- External smoke damage from wildfires or neighbor fires is frequently undervalued because adjusters rely on visual surface inspections for an invisible contaminant.

- The most expensive and commonly missed components are HVAC system contamination and soft-goods personal property, both requiring specialized assessment.

- Proper documentation must happen before you dispute a claim. Independent industrial hygienist testing is the standard method for proving non-visible particulate exists.

- Insurers often try to characterize smoke damage as “cosmetic” odor. A scientific testing report forces them to address the structural contamination.

- Never accept a settlement based on a visual-only assessment without first having your ductwork, insulation, and air quality professionally evaluated.

The Invisible Reality of External Smoke Damage

When your home survives a nearby wildfire or a neighbor’s structure fire, the immediate feeling is relief. But that relief often fades once the smoke clears and the invasive, lingering odor remains. Filing a smoke damage insurance claim for an external event is a unique process. Unlike a fire that originates inside your home, the damage here is primarily airborne. The structure is intact, but the environment inside is compromised.

In my experience reviewing claim files, external smoke damage is one of the most systematically undervalued categories in the industry. Homeowners call their insurer expecting a comprehensive cleanup. The adjuster arrives, conducts a visual walkthrough, wipes a wall with a sponge, and writes an estimate for surface cleaning and perhaps a coat of paint. When I review these estimates, the pattern is entirely predictable: the visual inspection completely misses the ductwork, the insulation, and the micro-particulates embedded in porous materials.

Because of this heavy reliance on what can be seen with the naked eye, if you are dealing with smoke from a wildfire or a neighbor’s property, you are facing a scope dispute waiting to happen. The gap between what the adjuster sees and what has actually contaminated your home can be tens of thousands of dollars. Understanding how to document this unseen damage is the only way to secure a settlement that covers your true recovery costs.

I have reviewed dozens of wildfire claims where the initial adjuster’s visual inspection found zero structural damage. It was only after an independent air quality test revealed severe particulate concentration in the attic and wall cavities that the scope was corrected. Do not let a visual inspection dictate your settlement for an invisible contaminant.

The HVAC Contamination Gap

The single most undervalued component in a smoke claim is the heating, ventilation, and air conditioning system. When a fire occurs nearby, smoke particles are drawn into your home through vents, gaps, and running HVAC intakes. This essentially turns your ductwork into a distribution network for soot and ash.

Adjusters frequently pay for basic surface cleaning while leaving behind a contaminated HVAC system. If the ductwork, coils, and air handler are not properly assessed, your system will continue to circulate hazardous particulate long after the walls have been painted. A standard insurance estimate might include a few hundred dollars for general duct vacuuming, but professional remediation often requires specialized negative air extraction, evaporator coil replacement, or entirely new ducting depending on the contamination level.

Accepting an estimate that includes surface wiping and basic carpet cleaning without any line items addressing the internal components of the HVAC system.

Pausing the settlement until a licensed HVAC technician conducts an internal assessment of the ductwork and air handler to document soot penetration.

Documenting the HVAC Impact

Do not rely on the insurance adjuster to open up your ductwork. They are generally not licensed HVAC technicians. You need to create a record that the insurer cannot dismiss as speculative.

- 👉 Filter analysis: Photograph your HVAC filters immediately. Heavy soot accumulation on a recently changed filter is primary evidence of system intake.

- 👉 Plenum inspection: Have a technician inspect the supply and return plenums for embedded soot.

- 👉 Coil assessment: Evaporator coils trap sticky smoke residue. If the coils are coated, basic duct cleaning will not resolve the issue.

But the HVAC system is not the only place smoke hides. Once it is pushed through your vents, it settles into areas an adjuster will never see.

Why Insurers Call It Odor When It’s Actually Soot

Smoke residue does not just sit on countertops. It penetrates wall cavities, saturates attic insulation, and embeds itself behind drywall. To limit claim sizes, insurers often play a subtle word game in their estimates: they differentiate between “soot” and “smoke odor.”

In the claims world, adjusters treat soot as a physical substance that requires paid cleaning or removal. They often treat smoke odor as a temporary nuisance that will fade over time. If they cannot physically wipe black soot off your walls, they will classify the damage as odor-only and exclude the cost of replacing porous materials like insulation.

📌 Note: Odor is a physical particulate. If you can smell it inside the house weeks after the fire, the particulate is present in the materials.

To bridge the gap between what is visible and what is actually contaminated, third-party testing is required. This is where an industrial hygienist comes in. An industrial hygienist is an independent environmental health professional who uses scientific sampling to detect hazards. They do not work for the insurance company, and their findings elevate your claim from opinions to scientific facts.

| Testing Method | What It Documents | Why Adjusters Need It |

|---|---|---|

| Air Quality Sampling | Concentration of smoke particulates (PM2.5, PM10) suspended in the indoor air. | Proves that the indoor environment remains hazardous and requires industrial air scrubbing. |

| Surface Swab Testing | Chemical composition of residue on walls, inside cabinets, and inside ductwork. | Confirms that the invisible residue is actually fire-related soot, not standard household dust. |

| Cavity Air Testing | Particulate levels inside wall voids and attics. | Justifies the removal of contaminated insulation and drywall that looks fine on the surface. |

If your home was exposed to heavy wildfire smoke, deploying an industrial hygienist before any remediation begins is a crucial step. Their report is what forces the insurer to address the unseen particulate rather than just the smell, giving you the leverage needed to negotiate a proper scope.

Building the File: How I Advise Documenting the Claim

Before you can successfully dispute a low settlement, you must have the documentation to back it up. When I advise homeowners on building their claim file, I emphasize that you cannot wait for the adjuster to find the damage for you. You have to present them with a fully developed package.

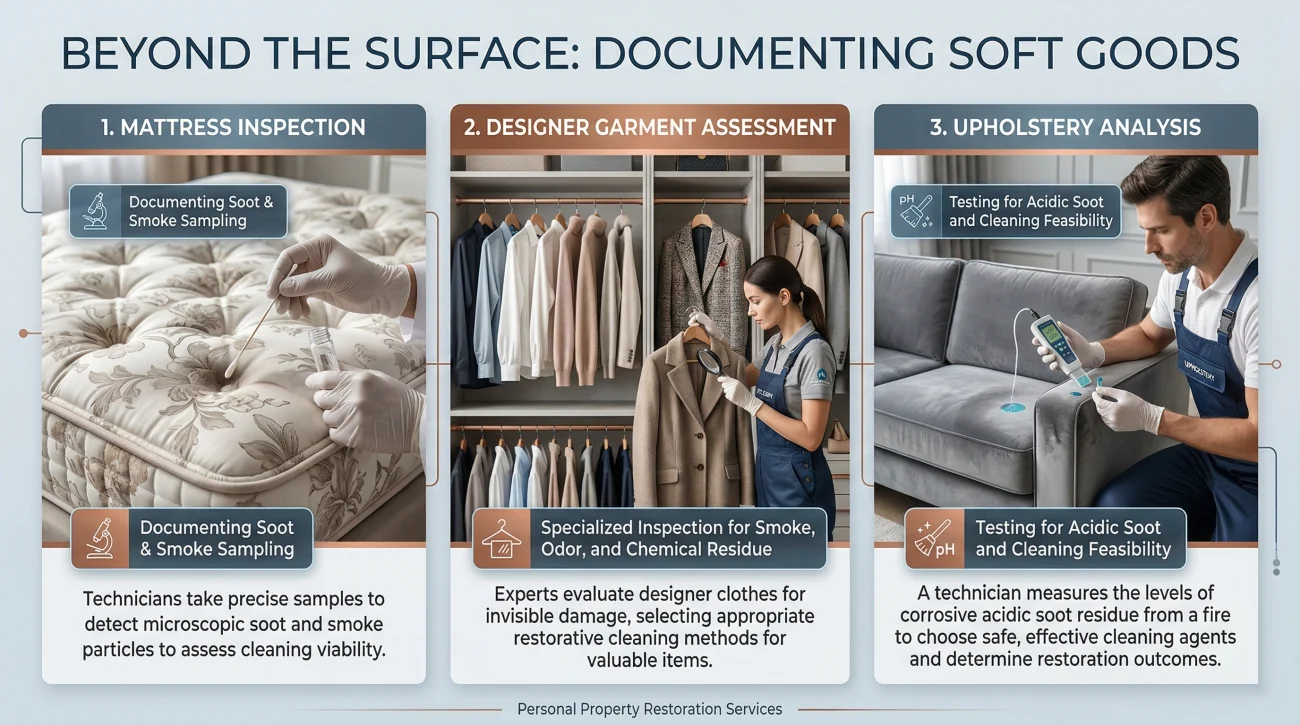

Documenting Personal Property and Textiles

External smoke claims are not just about the structure. Your personal property absorbs smoke heavily. Adjusters often suggest that you simply run your clothes through the washing machine and wipe down your couches. This is rarely sufficient for heavy wildfire smoke.

Textiles, upholstery, and mattresses trap acidic soot particles. Standard laundering can actually set the stain and the smell permanently. You need to document all affected soft goods immediately. Ask a specialized restoration dry cleaner to assess the wardrobe, and request a professional upholstery cleaning estimate. If the items cannot be restored to pre-loss condition using methods like ozone treatment or thermal fogging, they should be claimed as a total loss.

Triggering Additional Living Expenses (ALE)

Many homeowners try to tough it out and sleep in a smoke-filled house. This is often a difficult position financially, but from a claims standpoint, if you stay in the home, the insurer will argue it is habitable. If the air quality makes the home unlivable, you must document your symptoms (headaches, respiratory irritation) and relocate.

High PM2.5 levels detected by an air quality monitor or confirmed by a hygienist are a direct trigger for your policy’s Additional Living Expenses coverage. This pays for your hotel or temporary rental while the home is being properly mitigated.

The Secondary Water Intrusion Risk

If the fire was at an adjacent property, be aware of the water used by the fire department. Millions of gallons of water can run off into your yard, crawlspace, or basement. When I review neighbor-fire claims, I always check if secondary water damage was documented alongside the smoke. If moisture sat in your crawlspace for days while you were evacuated, you might be facing a mold issue as well. If this happens, reviewing the mold claim process becomes just as important as the smoke mitigation.

The Cosmetic Characterization Dispute

Once you have gathered your documentation and testing results, you will likely face the final hurdle: the cosmetic characterization. Insurers frequently attempt to label smoke damage as cosmetic to limit their financial exposure. They will argue that the smoke only caused surface staining and does not impact the structural integrity of the home.

If the damage is deemed cosmetic, the insurer only owes you for cleaning the surfaces. But smoke that has penetrated untreated wood framing and fiberglass insulation is structural contamination. The materials themselves have been fundamentally altered by the chemical residue.

The Escalation Sequence: What Happens Next

When you present the hygienist’s scientific report showing that the molecular structure of the smoke has embedded into the insulation, the “cosmetic” argument loses its weight. However, the insurer will not automatically cut a check the next day. Here is the typical sequence of events after you submit your proof:

- The Insurer Reviews: The desk adjuster will take 15 to 30 days to review the hygienist’s report.

- The Pushback: They may send their own preferred vendor (often a standard cleaning company) to give a competing, much lower estimate.

- The Demand for Scope Match: You must insist that their vendor’s estimate matches the exact remediation protocols (like IICRC standards) outlined in your hygienist’s report. They rarely do.

Communication during this dispute phase must be strictly in writing. If the adjuster tells you over the phone that testing was unnecessary or that they are ignoring the report, force them to put that position in writing. Here is a practical script you can use to frame your escalation.

Dear [Adjuster Name],

Attached is the environmental report from [Hygienist Company Name], conducted on [Date]. As the report details, air quality and cavity testing confirm heavy PM2.5 and soot contamination within the HVAC system and attic insulation.

The initial estimate provided by your office addressed only surface cleaning and characterized the damage as cosmetic odor. The attached scientific data confirms this is structural contamination requiring material removal and specialized air scrubbing per IICRC guidelines.

Please review the attached report and provide a revised estimate that addresses the documented contamination within 15 days. If [Insurance Company] intends to dispute these laboratory findings, please provide the specific policy language and the opposing scientific data you are relying on.

Sincerely,

[Your Name]

Signs Your Smoke Damage Claim Is Undervalued

Knowing when to push back is a critical skill during the claims process. Adjusters handle hundreds of files during a wildfire event, and rushed inspections lead to systemic underpayment. If you are experiencing frustration, recognizing the patterns of an incorrect scope is vital.

Your smoke damage claim is likely undervalued if you notice any of these red flags:

- The adjuster assessed surface staining only and did not recommend or approve an HVAC internal inspection.

- The settlement covers basic wiping and repainting but ignores the attic insulation entirely.

- The adjuster used the term “odor removal” instead of “particulate remediation” in their paperwork.

- The insurer explicitly characterized the damage as “cosmetic” without relying on any independent air quality testing.

- You were told to simply buy consumer-grade air purifiers and run them for a few weeks to solve the problem.

- Your personal property estimate offers a small allowance for standard laundry rather than specialized dry cleaning or replacement.

When reviewing home insurance claims by damage type, external smoke events consistently show the largest gap between the initial offer and the final settlement. If you are seeing these red flags, having a public adjuster review the smoke damage scope before you accept the final settlement is one of the safest ways to protect your property.

Final Steps to Protect Your Property

Recovering from an external smoke event requires patience and strict documentation. Because the damage is airborne and largely invisible, the burden falls on you to prove the severity of the contamination.

Always prioritize independent testing over visual assumptions. Secure your environmental report, ensure your HVAC system is thoroughly inspected, and maintain a paper trail of every request you make. Most importantly, do not sign a final “Proof of Loss” document or a full release of claims until you are completely confident the scope captures all hidden damage. Stand firm on the data. A properly documented claim file is your best defense against cosmetic characterizations and undervalued settlements. Gather your evidence, confirm your coverages, and do not hesitate to escalate the claim if the proposed scope fails to restore your home to a safe, breathable condition.

❓ FAQ

🔥 Does homeowners insurance cover smoke damage from a neighbor?

In most standard policies, yes. Smoke is typically a named peril. If a neighbor’s house catches fire and smoke damages your property, your own homeowners policy usually responds to cover the cleanup and remediation.

💨 How do I prove smoke damage for my insurance claim?

Visual proof includes before and after photos of soot on surfaces and HVAC filters. For invisible damage, the most effective proof is a written report from an independent industrial hygienist detailing air quality samples.

👃 Will my policy pay to remove smoke odor?

Yes, removing the odor is part of returning the home to its pre-loss condition. However, true odor removal usually requires structural cleaning, thermal fogging, or ozone treatments, not just surface wiping.

🛠️ Can I clean up smoke damage before the adjuster arrives?

You should mitigate further damage, but avoid doing a deep clean until the adjuster has inspected the property. If you clean away the visible soot before it is documented, the severity of the claim will be underestimated.

🌬️ Does my claim cover HVAC duct cleaning?

If smoke entered the home, the HVAC system was likely contaminated. Your claim should cover professional duct cleaning, coil cleaning, and filter replacement. Severe contamination may cover ductwork replacement.

🛋️ Are my clothes and furniture covered for smoke damage?

Yes, under your personal property coverage. Soft goods absorb smoke heavily and often require specialized restoration dry cleaning. If they cannot be restored, they should be claimed for replacement.

🛑 What do I do if my smoke damage claim is denied?

Request the specific policy language they are using to justify the denial in writing. Bringing in a public adjuster or providing an independent air quality report can force the insurer to re-evaluate the denied claim.

🌲 Are wildfire smoke damage claims handled differently?

The core process is the same, but wildfire claims often face massive delays due to the high volume of localized claims. Insurers may also be more aggressive in labeling wildfire smoke as temporary or cosmetic.

⏳ How long do I have to file a smoke claim after a nearby fire?

Most standard policies require you to file promptly after discovering the damage, often within one year of the event date. Check your policy declarations and confirm with your carrier directly to ensure you meet the deadline.

⚖️ Can an insurance company say the damage is only cosmetic?

They often say this to limit the scope of repairs. You can dispute a cosmetic characterization by providing evidence that the smoke particulate has penetrated porous materials, requiring structural removal rather than just cleaning.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.