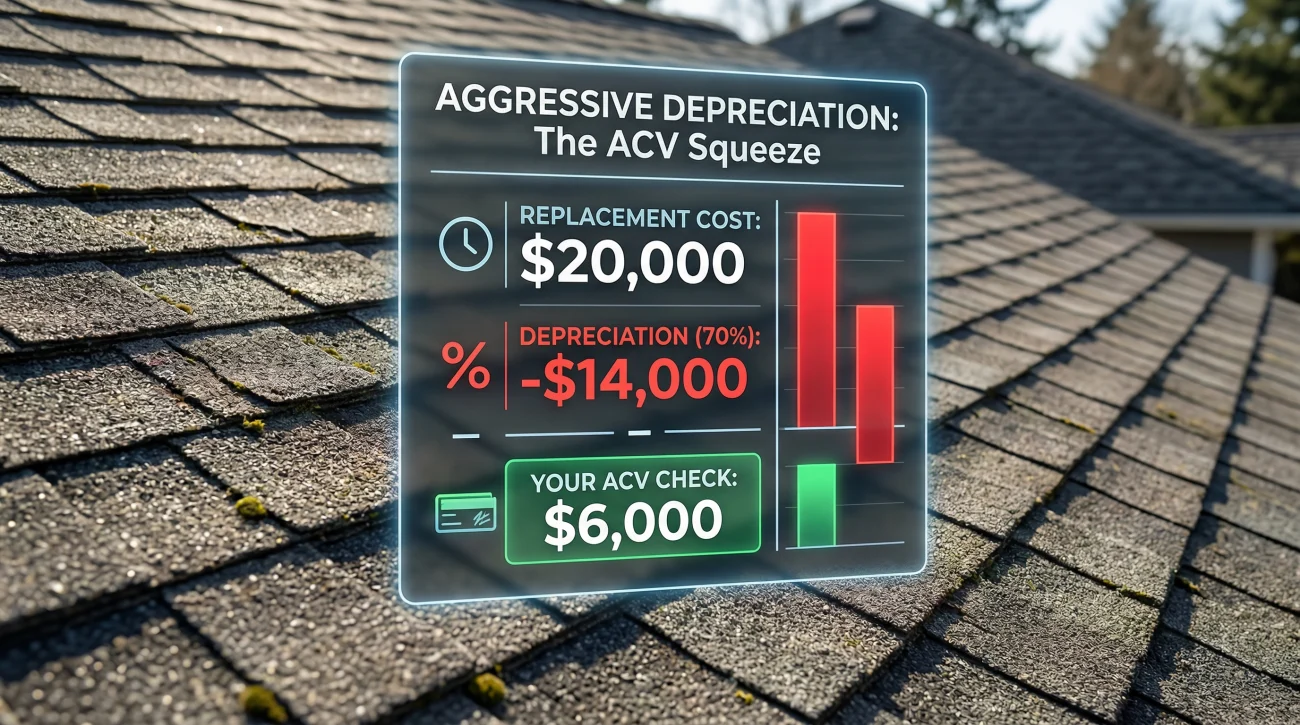

Tactic 5: Aggressive Depreciation (The ACV Squeeze)

Even if the adjuster gets the scope perfectly right, they can still minimize the payout through the math of depreciation.

Most standard homeowners policies utilize a two-check system. The first check you receive is for the Actual Cash Value (ACV). The ACV is the cost to replace your property minus depreciation for age and condition. The adjuster has significant discretion in determining the “condition” of your property.

Let’s look at a concrete math example. Imagine your roof suffered severe wind damage. Your contractor says it will cost $15,000 to replace. The adjuster agrees on the $15,000 replacement cost, but notes your roof is 10 years old. If they apply a standard 50% depreciation, your first check is $7,500. But if they subjectively decide the roof was in “poor condition” before the storm and apply an aggressive 70% depreciation penalty, your first check is only $4,500.

This drastically shrinks your upfront payout, leaving you with barely enough money to hire a contractor to begin the work. While you can eventually claim the rest of the money once repairs are done (the RCV supplement), the heavy upfront depreciation creates a massive problem.

Why this tactic works psychologically:

It creates a massive cash-flow panic for the homeowner. When you are staring at a $4,500 check for a $15,000 problem, you might just patch the roof instead of replacing it, or abandon the claim entirely. I cannot tell you how many homeowners leave thousands of dollars on the table simply because the upfront math felt impossible. Understanding how the two-check system and depreciation holdbacks actually work is vital to surviving this squeeze.

Tactic 6: The “Wear and Tear” Exclusion Trap

When an adjuster investigates a claim, they are looking for the cause of loss. The most common trap I see is the “gradual damage” or “wear and tear” exclusion. If an adjuster can point to a rusted pipe fitting or a slightly weathered roof shingle and claim the damage occurred over months rather than during a sudden, covered event, they will issue a partial or total denial.

This tactic relies entirely on the homeowner taking the adjuster’s interpretation as absolute truth. But an adjuster’s opinion is just that: an opinion. It is not a legal or engineering ruling.

Why this tactic works psychologically:

Homeowners naturally assume the adjuster is an objective building expert. If an inspector in a polo shirt tells you the pipe has been leaking for six months, you are likely to doubt your own memory of the sudden burst. This relies heavily on authority bias.

Tactic 7: Weaponizing Policy Ambiguity

Insurance policies are dense legal contracts written by teams of corporate lawyers. They are filled with ambiguities. When a claim sits in a gray area, adjusters are trained to interpret those ambiguities in favor of the insurance company.

For example, if water damages your custom hardwood floors, the policy might guarantee “materials of like kind and quality.” The adjuster might interpret that as generic builder-grade wood, while your contractor knows it requires premium materials.

Why this tactic works psychologically:

It weaponizes your lack of policy knowledge. Most people have never read their full policy. When the adjuster cites a specific clause or endorsement, the homeowner assumes the interpretation is legally binding, when in reality, it is highly negotiable. Spending time understanding what your specific policy language actually covers is the only way to recognize when an adjuster is overstepping.

Action Step: If you receive a denial or partial denial based on policy language, never accept a verbal explanation. Demand an itemized written explanation.

Subject: Request for Itemized Explanation of Claim Denial

Hello [Adjuster Name],

I received your letter citing “wear and tear” as the reason for denying coverage for the recent water damage. Before I accept this determination, please provide a detailed, written explanation pointing to the specific policy language you are relying on, along with the exact physical evidence your inspection yielded to support the conclusion that this was not a sudden event.

Regards,

[Your Name]

Red Flags Your Claim Is Being Actively Managed Against You

It is easy to read about these tactics in isolation, but in the real world, they usually happen simultaneously. The frustration you feel when dealing with an insurance claim is rarely an accident; it is the byproduct of a system designed to tire you out and limit payouts.

If you are experiencing any of the following signals, your claim is likely off-track:

- 🚩 The rushed inspection: The adjuster’s visit lasted under 45 minutes, even though you have significant, multi-room damage or structural issues.

- 🚩 The suspiciously fast check: You received a settlement offer within a few days of a brief inspection, before any underlying damage could be investigated.

- 🚩 The silent treatment: Your follow-up calls are not being returned after you questioned the initial lowball offer or submitted your contractor’s higher estimate.

- 🚩 The surface-only scope: The settlement document you received does not account for secondary damage (like water wicking into drywall or smoke in your HVAC system).

- 🚩 The conversational trap: You gave a recorded statement before getting an independent estimate, and now the adjuster is using your casual words to cite “deferred maintenance.”

If you recognize three or more of these red flags, your claim is no longer in a routine processing phase.

What Happens When You Try to Push Back Alone

The natural next move for most homeowners is to call the adjuster directly and demand answers. I watch them attempt this every single week. Here is the reality of what typically happens when you try to push back on your own.

First, you might get the silent treatment. Then, when they do reply, they will likely ask you to submit “proof” in the exact format they use (like Xactimate pricing), which you do not have. If you keep pushing, your file might get randomly reassigned to a new desk adjuster, forcing you to start your explanation all over again.

Note: This cycle is not an accident. It is a friction loop designed to exhaust you until you accept the current offer. You are playing their game, on their field, using their rules.

Why Knowing Isn’t Enough (And What to Do Next)

Recognizing that an adjuster is using a delay tactic or minimizing your scope is only step one. The problem is that homeowners are negotiating alone against professionals whose full-time job is claims settlement.

When you tell an adjuster, “I think my settlement is too low,” they will ask you to prove it using Xactimate software, moisture mapping, and specific policy citations. Most homeowners simply do not have the operational tools to push back effectively.

This is where the dynamic changes entirely. When an insurance company realizes you have hired a professional to represent you, someone who knows how to read Xactimate, understands local building codes, and knows how to document hidden damage, the standard tactics usually stop.

A Public Adjuster shifts that power dynamic. They do not work for the insurance company; they work exclusively for you. If your claim is stalled, underpaid, or plagued by the tactics outlined above, your best next step is requesting a free claim review from a licensed public adjuster to see exactly what was missed in your scope.

Final Thoughts: The Adjuster is Not the Final Judge

If there is one thing I want you to take away from my years of reviewing these claim files, it is this: the insurance adjuster’s initial estimate is simply an offer. It is not a final, unchangeable ruling.

Navigating a property claim is incredibly stressful, especially when the system is optimized to limit your payout. But once you understand that delays, lowball estimates, and complex policy citations are just standard negotiating tactics, you take back your power. Do not let the friction of the process force you into a bad settlement. Bring in a professional if you need to, and treat the first check as the beginning of the negotiation, not the end.

❓ FAQ

🕵️♂️ How do I know if my insurance adjuster is lowballing me?

The clearest sign of a lowball offer is a significant gap between the adjuster’s settlement and the estimates you receive from independent, local contractors. If the adjuster’s scope omits hidden damage or fails to include current local material costs, the offer is likely too low.

⏱️ Why is my insurance adjuster taking so long to respond?

While delays can happen during major weather events due to backlog, strategic delays are sometimes used to wear homeowners down. If they repeatedly ask for documents you already sent or go silent for weeks, it may be a tactic to increase your financial pressure so you accept a lower offer.

🎙️ Do I legally have to give a recorded statement to my home insurance?

Most policies include a “duty to cooperate” clause, which insurers often interpret as requiring a recorded statement. However, you have the right to prepare for it, have representation present, or request that questions be submitted in writing. Always check your specific policy terms.

📝 Can I dispute the adjuster’s estimate if it’s too low?

Yes, absolutely. The initial estimate is just an offer, not a final ruling. You can dispute it by providing your own contractor estimates, hiring a public adjuster to write a competing scope of loss, or invoking the appraisal clause in your policy.

🤝 Is it normal for an adjuster to offer a check on the spot?

It is common, but it is often a tactic. A “fast settlement” limits the scope of the claim to only what the adjuster can see immediately. Accepting a check on the spot before an independent contractor investigates for hidden damage can make it harder to claim more money later.

📸 What happens if the adjuster misses hidden damage?

If they miss hidden damage, they will not pay for it in the initial settlement. You must document the newly discovered damage (often when contractors open up walls), stop work, and submit a “supplemental claim” to request additional funds.

📉 How do insurance companies calculate depreciation so high?

Adjusters use proprietary software to calculate depreciation based on the age and “observed condition” of the item. Because “condition” is subjective, adjusters often err on the side of aggressive depreciation, which drastically reduces your first Actual Cash Value (ACV) check.

🗣️ What should I do if the adjuster twists my words?

If you feel your words are being misrepresented to deny coverage (e.g., claiming you admitted to “deferred maintenance”), you should immediately transition all communication to writing via email. Do not agree to further unrecorded phone calls.

🛑 Can an adjuster deny my claim for “wear and tear” after a storm?

Yes, this is a common tactic. If an adjuster believes the roof or pipe was old and failing before the storm, they will use the “wear and tear” or “gradual damage” exclusion. You typically need independent expert evidence to prove the damage was caused directly by the sudden event.

⚖️ How do I effectively push back against an experienced adjuster?

The most effective way to counter these tactics is to hire your own expert, such as a licensed Public Adjuster. They understand the policy language, use the same estimating software as the insurance company, and negotiate on your behalf to ensure the scope of loss is accurate.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.