- The honest reality: Almost every pros and cons list about public adjusters is written by a public adjuster. This guide provides a neutral assessment of where they actually add value and where they simply cost you money.

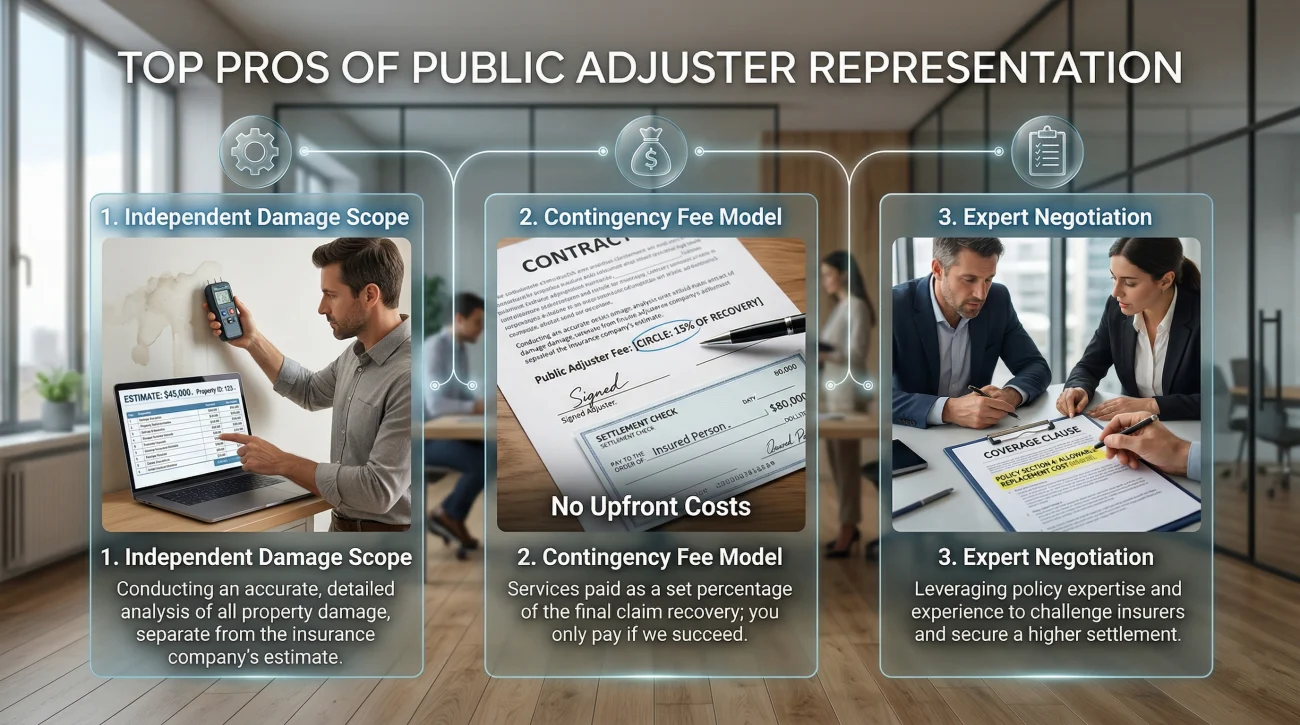

- The biggest pro: They build an independent, line-by-line scope of your damage using industry software. Industry research consistently shows this levels the playing field and often results in higher settlements for complex claims.

- The biggest con: Their contingency fee reduces your net payout. If your claim is straightforward and the insurer’s offer is fair, hiring representation will leave you with less money in your pocket.

- The sweet spot: They are most valuable for large, multi-system losses, hidden damage scenarios, or when there is a massive gap between your contractor’s estimate and the insurance adjuster’s offer.

The Truth Behind the Industry Pitch

If you are researching the pros and cons of hiring a public adjuster, you have probably noticed a glaring pattern. Almost every article you find is published by a public adjusting firm. Unsurprisingly, those articles conclude that hiring their services is universally the best decision you can make.

I have reviewed hundreds of property claims from both sides of the table. I have seen files where a homeowner would have been left with a fraction of what their claim was worth without a professional fighting for them. I have also seen files where a homeowner lost 15% of a perfectly fair settlement simply because they panicked and signed a contract they did not need.

The truth is that their value is absolutely real, but it is not universal. It depends entirely on the specific facts of your claim, the complexity of your damage, and the initial posture of your insurance company.

In this guide, we are going to walk through an honest, unfiltered assessment of the advantages and disadvantages. We will look at the exact scenarios where giving up a percentage of your settlement makes mathematical sense, and the scenarios where it does not. For a foundational look at what this professional actually does before we evaluate their worth, you can review our complete guide to understanding public adjusters.

The PROS: Where Representation Actually Adds Value

Let us start with the advantages. When a claim is large, messy, or disputed, having an independent advocate changes the dynamic entirely. Insurance companies handle thousands of claims a day using highly trained professionals. As a homeowner, this might be your first major disaster. The primary advantage of hiring representation is instantly closing that experience gap.

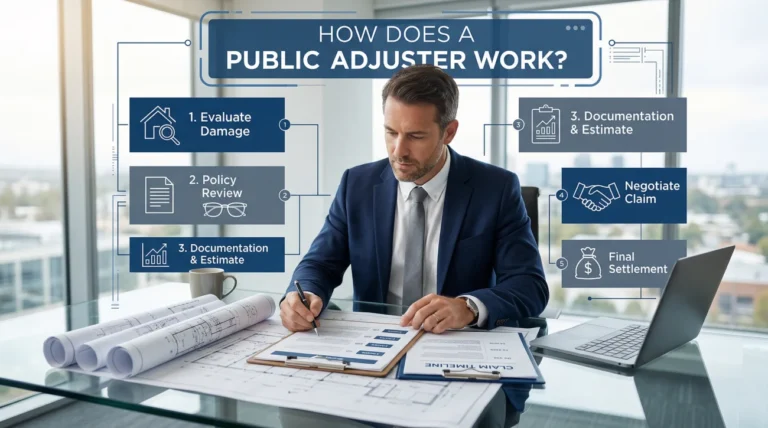

1. The Independent Scope of Loss

This is arguably the single most valuable service provided. When the insurance company’s adjuster visits your home, they write a “scope of loss.” This is a line-by-line estimate of what needs to be repaired and how much it costs. If they miss something, or if they use a cheaper material grade in their software, your settlement drops.

A good representative will conduct their own rigorous inspection, often spending hours finding what the first adjuster missed. They look for hidden moisture behind baseboards, structural deflection in roofing components, and collateral damage to adjacent rooms. They then build a competing scope using Xactimate, the exact same software the insurance carrier uses. Industry research consistently shows that this independent, line-by-line documentation process frequently results in higher net payouts for complex claims.

In reviewing claim files across hundreds of disasters, the biggest financial leaps do not come from arguing over the price of a single sheet of drywall. They come from the independent scope identifying entirely omitted systems, like the requirement to replace undamaged siding on three walls just to create a continuous, matching appearance.

2. The Contingency Fee Structure

Recovering from a disaster is incredibly expensive. Most homeowners do not have the liquidity to pay a professional an hourly rate to fight their insurance company for six months. The contingency fee model solves this.

Because they are paid as a percentage of the settlement, there are zero upfront out-of-pocket costs for you. This structure also answers the most common homeowner fear: what if the public adjuster does not recover any more money than the insurer already offered? Under a standard contingency model, you generally owe them nothing for the attempt. You can read more about how these calculations work in our deep dive on public adjuster fee structures.

3. Professional Negotiation and Emotional Distance

A severe house fire or a catastrophic flood is deeply traumatic. Homeowners dealing with a total loss are often exhausted, emotional, and vulnerable to accepting the first check just to get the nightmare over with. Insurance adjusters know this.

A professional steps in and removes the emotion from the transaction. They handle the endless emails, the requests for more documentation, and the frustrating phone calls. They speak the specialized language of policy endorsements, depreciation schedules, and building codes. When the insurance company says “we do not pay for that,” the professional knows exactly which policy clause proves that they actually do.

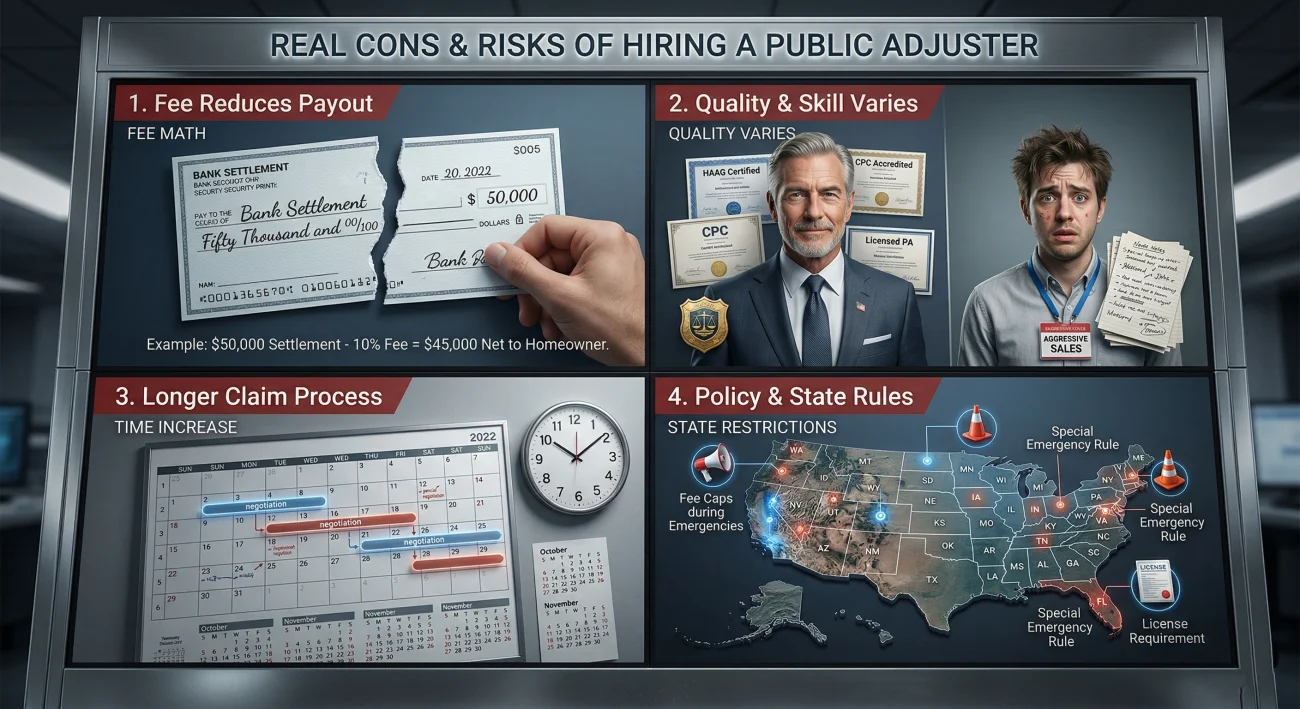

The CONS: The Honest Drawbacks You Need to Know

Now we must look at the disadvantages. This is the section most industry websites conveniently omit. Hiring representation is a financial transaction, and it comes with real costs, risks, and trade-offs that you must weigh carefully.

1. The Fee Reduces Your Net Payout

This is the most obvious but critical drawback. Any fee you pay comes directly out of your repair budget. If your claim is relatively straightforward, the insurer might have paid you the correct amount anyway. In that scenario, bringing in a professional simply costs you money without adding value.

Let us look at a practical example of how the math impacts your bottom line.

| Scenario | Insurer Offer | Final Settlement | PA Fee (15%) | Your Net Payout |

|---|---|---|---|---|

| The Bad Deal (Little Added Value) | $20,000 | $21,000 | $3,150 | $17,850 (You lost $2,150) |

| The Good Deal (High Added Value) | $20,000 | $45,000 | $6,750 | $38,250 (You gained $18,250) |

As the table shows, the math only works in your favor if the professional can identify and recover significantly more than the insurer initially offered. For a deeper breakdown of how different percentage models calculate this split, review our guide on how much a public adjuster actually costs.

2. Quality Varies Significantly

Holding a state license does not guarantee competence. The industry has incredibly skilled, ethical advocates who previously worked as executive adjusters for major insurance carriers. The industry also has aggressive salespeople who sign as many contracts as possible, write sloppy estimates, and rarely communicate with their clients.

A highly experienced advocate and a brand-new, inexperienced one often charge the exact same contingency percentage, but they will produce vastly different results for your home.

Acts as a middleman. Simply takes your contractor’s estimate, forwards it to the insurance company, and demands their 10% cut without adding any independent documentation or policy arguments.

Acts as an investigator. Utilizes advanced diagnostic equipment, brings in structural engineers, writes a detailed 40-page independent scope, and argues coverage based on your specific policy language.

3. The Process Takes Longer

If you want a check deposited in your bank account by next Tuesday, do not hire representation. Involving a third-party professional almost always extends the timeline of the claim.

Instead of accepting the initial offer and moving on, your representative will demand re-inspections, submit lengthy supplements, and engage in weeks (sometimes months) of back-and-forth negotiation. While this delay is often necessary to secure a fair payout, it requires you to live in a damaged home or temporary housing for a longer period.

4. State Restrictions and Caps

Some states place specific restrictions on how these professionals can operate. In certain jurisdictions, they are prohibited from handling specific types of claims or are capped by statute on the maximum fee percentage they can charge during a declared state of emergency. Navigating these rules requires you to do your own due diligence before signing a contract.

Comparing Your Options: PA vs. DIY vs. Attorney

Before looking at specific damage scenarios, it helps to see exactly where a public adjuster fits into the broader landscape of claim management. Here is how the three main paths compare.

| Option | Best For | Cost Structure | Timeline Impact |

|---|---|---|---|

| DIY (You + Contractor) | Straightforward claims, single-system damage, fair initial offers. | Free ($0) | Fastest resolution. |

| Public Adjuster | Complex damage, hidden issues, severe scope or pricing disputes. | Contingency (typically 5 to 20% of settlement). | Adds weeks to months for negotiation. |

| Claim Attorney | Full coverage denials, bad faith tactics, legal disputes. | Contingency (often higher percentage) or hourly. | Longest (can take years if litigated). |

Note that if your claim involves full coverage denials or bad faith tactics, those issues fall entirely outside a public adjuster’s scope. For those specific legal disputes, review our full comparison of public adjusters vs. attorneys to understand that separate path.

When the Value is Highest (The Sweet Spots)

Understanding the general pros and cons is helpful, but applying them to your specific situation is what matters. Based on hundreds of claim audits, here are the scenarios where hiring representation consistently yields the highest return on investment.

- Large or Complex Losses: If your home suffered a major fire, a massive tree impact, or a multi-story water leak, the scope of work is massive. Rebuilding multiple systems (plumbing, electrical, structural, cosmetic) requires a level of estimating precision that homeowners simply do not possess.

- Hidden Damage Suspected: Water and smoke are notorious for hiding behind drywall and inside HVAC systems. Insurance adjusters frequently write estimates only for what they can easily see. A professional advocate will demand destructive testing to uncover the true extent of the loss.

- The Unusually Fast Offer: If an insurance adjuster spends 15 minutes walking through your heavily damaged home and emails you a settlement offer the very next morning, be highly suspicious. Fast offers are almost always low offers. They rely on you taking the quick cash.

- The Contractor Gap: You received a detailed repair quote from a reputable, local general contractor for $60,000. Your insurance company sends an estimate for $22,000. When that gap is massive, a professional negotiator is usually required to bridge it.

- The Post-Settlement Discovery: You accepted an initial ACV check, but your contractor just tore down the drywall and found extensive hidden rot. If you have not signed a final legal release, you may still have options. Our guide on when to hire a public adjuster explains these late-stage windows.

When the Value is Lowest (When to DIY)

Just as there are sweet spots, there are dead zones. These are the situations where I strongly advise homeowners to handle the claim themselves.

- Small Claims Close to the Deductible: If a windstorm blew off a few shingles and the total repair cost is $3,500, but your deductible is $2,000, your net claim is only $1,500. Deducting another 15% fee from that small amount makes no financial sense.

- Single-System Alignment: Your water heater leaked and ruined the laminate floor in one room. Your contractor quotes $4,000 to fix it. The insurance company offers $3,800. The gap is too small to justify giving up a percentage of the total.

- The Insurer Agrees Completely: In some cases, the insurance adjuster is thorough, fair, and writes an excellent scope that matches your contractor’s bid exactly. If the insurance company is doing the right thing, sign the paperwork and start your repairs.

⚠️ Warning on Contractor Negotiations: You might be tempted to let your roofer or restoration company negotiate with the adjuster to save the public adjuster fee. Be very careful. In most states, it is illegal for a contractor to act as an unlicensed adjuster and argue policy coverage on your behalf. They can provide repair estimates, but they cannot legally negotiate the claim.

Signs You Are in a Scenario Where Representation Matters

Deciding whether to take on the cost of a fee comes down to recognizing the warning signs that your claim is going off the rails. It is rarely a clear-cut mathematical formula on day one. Instead, you have to look at the behavioral patterns of your insurance company.

You are likely in a scenario where the pros outweigh the cons if you notice these specific red flags:

- Your home suffered major, multi-room damage, but the field adjuster spent less than 90 minutes inspecting the property before leaving.

- You received a settlement offer within a few days of the inspection, and it feels incredibly rushed.

- Your licensed general contractor’s estimate to rebuild is more than 20% higher than the insurance company’s settlement offer, and the insurer is refusing to negotiate.

- Multiple damage types are present (e.g., water damage and subsequent mold), but the settlement only addresses the primary issue and ignores the secondary damage.

If you are experiencing any of those patterns, the risk of managing the claim on your own is generally much higher than the cost of a contingency fee. The honest answer is that value depends almost entirely on your specific claim facts, and those specifics are exactly what a professional evaluation uncovers.

To get a personalized answer on whether a professional is right for your exact situation, rather than just reading a general list of pros and cons, take the time to get a free claim review to see if involvement makes mathematical sense.

How to Pause Your Claim While You Decide

If you are not ready to commit to a professional review just yet, you still need to protect your position. Your insurance adjuster might be pressuring you to sign a proof of loss or accept an initial check while you are actively weighing these pros and cons. You have the right to review your options. Here is a simple, professional way to buy yourself time without abandoning your claim.

Hello [Adjuster Name],

I have received your initial estimate and the undisputed settlement check. I am currently in the process of reviewing this estimate alongside quotes from local restoration contractors.

Because there appears to be a significant difference in the scope of repairs required, I am evaluating whether I need to retain a professional to assist me in documenting the remaining damage.

I will contact you within the next 7 days once my review is complete to discuss the supplement process.

Thank you,

[Your Name]

Buying yourself this extra week gives you the breathing room needed to make the final call on representation.

Final Thoughts on Making Your Decision

Hiring an advocate is not a magic wand; it is a strategic transfer of leverage. You are trading a percentage of your settlement and accepting a longer timeline in exchange for professional scope documentation and policy enforcement. If your insurance company is playing fair on a straightforward loss, keep your money. But if you are facing a massive gap between the actual damage and the adjuster’s offer, that contingency fee is often the necessary price of a complete recovery.

❓ FAQ

⚖️ Are public adjusters worth it for every claim?

No. They are generally not worth the fee for small, straightforward claims or situations where the insurance company’s initial offer already matches your contractor’s estimate.

📈 Do public adjusters increase claim payouts on average?

Yes. Independent industry research consistently shows that represented claims, especially complex or catastrophic ones, result in significantly higher settlements on average compared to unrepresented claims.

💰 Are public insurance adjusters worth the money they charge?

They are worth the money if the additional funds they uncover in your policy and estimate far exceed the percentage they take as their fee. A free initial review usually clarifies this math.

🤔 Are public adjusters a good idea if I already have a contractor?

Yes, because contractors are legally restricted in most states from negotiating insurance policy language on your behalf. An advocate handles the coverage dispute so the contractor can focus on the actual repairs.

🛑 Are public adjusters good or bad for the timeline of a claim?

They typically extend the timeline. Because they demand re-inspections and refuse to accept low initial offers, the negotiation process takes longer, though it often yields a more accurate result.

📊 How much can a public adjuster increase a settlement?

It varies wildly based on how poorly the insurer’s initial adjuster performed. In cases of severe underpayment, it is not uncommon to see settlements double or triple once a proper independent scope is submitted.

💵 Do I have to pay out of pocket for their services?

Usually, no. They operate on a contingency fee model, meaning their payment is deducted directly from the final settlement check issued by the insurance company.

✅ Is it better to use a public adjuster before or after filing?

Bringing them in before filing is the strongest position, as they can control the narrative and documentation from day one. However, most homeowners successfully hire them after receiving a low initial offer.

🛠️ Do public adjusters really help with hidden water damage?

Yes. They utilize specialized equipment like thermal imaging cameras and moisture meters to document water damage behind walls that standard insurance adjusters frequently miss or ignore.

📝 Can I cancel the contract if I change my mind?

Most regulated states require a specific rescission period (often 3 to 5 days) during which you can cancel the contract without penalty. Always verify this clause before signing.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.