- The best time to hire a public adjuster is often before you even file the claim, allowing for a professionally documented scope from day one.

- Cashing an initial ACV check is typically not the same as closing your claim; you often still have a window to claim RCV supplements or additional damage.

- It is generally only “too late” if you have signed a full, final release of all claims or if your policy’s filing deadlines have completely expired.

The Timing Paradox: When Does Hiring a Public Adjuster Make Sense?

In my years of reviewing property claims, I have noticed a recurring pattern: most homeowners wait until they are frustrated, exhausted, and holding a lowball check before they even consider professional help. While a public adjuster can often help at that stage, it is not always the most efficient path. The timing of when you bring in an expert is one of the biggest variables in how your claim unfolds.

I often tell people that hiring a public adjuster is like hiring a guide for a trek through a wilderness you have never visited. You can call the guide when you are already lost and out of supplies, or you can have them lead the way from the trailhead. Both options work, but one is significantly less stressful. In the insurance world, being proactive is the only way to maintain leverage over a process that is designed by professionals, for professionals.

I once worked with a homeowner who had struggled for six months on a fire claim. By the time I saw the file, the insurer had already ‘closed’ it three times. We eventually got a fair settlement, but we had to undo months of documentation errors that could have been avoided in the first week.

Understanding when the window of opportunity is open and when it has actually slammed shut is critical for your financial recovery. Most homeowners overestimate how much power the insurance company has to “close” a claim permanently. Here are the three distinct windows where hiring a public adjuster makes the most sense and what each one means for your final settlement.

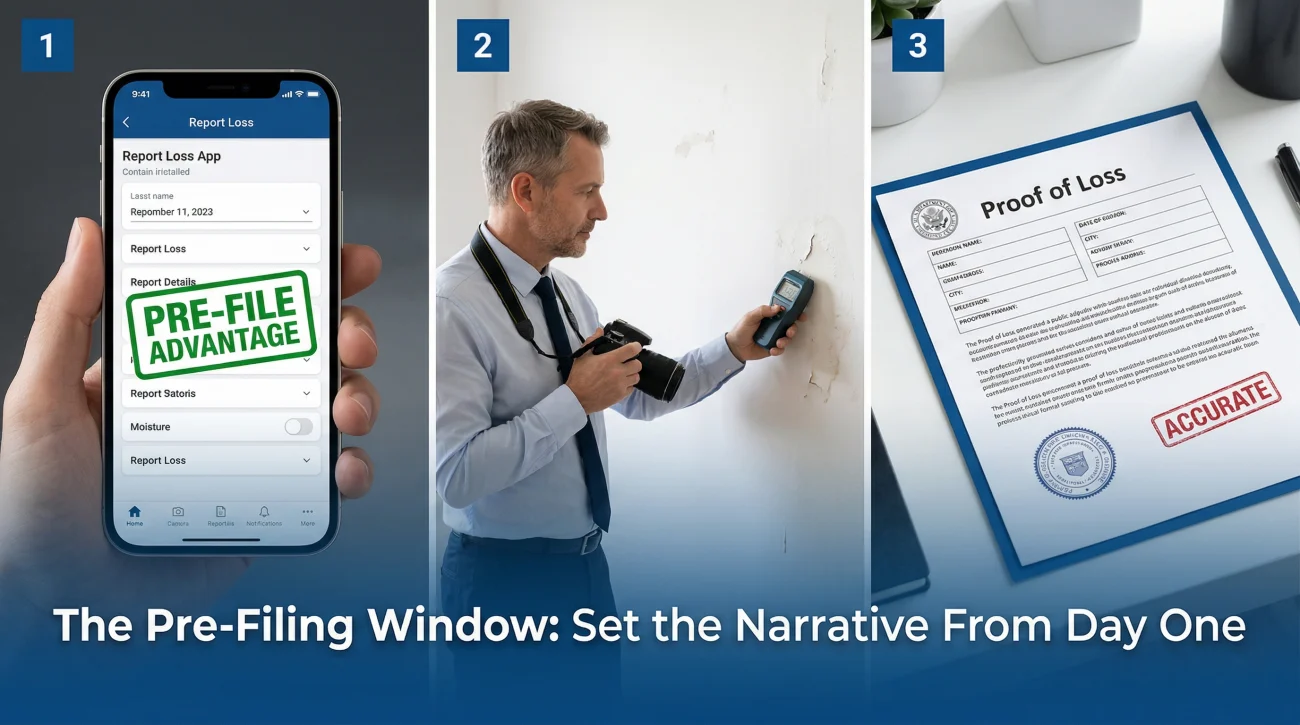

Window 1: Before Filing the Claim

This is the strongest position you can be in. Bringing in a public adjuster before you pick up the phone to call your insurance company allows you to set the narrative from the very first minute. Instead of the insurer’s adjuster being the first person to define the scope of damage, your own expert does it first.

When a public adjuster manages the claim from day one, they prepare a professional Proof of Loss and a detailed line-item estimate using industry standard software. This forces the insurance company to respond to your data rather than you trying to find errors in theirs later. For context on how this fits into the overall journey, you can see our guide on how the home insurance claim process works from a professional perspective.

I’ve seen the ‘Pre-Filing Advantage’ in action many times. On a recent pipe burst claim, the homeowner called me before filing. I attended the initial inspection with the insurer’s adjuster. By pointing out hidden moisture in the subfloor and insulation that the adjuster initially overlooked, the very first estimate was $12,000 higher than it likely would have been otherwise.

The primary benefit here is accuracy. When you file a claim yourself, you might describe the damage as “water in the kitchen.” A public adjuster will describe it as “Category 3 water intrusion affecting 150 square feet of hardwood subflooring, requiring professional mitigation and structural drying.” The difference in those two descriptions can mean thousands of dollars in the initial reserve the insurance company sets aside for your claim.

Sample Script: Notifying the Carrier of PA Representation

This window is especially vital for large-scale losses, such as a house fire or significant hurricane damage, where the initial documentation will dictate the settlement for months to come. If the foundation of the claim is built correctly, there is less friction in the later stages of the supplement process.

Window 2: During the Active Claim

This is the most common time homeowners seek help. You have filed the claim, the insurer’s adjuster has visited, and perhaps you have received an initial estimate that feels far too low. You are mid-stream, and the current is pulling you toward a settlement that will not cover your contractor’s quotes.

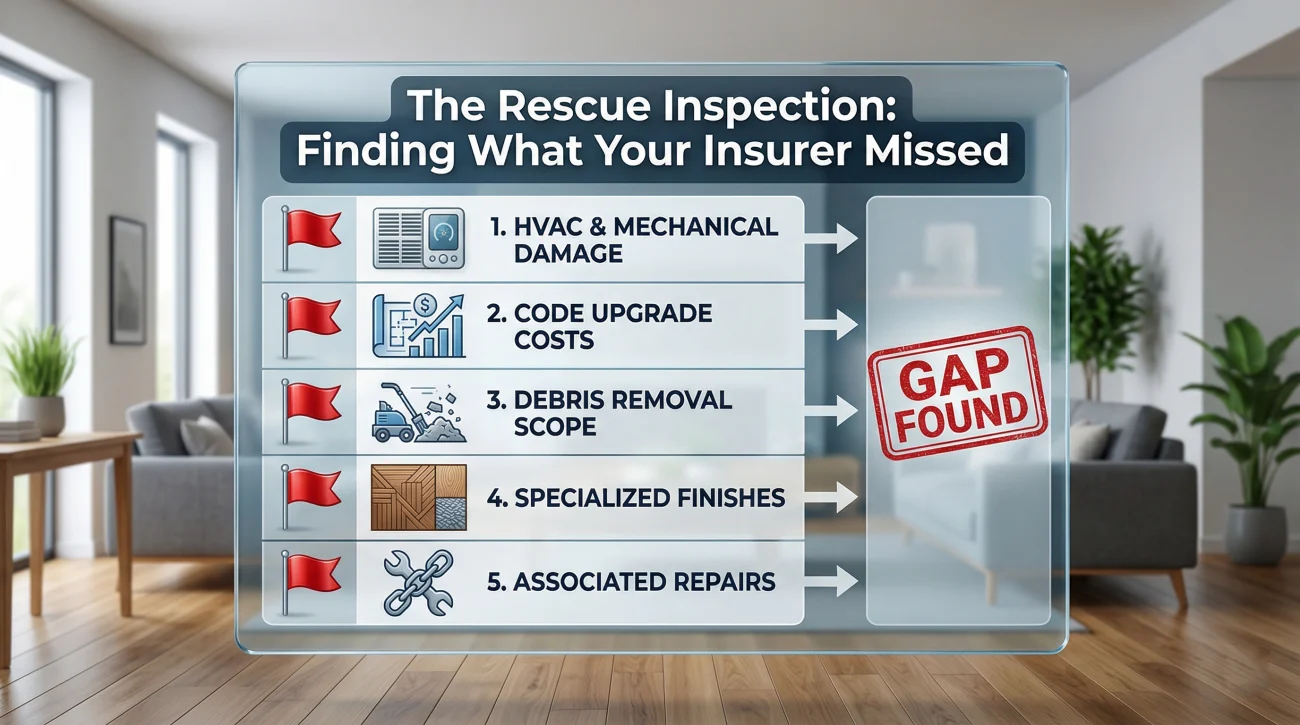

In this window, a public adjuster conducts a “Rescue Inspection.” They go behind the insurer’s adjuster to find the missed line items that frequently cause a gap between the insurance offer and a contractor’s reality. From my experience in the field, insurer estimates often focus on the most visible damage while ignoring the systemic repairs required by local building codes or industry standards.

The Rescue Inspection Checklist

A quality public adjuster doesn’t just look for what is broken; they look for what is required to make the home whole again. Common items I find missed during these mid-claim inspections include:

- 📍 HVAC and Mechanical Damage: Smoke or water particles that require professional cleaning or component replacement that a visual inspection misses.

- 📍 Code Upgrade Costs: The cost to bring old wiring, plumbing, or roofing materials up to current local building codes as required by law.

- 📍 Debris Removal Scope: Underestimating the sheer volume and specialized labor cost of removing damaged hazardous materials.

- 📍 Specialized Finishes: Custom trim, high-end paint finishes, or non-standard moldings that the adjuster priced as basic “contractor grade” materials.

- 📍 Associated Repairs: The cost to detach and reset cabinets or appliances to properly replace the flooring underneath them.

Trying to negotiate with the insurer yourself for months, only calling a PA when the insurer stops responding or provides a final “take it or leave it” offer.

Calling a PA the moment you see a significant, unexplained gap between your contractor’s quote and the insurer’s estimate.

If you are weighing whether the cost is worth it at this stage, I recommend reviewing the honest pros and cons of public adjusters to see how the fee structure might impact your net recovery. In many cases, the “delta” or the increase the PA finds is so significant that the fee is easily absorbed by the higher settlement.

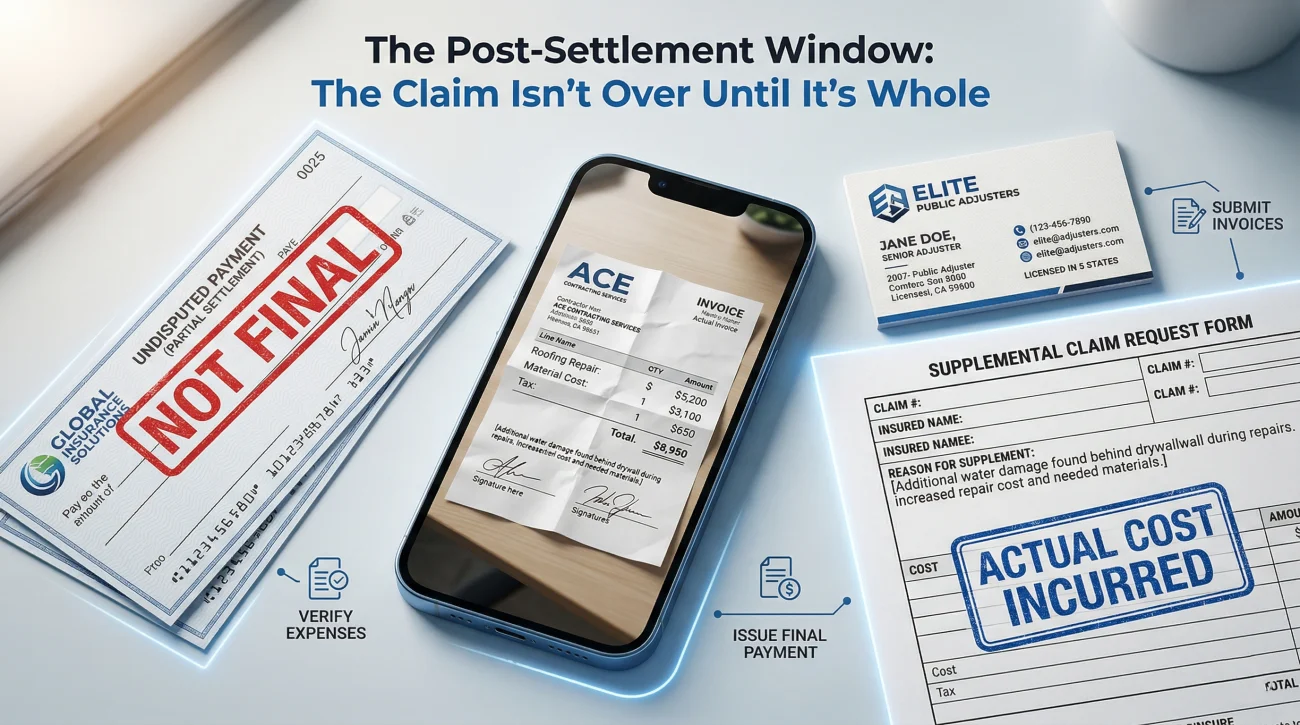

Window 3: After the Settlement Offer

This is the “emergency room” of insurance claims. You have a check in your hand, but it is not enough to even start the repairs. Many homeowners believe that once a check is issued and cashed, the claim is over and the file is locked. In most cases, this is a misconception that costs people thousands of dollars. Standard policies often use a two-check system: an initial payment followed by a later supplement for depreciation or hidden damage.

In this window, a public adjuster reviews the scope of the settlement line by line. If you have not signed a document formally releasing the insurer from further liability, the claim is technically still open for supplements. The adjuster can identify underpriced items, incorrect measurements, and missed labor costs, then file a supplemental claim to bridge the gap. Understanding the definition and role of a public adjuster is the first step in realizing they are negotiators who can reopen these doors.

Field Observation: I once met a homeowner who thought his roof claim was dead because it had been closed for over a year. He had only received the initial ACV (Actual Cash Value) payment. After reviewing his specific policy deadlines, we found he was still within the window to claim the RCV (Replacement Cost Value) supplement. We documented the completed work and recovered an additional $6,000 he didn’t even know existed.

This stage requires a very specific documentation strategy. You are no longer just arguing about what *might* be damaged; you are documenting what the repairs actually cost. A public adjuster uses the “Actual Cost Incurred” to hold the insurance company accountable to the Replacement Cost provisions of your policy.

The Anxiety of the Stalled Claim

There is a specific kind of stress that comes when you realize your insurance claim is not going to cover your repairs. You might be weeks or months into the process, living with temporary fixes, and feeling the pressure to just “sign the papers and move on” so you can have some peace of mind. The insurance company knows this. Sometimes, the delay itself is a tactic used to make you more willing to accept a low offer just to get the process over with.

I see homeowners every day who feel they have already waited too long, or that by arguing now, they will only delay the repairs further. This anxiety often leads to the mistake of cashing a final settlement check or signing a release before they have confirmed the scope is actually complete. You feel like the door is closing, and you are scrambling to get whatever you can. If you are feeling that pressure to settle just to end the headache, that is exactly when you need to pause and seek a professional second opinion. Most of the time, the door isn’t closed; it’s just being held shut by the carrier.

How to Determine if the Timing is Worth the Fee

One of the most common reasons homeowners hesitate to hire a public adjuster late in the game is the concern that the fee will eat up too much of the remaining settlement. This is a valid concern, and it requires a quick “Net Gain” calculation. A public adjuster should be able to look at your current estimate and tell you if they see enough “missed scope” to justify their involvement.

For example, if the insurance company offered you $20,000 and your contractor says it will cost $35,000, there is a $15,000 gap. If a public adjuster charges a percentage of the total recovery but finds $18,000 in additional damage, your net payout after the fee will still be significantly higher than the original $20,000 offer. If the gap is only $1,000, hiring a professional might not make financial sense.

| Claim Stage | Leverage Level | Primary Goal of PA |

|---|---|---|

| Pre-Filing | Highest | Establish correct scope and prevent initial lowballing. |

| Active Dispute | Medium | Identify missed items and negotiate the supplement gap. |

| Post-Settlement | Low but Viable | Recover depreciation and document hidden damage found during repair. |

The “Is It Too Late” Reality Check

I get asked “is it too late to hire a public adjuster” more than almost any other question. The answer usually depends on what you have signed, not what you have cashed. Insurers often have more room for negotiation than they let on, and most policies provide a longer window for supplemental claims than homeowners realize. The key is distinguishing between an undisputed payment and a final settlement.

Cashed Check vs. Signed Release

In most standard homeowners policies, cashing an initial settlement check does not automatically waive your right to ask for more money later. This check is usually an undisputed payment of what the insurer admits they owe. However, you must be extremely careful about what you sign when you receive that check. Look for “Red Flag Phrases” on your settlement documents such as:

- 📍 “Final and complete settlement of all claims”: This phrase suggests that by accepting the funds, you are giving up your right to any future supplements.

- 📍 “Waiver of all future claims related to this event”: This is a clear indicator that the insurer is trying to close the file permanently.

- 📍 “Full and final release”: Often found on a separate document, this is the most restrictive language in a claim.

The RCV Supplement Window

If your policy has Replacement Cost Value coverage, you are typically entitled to a second check for the depreciation the insurer withheld. There are strict deadlines for this, often ranging from 180 to 365 days from the date of the loss. A public adjuster can step in to ensure that every dollar of that depreciation is recovered, provided the deadline has not passed. If you are currently holding a check, check out our breakdown of how public adjuster fees work to see if a late-stage intervention makes sense for you.

While the windows are wider than most people think, they do eventually close. It is critical to recognize the moment when the door is truly locked so you don’t waste time on a claim that cannot be recovered.

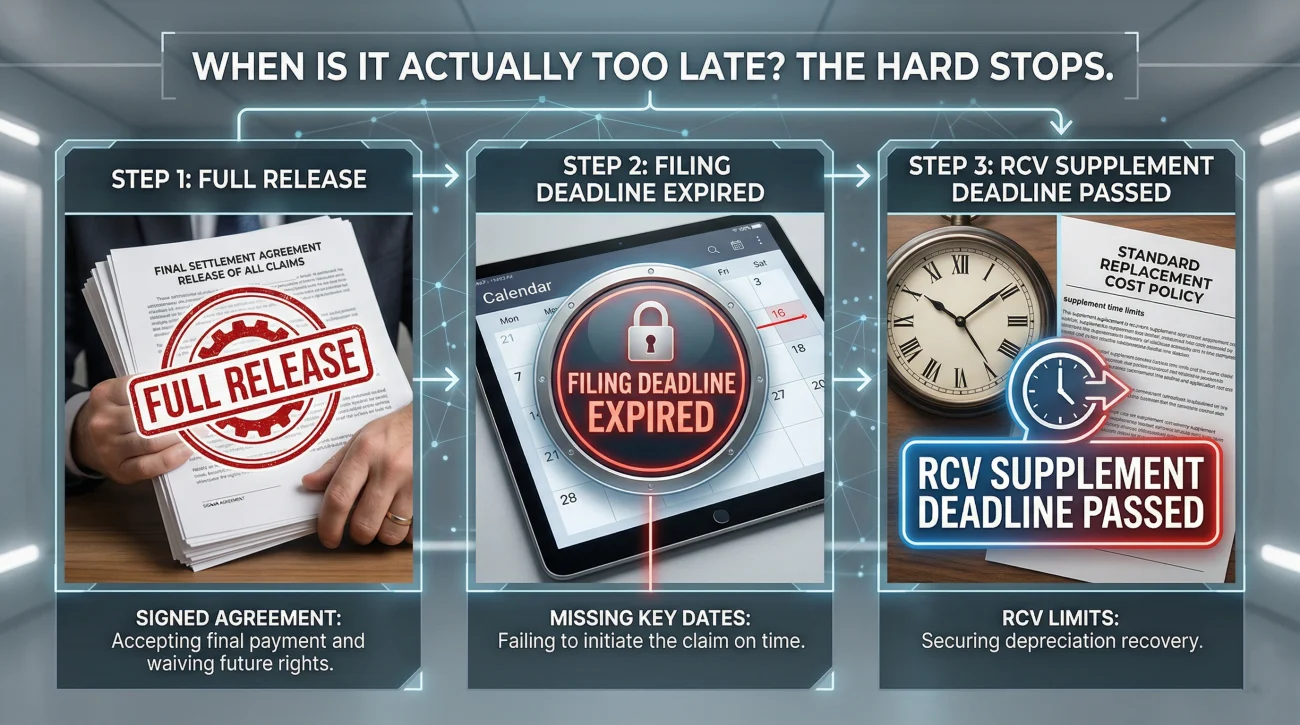

When Is It Actually Too Late?

There are three specific scenarios where a public adjuster generally cannot help you anymore, regardless of how much damage was missed. These are the “hard stops” of the claims world:

- 📍 You signed a Full Release of All Claims: This document confirms that the payment you received is the final settlement and waives your right to claim further related to the specific loss event. Once this is signed and notarized, it is very difficult to undo.

- 📍 The filing timeframe has expired: Most policies and claim agreements include a specific timeframe for how long you have to reopen a claim or report new damage. There is a point at which the practical window for seeking more funds closes entirely.

- 📍 The RCV Supplement Deadline has passed: If your policy gives you one year to complete repairs and you are now in year two, that depreciation money is usually gone unless you received a written extension before the deadline hit.

📌 Note: If you are unsure whether you signed a Full Release or just a Proof of Loss, you should have your documents reviewed. They look very similar to the untrained eye but have vastly different consequences for your claim’s future. A Proof of Loss is just a sworn statement of damage; a Release is a contract to stop asking for money.

Final Takeaway on PA Timing

The best time to hire a public adjuster was yesterday; the second best time is today. While “too late” is often much later than homeowners assume, your actual window for recovery depends entirely on the documents you have signed and the specific deadlines buried in your policy language. Do not take the insurance company’s word for it when they say a file is closed.

Always communicate in writing, keep copies of every document you sign, and be proactive in your follow-ups. A professional review can identify if there is still a path forward, even if the insurer says the file is closed. To get a clear answer on whether your claim still has room for recovery, I recommend getting a free review to see if your claim can still be salvaged by a licensed professional.

If you are still in the early stages of deciding or if you have just begun the process, reading through the step-by-step public adjuster process can help you visualize what the next few weeks will look like once you bring in an expert to lead the way.

❓ FAQ

💸 Can I hire a public adjuster after I already cashed the insurance check?

Yes. In most cases, cashing a check for the undisputed amount does not close your claim. As long as you did not sign a document formally releasing the insurer from further liability, you can usually still seek a supplement for missed items or hidden damage found later.

⏳ How late in the claim process is it too late to hire a PA?

It is typically too late only if you have signed a final settlement release or if the filing deadlines in your policy have fully expired. Most homeowners have more time than they realize to seek additional funds.

🏠 Should I hire a public adjuster before or after the insurer’s adjuster visits?

Hiring a public adjuster before the insurer visits is ideal. This ensures that your own expert is present to identify damage and document the scope correctly from the very beginning, preventing errors before they happen.

📉 Can a public adjuster help if my claim was already denied?

Yes, provided the denial was based on a scope or characterization issue. A PA can provide the professional documentation needed to challenge an insurer who calls sudden damage “gradual” or maintenance-related.

📅 Is there a deadline for claiming the RCV depreciation check?

Yes. Most policies require you to complete repairs and submit proof within a specific timeframe, often 180 or 365 days. A public adjuster can help you track these critical deadlines so you don’t leave money on the table.

🖊️ What happens if I already signed a contract with a contractor to handle the claim?

Licensing laws in many areas prohibit contractors from acting as public adjusters. You can still hire a licensed PA to handle the actual negotiation, but you should check your contractor’s agreement for any cancellation fees.

🚶 Can I fire a public adjuster if I hire them too late and they can’t help?

Most public adjuster contracts have a short rescission period (usually 3-5 days). After that, you can usually terminate the agreement, but you may owe a fee for the professional work already performed on your behalf.

🛑 Does a public adjuster make the claim process take longer?

A public adjuster may initially extend the timeline due to their thorough inspection and negotiation. However, this often prevents the long cycles of appeals and re-openings that haunt poorly documented claims later on.

👔 Can I hire a PA just for the final negotiation part?

Yes. Many homeowners bring in a public adjuster only after they have reached an impasse with the insurer. This is often referred to as a supplemental claim engagement and is a very common scenario.

🌊 Is it too late to hire a PA for a flood insurance claim?

Flood claims (NFIP) have very strict deadlines for the Proof of Loss. If you miss that specific deadline, it is much harder for a PA to help, though it is not always impossible depending on the circumstances.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.