- A gap between your contractor’s estimate and the insurance adjuster’s estimate is one of the most common hurdles in the property claim process.

- Estimates differ because adjusters use standardized software (like Xactimate), while contractors quote real-world local market costs for labor and materials.

- The most crucial distinction you must make is whether you are facing a “pricing gap” (same items, different costs) or a “scope gap” (the adjuster completely missed damaged items).

- If the gap is over 20%, or if hidden damage was not addressed, it is highly likely a scope issue that requires a professional line-by-line comparison and a formal supplement.

The Frustration of the Estimate Gap

Your contractor inspects the damage and hands you an estimate for $18,000. A week later, your insurance company sends you a settlement letter and a check based on an estimate of $11,000. You are left staring at a $7,000 gap, wondering how two professionals looking at the exact same property could come up with such drastically different numbers.

In my years of reviewing property claim files, I have seen this exact scenario play out hundreds of times. This gap is one of the most common and most frustrating moments for any homeowner trying to rebuild. It often feels like the insurance company is intentionally lowballing you, or that your contractor is trying to overcharge.

While emotions run high at this stage, the reality is usually much more mechanical. Adjuster estimates and contractor estimates are fundamentally built using different languages, different methods, and different priorities. Knowing why this gap exists is the first step. But more importantly, you need to understand what this gap signals about the health of your claim, and exactly how to identify what was left out.

How Adjusters and Contractors Calculate Damage Differently

To understand why your home insurance claim estimate is too low, you have to look at how the two numbers were generated. They are not comparing apples to apples.

The Adjuster’s Method: Xactimate

When an insurance adjuster walks through your home, they are not calling local drywallers or roofers to get current pricing. Instead, they input measurements and damage categories into a standardized estimating software, most commonly a program called Xactimate. If you have been through the standard home insurance claim process, you have likely received one of these reports – a dense, multi-page document filled with obscure line items and unit costs.

Xactimate uses regional pricing databases that are updated monthly. However, this software calculates averages. I have sat across from desk adjusters who rely entirely on the software, ignoring the reality that a specific local contractor might charge more because your neighborhood has difficult parking, or because a specific type of matching material is currently facing a supply chain shortage.

The Contractor’s Method: Real-World Costs

Your local general contractor builds their estimate based on the actual, present-day cost to get a crew into your house and finish the job. They look at access issues, the exact cost of materials at their local supplier this week, minimum trip charges for specialized trades (like plumbers or electricians), and the real-world time it takes to complete the work.

Measures the room, inputs “replace 100 sq ft of standard drywall”, and the software outputs an average regional price.

Knows they have to pay a crew for a full day of labor regardless of the square footage, factor in gas, disposal fees, and local permit costs.

The 5 Most Common Reasons for an Estimate Gap

When you place both estimates side by side, the financial difference usually boils down to one or more of these five specific areas.

1. Hidden and Secondary Damage

Insurance adjusters are generally trained to document what is visible and accessible during their visit. If they cannot see it, they usually do not include it in the initial estimate. Contractors, on the other hand, know how water, smoke, or fire behaves behind the scenes.

For example, if you have a kitchen pipe burst, the adjuster might write an estimate to replace the ruined laminate flooring. But your contractor knows that water travels. They will estimate for pulling up the floor, removing the wet subfloor, replacing the saturated drywall behind the lower cabinets, and treating the area to prevent mold. If the adjuster did not open the walls or lift the floorboards, that hidden damage is completely missing from your settlement.

2. Building Code Upgrades (Ordinance and Law)

Building codes change constantly. If your home is older, repairing a damaged section might require bringing the entire system up to current local codes. For instance, I frequently review claims on 1980s homes where fixing fire-damaged drywall legally requires updating the entire room’s electrical wiring to modern standards.

Contractors must pull permits and follow current laws, so they include these upgrade costs. Adjusters frequently leave code upgrades out of initial estimates, either because they missed the local requirement or because your specific policy requires you to incur the cost first before they will reimburse it.

3. The Missing Overhead and Profit (O&P)

This is arguably the most fiercely contested line item in property claims. Overhead and Profit (often represented as a 10% and 10% markup, totaling 20%) is the standard fee a general contractor charges to coordinate and supervise multiple trades (like a plumber, electrician, and drywaller) on a single job.

I routinely see insurers intentionally drop this 20% markup from their estimates. They will argue that “the job isn’t complex enough to require a general contractor,” even when the repair clearly involves three or more distinct trades. If your contractor includes O&P and your adjuster strips it out, you instantly have a 20% gap.

4. Outdated or Incorrect Software Pricing

Sometimes, the Xactimate database simply lags behind reality. After a major regional weather event, I have watched roofing material costs jump 30% in a single week. The software’s monthly averages will not reflect these sudden surges, leaving the adjuster’s estimate far below what any local contractor will actually accept.

5. Fundamental Scope Differences

The adjuster might say a water-stained ceiling only needs a coat of stain-blocking primer and new paint. Your contractor might say the drywall has lost its structural integrity and must be completely cut out and replaced. If the two professionals disagree on the physical reality of what needs to be fixed, the numbers will never align.

The Critical Distinction: Scope Gap vs. Pricing Gap

Once you understand these five pitfalls, you need to figure out which one is actually tanking your claim. That brings us to the most critical distinction in this entire process. In my daily reviews, I see homeowners exhaust themselves fighting the wrong battle.

I frequently see homeowners spend weeks arguing with their desk adjuster over a 50-cent difference in the cost of a square foot of flooring, completely missing the fact that the adjuster forgot to include the removal of the kitchen cabinets. You can’t win a pricing argument if the scope is fundamentally broken.

| The Pricing Gap | The Scope Gap |

|---|---|

| Both estimates list the exact same repair action (e.g., replace 50 sq ft of drywall). | The contractor’s estimate includes actions the adjuster’s estimate ignores entirely (e.g., tear out subfloor). |

| The disagreement is purely about the cost of labor and materials in your zip code. | The disagreement is about the physical reality of what was actually damaged. |

| Usually accounts for a 10% to 15% difference in the total numbers. | Usually accounts for massive differences (20% or much higher). |

How to Actually Compare the Two Estimates

You cannot identify a scope gap by looking at the summary page of your settlement letter. You must do a line-by-line comparison. Here is the process I use when breaking down a file:

- 👉 Step 1: Demand the full, unabridged Xactimate report from your adjuster. It should be anywhere from 10 to 40 pages long.

- 👉 Step 2: Open your contractor’s bid side-by-side with the adjuster’s report. Group the comparison by room (e.g., Kitchen vs. Kitchen).

- 👉 Step 3: Ignore the dollar amounts at first. Look strictly at the *actions*. If your contractor says “remove baseboards” and the adjuster’s estimate skips straight to “paint walls”, highlight it. That is a missing item.

What the Size of Your Gap Actually Signals

The percentage difference between the two estimates tells a story about how your claim was handled. It often points directly to common adjuster delay and minimization tactics.

If the gap is relatively small (under 10%), it is almost certainly a pricing issue. This might just be the difference between Xactimate averages and your specific contractor’s premium labor rate.

However, if the gap is 20%, 50%, or even double the insurance offer, it is a glaring signal that the adjuster’s investigation was inadequate. Where the gap is concentrated is also revealing: if the roof numbers match but the interior water damage numbers are completely off, it tells me the adjuster likely did not use a moisture meter on the drywall. If the entire gap is on the roof, they likely didn’t walk the full surface.

⚠️ Warning: Never accept a verbal explanation for a large estimate gap. If the adjuster says over the phone, “We just pay less for that kind of repair,” require them to put that reasoning in writing. A polite email stating, “Could you please point me to the specific line item or policy exclusion that reflects our phone conversation?” forces them to create a paper trail. You cannot dispute a phone call.

Your Action Plan: What to Do Next

Once you identify the type of gap, your path forward diverges:

If it is a Pricing Gap: Have your contractor draft a formal letter outlining their real-world costs. They may need to provide supplier invoices or prove that local labor rates have spiked. You can submit this to your desk adjuster to request a price adjustment.

If it is a Scope Gap: You must file a formal supplement. This means your contractor needs to thoroughly document the missing damage with photos, code requirement sheets, and detailed descriptions, and submit it back to the insurer for review.

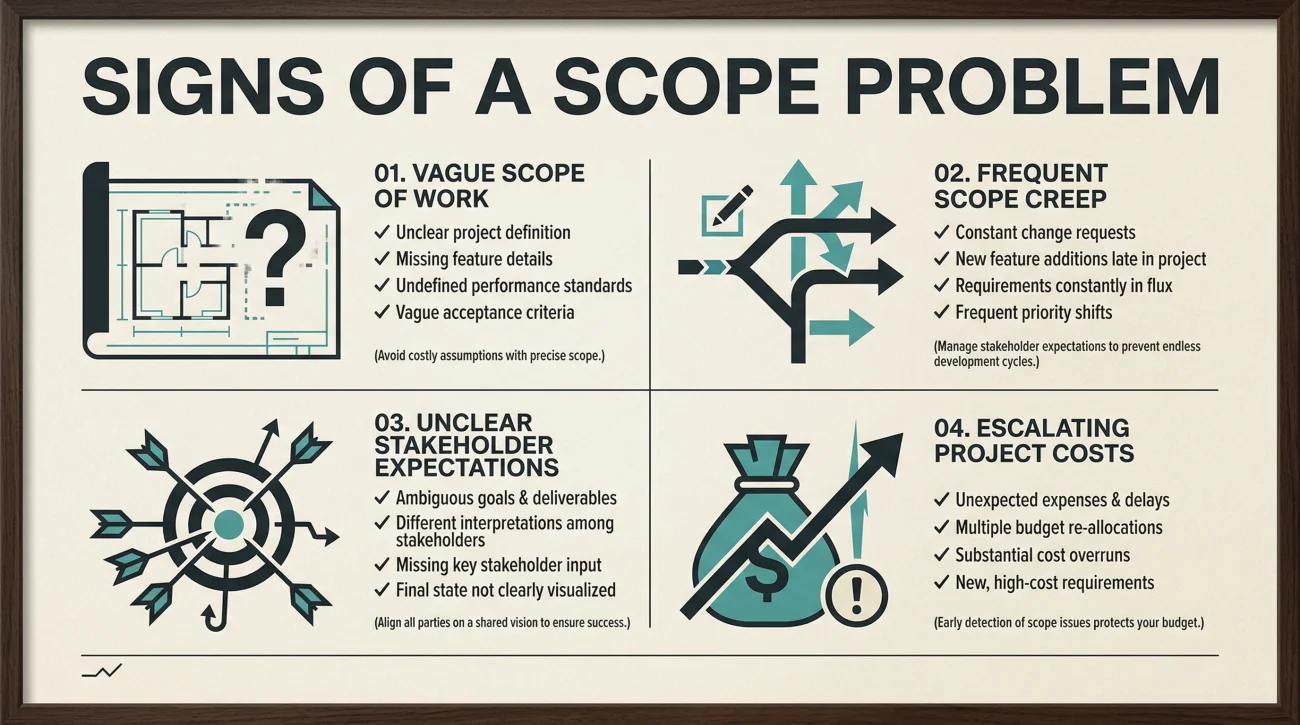

Signs Your Estimate Gap is a Major Scope Problem

When you are holding a check that will not cover the work, it is incredibly easy to panic. Before you take out a personal loan or accept a subpar repair job, look closely at how the adjuster actually handled your file.

I consider an estimate gap to be a severe scope problem if I see any of these operational red flags in a client’s history:

- 👉 The adjuster’s physical visit lasted under 60 minutes, despite significant or multi-room damage to the property.

- 👉 The settlement letter only lists visible surface damage (like paint and carpet) and ignores all structural elements entirely.

- 👉 Your contractor physically identified hidden damage (like wall moisture, subfloor rot, or deep smoke penetration) that is entirely absent from the settlement.

- 👉 The insurer’s estimate does not include any code upgrade costs, even though your contractor explicitly flagged that local laws require them.

If your insurer only sent you a summary page, you cannot begin to diagnose the problem. Request the full document immediately to establish a paper trail.

Hello [Adjuster Name],

I received the settlement summary and the initial payment for my claim. However, the total amount differs significantly from the estimates provided by my licensed contractors.

To understand this difference, please send me the complete, line-by-line Xactimate estimate (or equivalent software report) that details exactly how the settlement figure was calculated, including all measurements and pricing for materials and labor.

Please provide this via email within 48 hours so my contractor and I can review the scope of work.

Thank you,

[Your Name]

Comparing a dense, 30-page adjuster document against a contractor’s findings is a highly technical task. It requires knowing how insurance software works and how to frame a supplement request so it doesn’t get automatically rejected.

💡 Pro Tip: If you are exhausted just thinking about cross-referencing line items, you do not have to do it alone. Level the playing field by getting a free scope comparison from a licensed public adjuster to see exactly what the insurance company left off their report.

Final Thoughts on Low Estimates

One final piece of the puzzle: make sure you are not confusing an estimate gap with a standard depreciation holdback. The first check you receive is usually the Actual Cash Value (ACV), which is the replacement cost minus depreciation for age. That initial check will almost always look shockingly low. You are meant to claim the rest (the RCV supplement) after repairs are completed. For a deep dive on this mechanic, understanding the difference between your ACV and RCV payout is essential.

However, if the total estimated replacement cost on the adjuster’s paperwork is still vastly lower than your contractor’s bid, you have a real gap. Do not let an aggressively low opening offer bully you into a cheap repair. Secure your documents, diagnose the scope, and escalate professionally.

❓ FAQ

❓ Is it normal for the first insurance check to be lower than the estimate?

Yes. The first check is usually for the Actual Cash Value (ACV), which subtracts depreciation. You typically receive the remaining amount (the recoverable depreciation) after you prove the repairs have been completed.

🛑 How do I dispute a low property damage offer?

You dispute it by submitting a detailed supplement. This requires your contractor to provide a line-by-line bid, backed by photographs, local material invoices, and code enforcement documents that prove the adjuster’s scope is incomplete.

📸 Will insurance pay for damage found after the wall is opened?

Generally, yes. Your contractor must stop work, photograph the newly discovered damage before touching it, and submit a supplemental claim. Do not fix hidden damage and throw away the evidence before the insurer approves it.

📈 Can an insurance company refuse to pay Overhead and Profit (O&P)?

They frequently try to refuse it by claiming the job isn’t “complex” enough. However, industry standard generally dictates that if three or more distinct trades (e.g., drywall, electrical, flooring) are required, O&P is warranted.

🔨 Can I hire my own contractor instead of the insurance company’s?

Yes. You have the right to hire any licensed contractor you choose. Insurers have “preferred vendor” networks, but you are never legally obligated to use them.

⏳ How long do I have to supplement an insurance claim?

The window varies significantly by state law and your specific policy language. Never rely on general timelines. Always confirm the exact deadline directly with your insurer in writing to avoid missing your window.

📝 What is Xactimate in insurance claims?

Xactimate is the standard estimating software used by most property adjusters. It uses regional databases to determine average pricing for materials and labor, which often lags behind real-time, local market spikes.

💸 Should I cash a low settlement check?

Cashing the standard initial ACV check usually does not prevent you from filing a supplement. However, never sign a document labeled “Release of All Claims” or accept a “full and final settlement” buyout if you intend to ask for more money.

🤝 Do I need a lawyer for a low insurance estimate?

For a pure estimate or scope dispute, a public adjuster is usually the most effective first step, as they handle the technical estimating. Lawyers are typically needed if the insurer is acting in bad faith or outright denying covered perils.

🕵️♂️ What if the adjuster refuses to share their line-by-line estimate?

Put your request in writing via email. If they continue to withhold the breakdown of how they calculated your payout, they are obstructing your ability to repair your home. This is a red flag that warrants professional intervention.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.