- A frozen and burst pipe is a covered peril, but insurers frequently attempt to deny these claims by accusing the homeowner of failing to maintain adequate heat.

- The burden is on the insurance company to document that you actually neglected the property, not just assume it because a pipe froze during a cold snap.

- Your plumber’s documentation is your strongest defense. Retain the burst section of the pipe and require the plumber to document the cause of the failure in writing.

- Discovering a burst pipe days after it happens does not automatically make it excluded “gradual damage,” provided you document the timeline of discovery correctly.

When a Winter Freeze Turns Into a Claim Dispute

A pipe freezes, bursts, and floods your home. On paper, this is supposed to be one of the clearest, most straightforward covered events in a standard policy. You pay your premium exactly for this type of sudden, catastrophic winter disaster. Yet, a home insurance claim for burst pipe damage is routinely one of the most contested files I see in the field.

If you are filing a burst pipe insurance claim, you might expect the adjuster to arrive, measure the water damage, and write an estimate. Instead, you will often find them asking highly specific questions about your thermostat, your winterization habits, and when you last occupied the property. They are not just investigating the damage; they are investigating you.

I have reviewed hundreds of these claims, and the pattern is remarkably consistent. Insurers frequently attempt to shift a plumbing failure into a maintenance issue. They do this by issuing a negligence denial, arguing that you failed to keep the house warm enough. Understanding how adjusters build this argument, and knowing exactly what documentation you need to dismantle it, is the difference between a fully funded repair and a devastating denial.

The Negligence Denial Explained

To understand why frozen pipe claims get denied, you have to understand the foundational rule of your policy: it covers “sudden and accidental” damage, but explicitly excludes damage resulting from a failure to maintain the property. When a pipe bursts in the winter, the insurance company looks for an opportunity to classify the event as a predictable result of your negligence rather than a sudden accident.

I recently reviewed a file where a pipe burst in a master bathroom during a historic freeze. The insurer initially denied the claim, stating the homeowner must have left a window open. We pulled the home’s smart thermostat data showing the ambient temperature never dropped below 68 degrees prior to the pipe failure. The pipe actually burst due to poor insulation in the exterior wall cavity, not homeowner negligence. Once we submitted the data log, the denial was reversed.

The adjuster’s objective during the initial inspection is to find evidence that you failed to heat the home or failed to drain the system. They will look for open vents, uninsulated crawlspaces, or thermostats set too low. If they can build a narrative that you did not take reasonable care to prevent the freeze, they will issue a denial.

Telling the adjuster, “It was really cold outside, I guess the pipe just froze,” leaving the cause open to their interpretation.

Showing the adjuster your thermostat settings and presenting the plumber’s written statement confirming the pipe failed despite adequate interior heating.

What ‘Failure to Heat’ Actually Requires

One of the biggest misconceptions homeowners have is that they must prove they did everything perfectly. In reality, the burden of proof rests with the insurance company. To legitimately deny your claim for failure to heat, the insurer must demonstrate that the home was being maintained below a reasonable threshold that caused the freeze.

Simply having a burst pipe in the middle of winter is not sufficient evidence of negligence. A pipe in a properly heated home can easily burst due to age, sudden pressure changes, or severe external temperature drops that overcome the home’s insulation. The insurer cannot simply assume you turned the heat off; they have to document it.

⚠️ Warning: Never guess about your thermostat settings when speaking to an adjuster. If you say, “I might have turned it down to 50 degrees before I left,” that casual, uncertain statement will be recorded as a factual admission of negligence in your claim file.

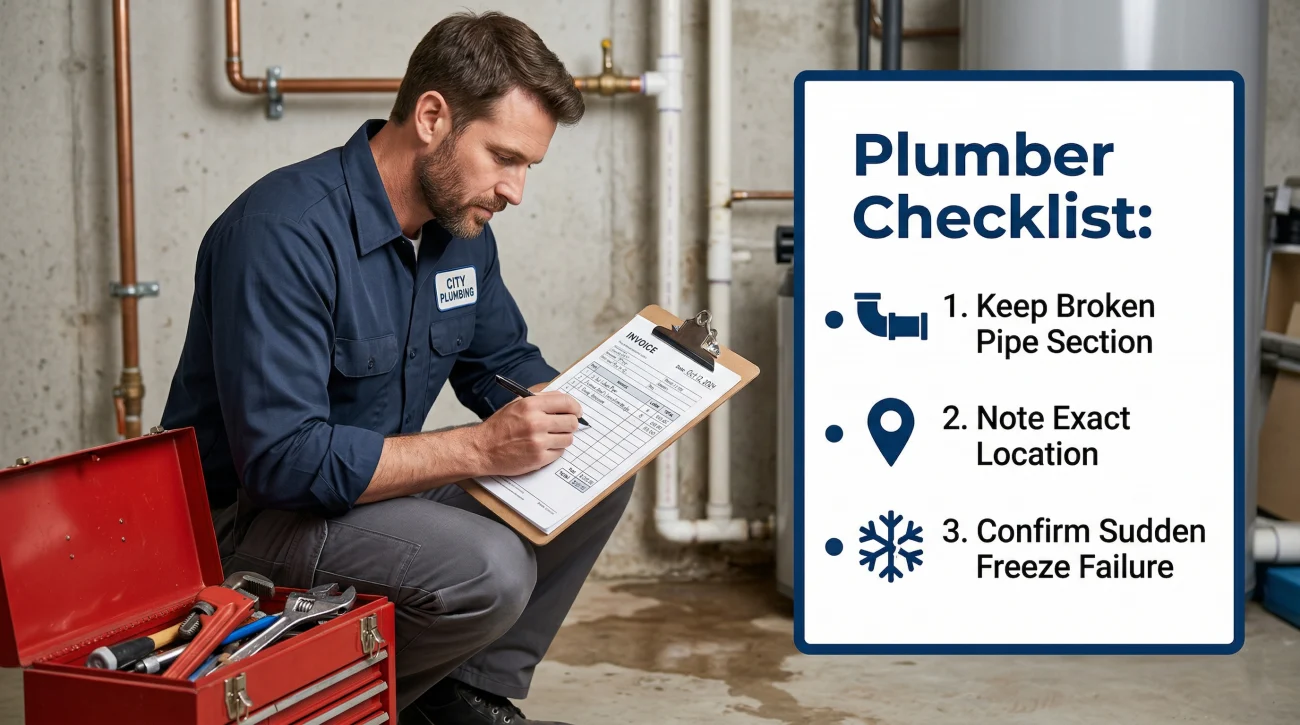

Securing the Right Plumber Documentation

Proving the ambient temperature of your home is only half the battle. You also need an expert to confirm exactly how the pipe failed. While you are compiling your heating evidence, you also need to secure physical evidence, and this brings us to your plumber. Your plumber is your first line of defense against a bad faith adjuster.

Adjusters are not licensed plumbers, but they will happily determine the cause of the break if no professional contradicts them. You must instruct your plumber to do two specific things before they leave the property: retain the broken section of the pipe for the adjuster to inspect, and explicitly state the cause of the failure on the invoice.

Sample request to your plumber:

The Vacancy Problem in Winter Claims

Pipes in vacant homes face a significantly higher hurdle. If you were away on vacation, or if the property is a second home that was unoccupied when the pipe burst, the adjuster will immediately look for the vacancy clause in your policy. Most policies state that if a home is vacant for a certain period (often 30 to 60 days), coverage for water damage or frozen pipes is heavily restricted unless you took specific preventative steps.

If your home was vacant, you must proactively prove that you either maintained heat in the building or completely shut off the water supply and drained the system. Without documentation for one of those two actions, overcoming the vacancy exclusion becomes an uphill battle.

| Occupancy Status | Adjuster’s Primary Assumption | Your Required Documentation |

|---|---|---|

| Primary Residence (Occupied) | Pipe froze due to inadequate ambient heat. | Utility bills, smart thermostat logs, statements confirming heat was on. |

| Away on Vacation (Short Term) | Homeowner turned heat off to save money. | Proof of travel dates, utility usage showing furnace cycles during absence. |

| Vacant Property (Long Term) | Failure to winterize the plumbing system. | Plumber receipts for winterization, or proof the main water valve was shut off. |

The Discover-and-Claim Sequence

Another area where burst pipe claims fall apart is the timeline of discovery. A pipe that bursts inside a ceiling or behind drywall might leak for days before the water pools enough to become visible in your living room. When you finally call the insurance company, the adjuster might notice extensive rot or prolonged saturation and attempt to classify the claim as “gradual damage.”

Gradual damage (like a slow, dripping leak under a sink over six months) is typically excluded. A sudden burst that you simply could not see for a few days is not gradual damage; it is a delayed discovery of a sudden event. It is critical that you frame the timeline correctly from your very first communication.

Hello [Adjuster Name/Claims Dept],

I am writing to report a sudden pipe burst at my property. The water damage became visible to me on [Date] at [Time], at which point I immediately shut off the main water supply to mitigate further damage. The plumber arrived on [Date] and confirmed a sudden pipe failure inside the wall cavity.

Attached are my initial photographs of the damage upon discovery, along with the plumber’s assessment. Please let me know when the adjuster will be scheduled to inspect the structural damage.

The True Scope: Depreciation, Displacement, and Multi-System Damage

Securing the right drying protocol prevents secondary mold, but structural damage is only one part of the financial equation. A severe burst often turns into a complex multi-system claim. This is where I see the biggest financial gaps between what homeowners need and what insurers offer.

The ACV vs. RCV Trap

If your burst pipe ruins custom kitchen cabinets or high-end hardwood floors, the initial check you receive will likely be based on Actual Cash Value (ACV). This means the insurer deducts for depreciation based on the age of the materials. Many homeowners panic at this low number. If you have Replacement Cost Value (RCV) coverage, you are entitled to the full amount, but the withheld depreciation is only paid after the repairs are completed and invoiced. Check your policy’s declarations page to verify whether you carry ACV or RCV coverage before panicking over that first check.

Additional Living Expenses (ALE)

A major burst pipe often requires shutting off the main water or tearing out bathrooms, making the home temporarily unlivable. Your policy likely includes Additional Living Expenses (ALE) to cover a hotel, food, or temporary rental. Insurers rarely volunteer this coverage upfront; you have to invoke it by proving the home lacks basic sanitation or safety.

Signs Your Burst Pipe Claim Was Mishandled

Homeowners often accept a denial because the letter quotes dense policy language that sounds authoritative. But policies rely on the facts of the loss, and those facts are often poorly investigated. You need to look critically at how the adjuster reached their conclusion. You are likely dealing with a mishandled claim if you are experiencing any of the following:

- ❌ The denial letter cites “negligence” or “failure to heat,” but the adjuster never requested your utility bills or thermostat records to verify the actual ambient temperature.

- ❌ Your home was fully occupied and heated, yet the adjuster is applying vacancy-related restrictions to the claim.

- ❌ The adjuster is classifying the event as “gradual damage” simply because the pipe burst inside a wall and you did not discover it immediately.

- ❌ The settlement offer only covers surface repairs (drywall patching, paint) but ignores the saturated subfloor damaged by the pressurized water.

- ❌ The drying equipment was removed by order of the insurer while the structural framing was still reading high moisture levels.

How to Appeal a Denial or a Disputed Estimate

If you are reading this after already receiving a denial letter, understand that a denial is an initial negotiating position, not a final legal verdict. A negligence denial based solely on the fact that a pipe froze in winter without documented proof that you turned off the heat is highly vulnerable to a formal appeal. The burden remains on them to prove the exclusion applies.

If your claim was approved, the most common hurdle is the “estimate gap.” Your contractor says repairs will cost $25,000; the adjuster’s estimate is $9,000. This is rarely a simple disagreement over the price of drywall. It is a disagreement over the scope. The adjuster’s estimate likely omits continuous flooring rules, required code upgrades, and the extended structural drying time.

Whether you are fighting an outright negligence denial or an estimate that leaves out thousands of dollars in structural repairs, bringing in an independent expert changes the dynamic. A professional can pull the moisture readings, challenge the adjuster’s assumptions about your heating habits, and write a complete scope of loss. If you feel your burst pipe claim has been unfairly denied or significantly undervalued, you should consider exploring options for getting a second set of eyes on your water damage scope from a licensed public adjuster.

Final Thoughts on Burst Pipe Claims

You buy insurance to protect you on your worst days, and a flooded house from a burst pipe is absolutely one of those days. Do not let an adjuster’s rushed inspection or default assumption of negligence cost you the coverage you paid for. Control the narrative from day one by gathering your heating evidence, insisting on detailed documentation from your plumber, and never settling for a purely visual inspection of hidden water damage. When you force the insurer to evaluate the claim based on hard facts rather than exclusions, the balance of power shifts back to you.

❓ FAQ

🥶 How long do I have to file a burst pipe claim?

You should file the claim immediately upon discovering the damage. While most policies allow up to a year to file formally, delaying the report gives the adjuster room to claim the damage worsened due to your inaction.

💧 Does homeowners insurance cover the broken pipe itself?

Generally, no. The insurance policy covers the resulting water damage to your home and property, but it usually does not pay the plumber’s bill to replace the actual piece of pipe that failed.

🌡️ What constitutes ‘reasonable care’ for heating a home?

While policies rarely state an exact degree, maintaining the interior ambient temperature at 55 degrees Fahrenheit or higher is the standard industry benchmark to demonstrate you took preventative care.

🏚️ What happens if the pipe burst while I was on vacation?

If you were away temporarily, you must prove you left the heat on. Providing evidence of furnace cycles or energy usage during your absence is usually sufficient to bypass a denial.

💸 Will my rates go up after a frozen pipe claim?

Yes, in most cases, filing a significant water damage claim will result in a premium increase at your next renewal, and it will be recorded on your CLUE report for up to seven years.

📸 What pictures should I take before cleanup begins?

Take wide shots of the flooded areas, close-ups of the burst pipe while it is still inside the wall, and photos of any damaged personal property before you move it or begin water extraction.

🛑 Can the insurer deny my claim if I didn’t shut off the water fast enough?

They can deny coverage for additional damage if they prove you knowingly allowed the water to keep running. However, if you shut the main valve off as soon as you discovered the leak, you have fulfilled your duty to mitigate.

🚰 Is a slow pipe leak covered the same way as a burst pipe?

No. A sudden burst is typically covered, but a slow, continuous leak that happens over weeks or months is often denied under the policy’s gradual damage or maintenance exclusion.

📝 What should I ask the plumber to write on the invoice?

Ensure they explicitly document the exact location of the break and confirm it was a sudden pressure or freeze failure. For a detailed script, see the Plumber Documentation section above.

🏨 Will my insurance pay for a hotel if my house is flooded?

If the damage makes the home uninhabitable (e.g., no working bathrooms or severe safety hazards), your Additional Living Expenses (ALE) coverage should pay for temporary housing and extra food costs.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.