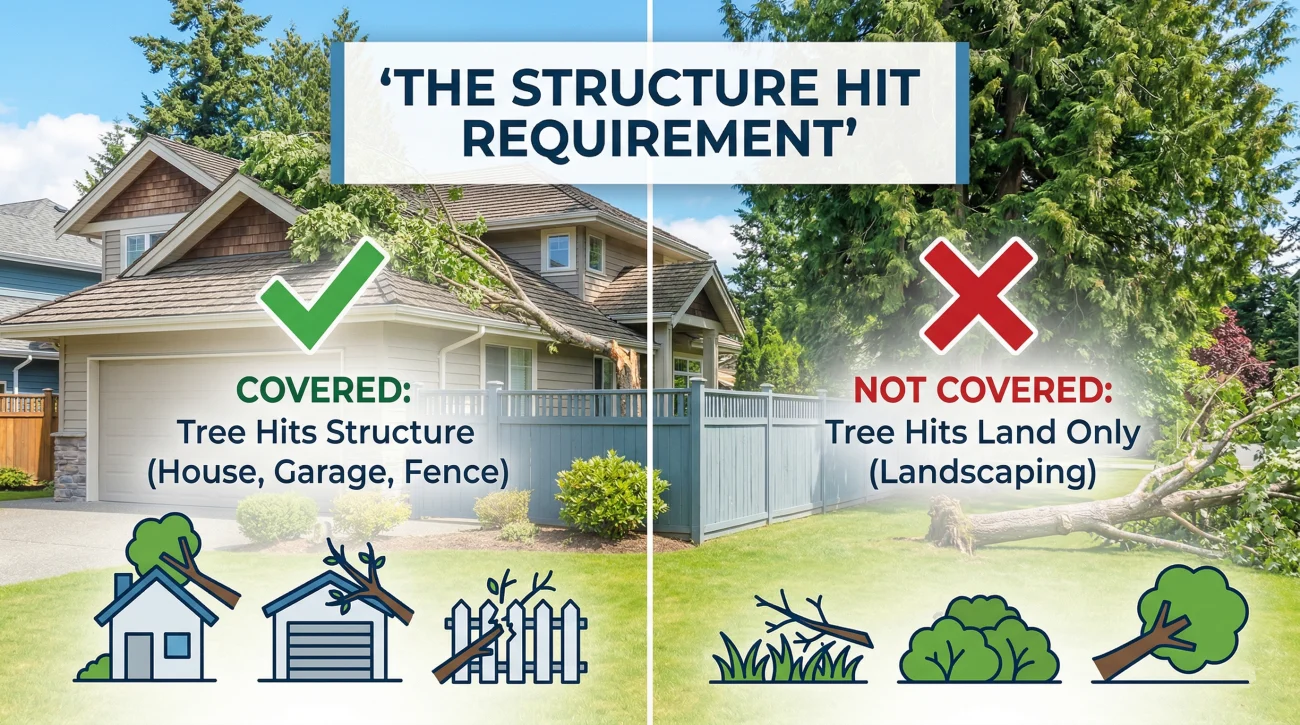

- Most standard policies cover tree damage only if the tree physically strikes a covered structure, like your home, garage, or fence.

- If a neighbor’s tree falls on your house, your insurance pays the claim. The neighbor is only liable if you can prove they were negligent before the fall.

- Insurers frequently deny claims by arguing the tree was dead or rotting, shifting the cause from a sudden accident to a foreseeable maintenance failure.

- Tree removal sub-limits usually cap at $500 to $1,000 per tree, which often leaves homeowners paying out of pocket for major cleanups.

The Reality of Tree Damage Claims

When a heavy tree crashes through your roof or takes out your fence, the immediate focus is on safety and securing the property. You call your insurance company expecting a straightforward tree damage insurance claim. After all, a tree falling is a sudden, dramatic event. But when the adjuster arrives and starts looking closely at the condition of the trunk or asks where exactly the tree landed, the process can quickly become complicated.

In my experience reviewing property files, tree damage claims are uniquely frustrating for homeowners. The damage is obvious, yet the coverage is often heavily debated. Adjusters frequently bring up terms like “negligence,” “maintenance failure,” or “debris removal sub-limits.” These phrases are signs that your claim might not be paid in full.

I have seen homeowners left with thousands of dollars in out-of-pocket expenses simply because they did not understand how their policy categorizes tree removal versus structural repair. This guide will walk you through exactly how insurers assess fallen tree incidents, the specific rules regarding neighbor disputes, and how you can document your damage to protect your settlement.

The Basic Coverage Rule: The Structure Hit Requirement

To understand what your policy covers, you have to look at the event through the eyes of an insurance adjuster. Standard homeowners insurance policies cover sudden and accidental damage. However, when it comes to trees, there is a very specific trigger required for coverage to apply.

The fallen tree must physically strike a covered structure. If a massive oak tree falls during a storm but lands entirely on your front lawn without touching your house, your shed, or your fence, your structural coverage typically will not respond. In the insurance world, a tree laying in the grass is considered a landscaping issue, not a property damage claim.

Key Point: The definition of a “covered structure” includes your main dwelling, an attached garage, a detached garage, a shed, and typically your fences. If the tree hits any of these, you have grounds for a claim.

If the tree does hit your house, the resulting structural damage is treated like any other peril. The cost to repair the roof, replace the siding, and fix the framing is covered under your dwelling limits. However, the cost to actually chop up and haul away the tree itself is handled differently, which is where many homeowners encounter their first major scope gap.

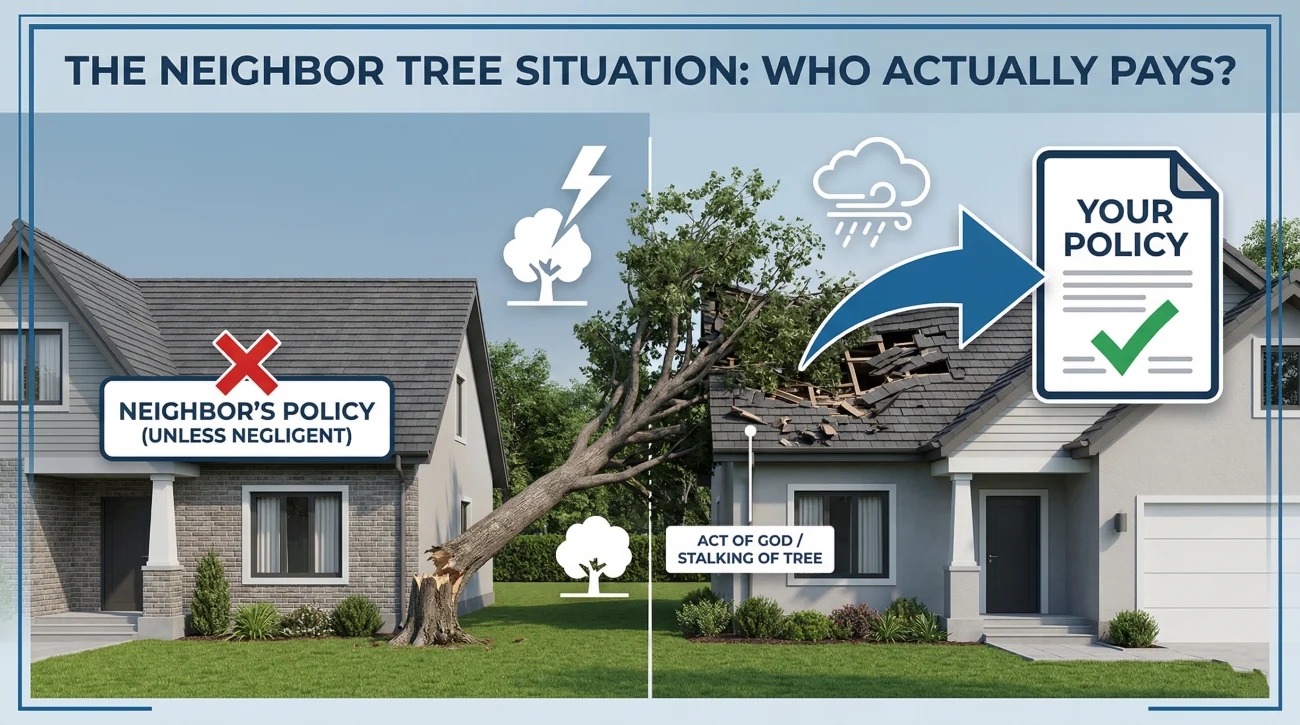

The Neighbor Tree Situation: Who Actually Pays?

One of the most common questions I hear involves property lines. When a neighbor tree fell on my house insurance wise, the immediate reaction is usually anger directed next door. Most people assume that because the tree belonged to the neighbor, the neighbor’s insurance should pay for the roof repair.

That is rarely how it works in practice. If a healthy tree falls due to a severe storm or high winds, insurance companies view it as an “Act of God.” In these scenarios, the tree becomes your problem the moment it crosses your property line and strikes your home. Your homeowners insurance policy will be the one to pay for your damages, and you will be responsible for your deductible.

I am also frequently asked about trees that sit exactly on the property line. Generally, these are considered shared property, but the rule of thumb remains the same. If it falls and hits your side of the property, your insurance responds to your specific damage.

Waiting for your neighbor’s insurance company to inspect your damaged roof and write you a check, delaying your own cleanup efforts.

Filing a claim directly with your own insurance company immediately so they can cover the repair and tarp the roof to prevent water intrusion.

The only exception to this rule involves clear negligence. If the tree was dead, rotting, and visibly leaning over your property for months, and your neighbor knew about it but did nothing, they might be held liable. However, you must prove they were negligent. This usually requires a paper trail, such as a certified letter you sent them warning about the dangerous tree prior to the fall. Without prior written notice, proving liability is an uphill battle.

The standard insurance mechanism is clear. Let your insurer handle your repairs. If your insurer believes the neighbor was negligent, they may attempt to recover the costs directly from the neighbor’s policy later through a process called subrogation. If they succeed, they will typically reimburse your deductible.

The Dead or Rotting Tree Denial

When the insurance adjuster visits your property, they will take extensive photographs of the damage. But they will also take close-up photos of the tree stump, the exposed root ball, and the fallen branches. They are looking for signs of disease, rot, or insect infestation.

This brings us to the most frequent cause for a tree damage claim denial. If the adjuster determines the tree fell because it was dead or severely diseased rather than due to a sudden weather event, the insurer will likely cite a “maintenance failure.” Homeowners insurance covers sudden and accidental events, not damage that could have been prevented through routine property maintenance.

I have seen perfectly valid claims heavily disputed because a single photograph showed a hollow core in the trunk. Even if wind knocked the tree down, the adjuster argued the tree was compromised and would have fallen anyway. This is where the narrative shifts from an accident to negligence.

The dispute centers on whether you knew or should have known the tree was a hazard. A tree can have internal rot while still displaying green leaves and looking perfectly healthy to the untrained eye. If your claim is denied on these grounds, you have the right to challenge it. An independent arborist report can sometimes confirm that the disease was internal and not visible to a reasonable homeowner. If you find yourself in this situation, understanding the typical pathways to navigate a home insurance claim denial becomes your immediate priority. But even if the claim is approved, the next hurdle is figuring out exactly how much the insurer will pay to get the tree off your property.

Tree Removal Costs and Sub-limits

Removing a massive tree from a residential property requires heavy machinery, cranes, and specialized crews. The bill can easily reach thousands of dollars. Unfortunately, does homeowners insurance cover tree removal is a question with a very strict, sub-limited answer.

Most standard policies have a specific “debris removal” sub-limit. This is a cap on how much the insurer will pay to cut up and haul away the tree debris. Commonly, this limit is set at $500 to $1,000 per tree. If multiple trees fall during a single storm event, policies typically enforce an overall cap (for example, a maximum of $1,000 or $2,000 total) for debris removal regardless of how many trees fell.

There is a critical distinction that many adjusters fail to explain clearly, and it is a major area where claims fall short.

| Type of Removal Action | How It Is Covered |

|---|---|

| Lifting the tree off the damaged roof | Considered part of the structural repair (Dwelling Coverage A). No sub-limit typically applies. |

| Chopping logs and hauling branches from the yard | Classified as debris removal. Subject to the strict sub-limit per tree. |

When you hire a contractor, make sure their invoice clearly separates the cost of extracting the tree from the structure from the cost of hauling the debris away. If the invoice is lumped together as a single “tree service” line item, the adjuster may apply the low debris removal sub-limit to the entire bill, leaving you to pay the difference.

When No Structure Was Hit: Fences, Driveways, and Vehicles

In my reviews of partial denials, this is a common point of friction. What happens if the tree misses the house but causes other damage? This scenario triggers entirely different sections of your policy.

If the tree hits your fence, it is covered under the “Other Structures” portion of your policy (Coverage B). However, you must be aware of how the settlement is calculated based on your policy type. Unlike your roof, which might have Replacement Cost Value (RCV) coverage paying for a brand new replacement, fences are usually paid at Actual Cash Value (ACV). ACV deducts for depreciation. I have had to explain to many frustrated homeowners why their completely destroyed 15-year-old fence only yielded a few hundred dollars in settlement.

If the tree falls and damages your driveway or underground plumbing without hitting a structure, coverage becomes very difficult to secure. Many policies exclude damage to land, driveways, and underground systems unless explicitly endorsed.

Finally, a tree fell on car homeowners insurance scenario is quite common. If a tree falls on your vehicle in the driveway, your homeowners insurance will generally not cover the car. You must file a claim under the comprehensive coverage of your auto insurance policy. Your homeowners policy will, however, usually pay the debris removal sub-limit to remove the tree from the driveway if it is blocking your access.

Documenting the Damage Effectively

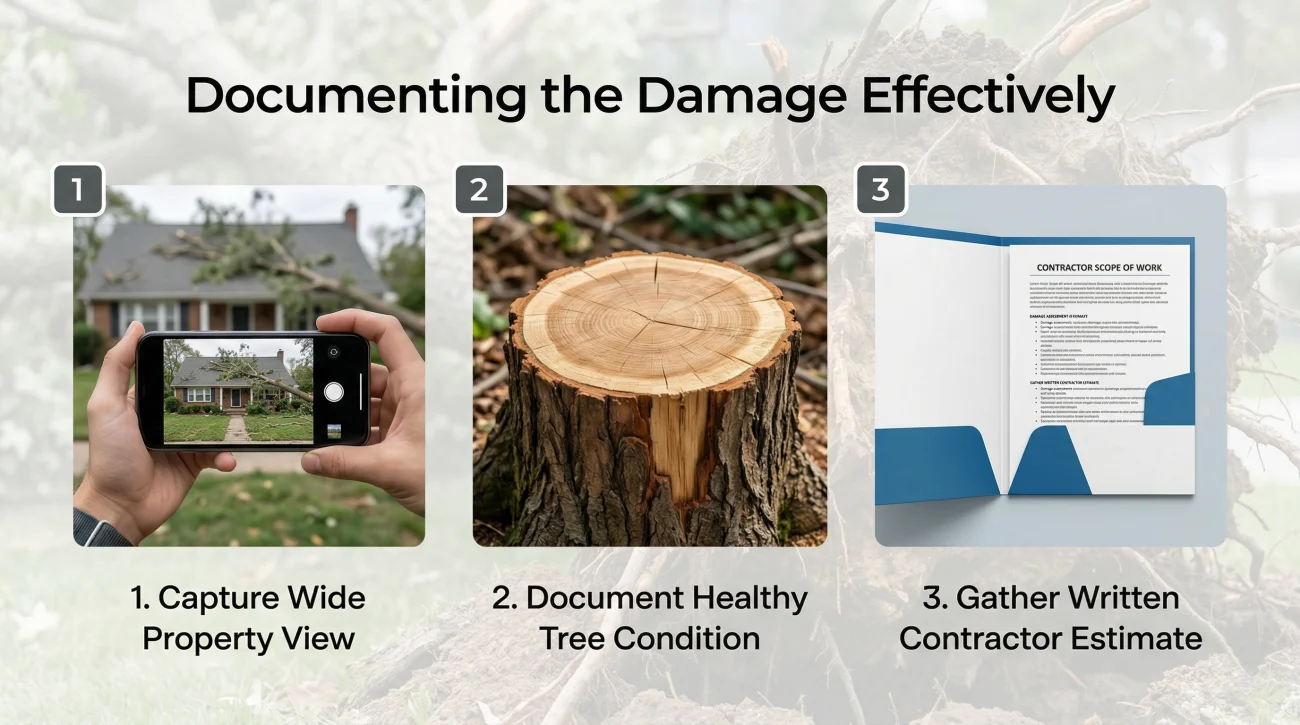

The speed at which tree damage must be cleared often creates a documentation nightmare. I have seen too many homeowners lose out on legitimate payouts because the tree service cut up all the evidence before the adjuster arrived.

Before anyone touches the tree with a chainsaw, you must document the scene. Take wide photos showing the entire fallen tree and its relationship to your house. Take close-up photos of the impact points on the roof, siding, and gutters. Crucially, photograph the stump and the root ball to show that the wood was solid and healthy prior to the fall.

If the tree fell during a severe storm, remember that the tree impact might not be your only damage. High winds that brought down a heavy trunk likely caused shingle damage, lifted flashing, or shifted siding on other elevations of the home. I always advise homeowners to treat a storm-related tree fall as a multi-system claim. Because wind affects the whole structure, understanding how storm and wind damage assessments work helps ensure the adjuster inspects the entire property, not just the single spot where the tree landed.

Instead of just pointing the tree service to the roof, your immediate response should be a specific three-step process: secure emergency tarping to stop water, take comprehensive photos of the stump and impact points before cutting begins, and get a detailed written scope of work from your contractor.

When communicating with the adjuster after their initial visit, keep everything in writing to secure your paper trail.

Hello [Adjuster Name],

Thank you for inspecting the property today. I am writing to confirm that you documented the structural impact on the roof, the broken rafters in the attic, and the healthy condition of the stump. Please let me know when we can expect the initial structural estimate, and confirm how the crane extraction costs will be categorized under the dwelling coverage.

Thank you.

Signs Your Tree Damage Claim Is Heading for Trouble

The difference between a fully paid tree claim and a frustrating out-of-pocket loss often comes down to how the adjuster characterizes the event. Watch for these specific signals that your claim is being steered toward a denial or a severe underpayment.

- The adjuster spends more time taking photos of the tree stump and asking about your landscaping maintenance than inspecting the damage to your roof.

- Your insurer is citing the tree’s age or condition as a basis for denial, effectively categorizing a sudden storm drop as a preventable maintenance failure.

- The tree removal service quoted an expensive crane extraction from your attic, but the adjuster is incorrectly categorizing the entire invoice as yard debris to cap your payout.

- The neighbor’s tree caused the damage, and your adjuster is telling you to pursue the neighbor directly instead of processing the claim under your own policy.

- The structural estimate includes patching the roof decking but completely ignores the structural framing, interior drywall cracking, or water intrusion that occurred before the tarp was placed.

If you see any of these patterns, the adjuster is likely building a case to minimize your settlement. It is time to pause and get a second set of eyes on the file before signing any releases.

Final Steps to Protect Your Claim

A fallen tree creates a chaotic environment, and insurance companies often rely on that chaos to settle claims quickly and quietly. As you review your initial settlement offer, remember that what the adjuster documented is only part of the story. The distinction between sudden damage and foreseeable wear, or between structural extraction and yard debris, can cost you thousands if applied incorrectly.

You also need to verify exactly how your deductible is being applied. If the tree fell during a named storm, your insurer might trigger a much higher wind or hurricane deductible rather than your standard flat deductible. Because tree incidents share the same structural dispute patterns as other major events, I suggest reviewing how different home insurance claims by damage type are handled to see where your specific scope gaps might be hiding.

If your tree damage claim was denied based on a questionable rot assessment, or if the insurer is using debris limits to avoid paying for massive roof damage, do not just accept the first letter. A licensed professional can identify exactly where the adjuster misapplied the coverage rules. Getting a second opinion is your safest next move, and having a public adjuster review the scope before you accept can change the entire trajectory of your recovery.

❓ FAQ

🌳 Does home insurance cover tree damage to my roof?

Yes, standard homeowners policies cover damage to your roof and home structure caused by a fallen tree, provided the tree fell due to a sudden and accidental peril like wind or a storm.

🏡 What happens if a neighbor tree fell on my house insurance wise?

Your own homeowners insurance will handle the claim and pay for your repairs. Your neighbor is only liable if you have documented proof they were negligent regarding the tree’s health prior to the fall.

🚗 Is a tree fell on car homeowners insurance claim possible?

No, homeowners insurance generally does not cover vehicles. If a tree damages your car, you must file a claim under the comprehensive coverage of your auto insurance policy.

🪓 Does homeowners insurance cover tree removal if no structure was hit?

Typically, no. If a tree falls purely in your yard without striking a covered structure, blocking a driveway, or damaging a fence, most insurers consider it a landscaping issue and will not pay for removal.

🪵 Can I file a dead tree fell on house insurance claim?

You can file the claim, but insurers frequently deny claims involving dead trees by arguing it was a maintenance failure rather than an accident. You may need an arborist to prove the rot was internal and unforeseeable.

🚧 How does an insurance claim for tree damage to fence work?

Fences are considered “Other Structures” and are covered. However, insurers typically pay for fence damage at Actual Cash Value (ACV), meaning they will deduct money based on the age and wear of the fence.

💰 What is the average tree damage house insurance payout?

Payouts vary wildly depending on the severity of the structural damage. Roof impacts can range from $5,000 to over $30,000, while simple debris removal is usually capped at a set policy sub-limit.

📸 How to prove tree damage for a fallen tree insurance claim?

Take immediate photos of the fallen tree before cleanup, highlighting the impact points on the structure. Most importantly, photograph the healthy stump and root ball to prove the tree was not dead prior to falling.

❌ Why would my tree damage claim be denied?

The most common reasons for denial are that the tree was dead or diseased (maintenance failure), the tree did not hit a covered structure, or the damage was entirely pre-existing.

⏱️ How long do I have to file a tree damage insurance claim?

Most policies require you to file promptly after the event, usually within one year, though state laws vary. You should report the claim immediately to allow the insurer to inspect the damage before repairs begin.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.