- Public adjusters work on a contingency fee model, meaning they take a percentage of your final settlement and require zero upfront payment to start working on your claim.

- The most critical financial detail in any agreement is whether the fee percentage is applied to your entire total settlement or only to the new money the adjuster recovers above your insurer’s initial offer.

- Fee percentages typically range from 5 to 20 percent, but many states strictly cap these rates, especially following declared weather disasters.

The Reality of Public Adjuster Fees

When you are navigating a complicated property damage claim, hiring a professional to handle the insurance company sounds incredibly appealing. The concept of a contingency fee sounds even better. You do not have to write a check out of your own bank account to hire them. However, what that percentage is applied to, and how that calculation affects your actual net recovery, is exactly what most homeowners fail to understand before signing a representation agreement.

In my years of reviewing claim files and settlement documents, I have seen homeowners thrilled with the final numbers and others deeply frustrated by how much of their payout went to professional fees. The difference between those two experiences rarely comes down to the percentage itself. The difference almost always lies in how the fee structure was built into the fine print.

If you are currently evaluating a contract or simply trying to figure out if this path makes financial sense, you need to strip away the sales pitch and look strictly at the mechanics. A public adjuster is a business partner in your claim. Before you agree to share a portion of your rebuilding funds, you must understand exactly how that portion is calculated.

Key Point: A contingency fee sounds simple on the surface. But the base number that the percentage is multiplied against will determine whether your net financial gain justifies the cost of the service.

How the Contingency Fee Model Actually Works

As outlined above, public adjusters operate on a contingency basis. But understanding exactly why this model exists helps explain how it should protect you in practice. After a major loss like a fire or a catastrophic flood, homeowners rarely have thousands of dollars in disposable cash to pay hourly retainer fees to a consultant.

The contingency model removes the upfront financial barrier. More importantly, it shifts the financial risk away from the homeowner and onto the professional. You are not paying for an attempt; you are paying for a result. If a public adjuster takes your case, spends twenty hours building an independent damage scope, argues with the insurance company for a month, and ultimately fails to recover a single dollar above what you were already offered, you owe them nothing.

However, this protection only works if the contract is structured correctly. If you are still trying to figure out the broader role these professionals play in the ecosystem, you can read our foundational guide to understand what a public adjuster actually does. For now, we will focus exclusively on the money.

The Rule Against Upfront Fees

A legitimate, licensed public adjuster will not ask you for a deposit. They will not ask for a retainer. They will not ask you to cover their travel expenses or their software licensing fees.

Typical Percentage Ranges and State Caps

Knowing that you only pay for a successful recovery naturally leads to the most common question homeowners ask: exactly what percentage is normal? The standard range across the industry typically falls between 5 percent and 20 percent of the settlement. That is a massive spread, and the exact number you see on a contract will depend heavily on three variables.

- 1. The size of the claim: A massive commercial fire loss might be billed at 5 percent because the total settlement will be in the millions. A relatively straightforward $15,000 water damage claim will likely be billed at a much higher percentage because the adjuster has to justify their time investment.

- 2. The complexity of the loss: Claims that require deep forensic investigation, structural engineering coordination, or extensive policy interpretation generally command higher fees.

- 3. State statutory limits: This is the most important variable of all.

Pro Tip: Can you negotiate the fee? Yes. Like most professional services, public adjuster fees are often negotiable. If you have suffered a severe total loss (like a home completely destroyed by fire), the potential payout is high enough that you have leverage to negotiate a lower percentage while still offering the adjuster a substantial fee.

How States Regulate Public Adjuster Fees

You should never assume that a quoted percentage is standard without checking your local regulations. A significant number of states heavily regulate these fees by statute to protect consumers from price gouging, especially after major weather events.

For instance, some states impose strict emergency caps that kick in when a state of emergency is declared following a hurricane or wildfire — this emergency limit can differ significantly from the cap allowed during normal operating periods. Other states cap fees at a flat 10 percent across the board, while some allow adjusters to charge whatever the open market will bear.

You must verify the legal fee cap in your specific state before signing anything. You can do this easily by searching the website of your state’s Department of Insurance. If a professional quotes you a 20 percent fee in a state where the legal maximum is 10 percent, that is an immediate signal to walk away.

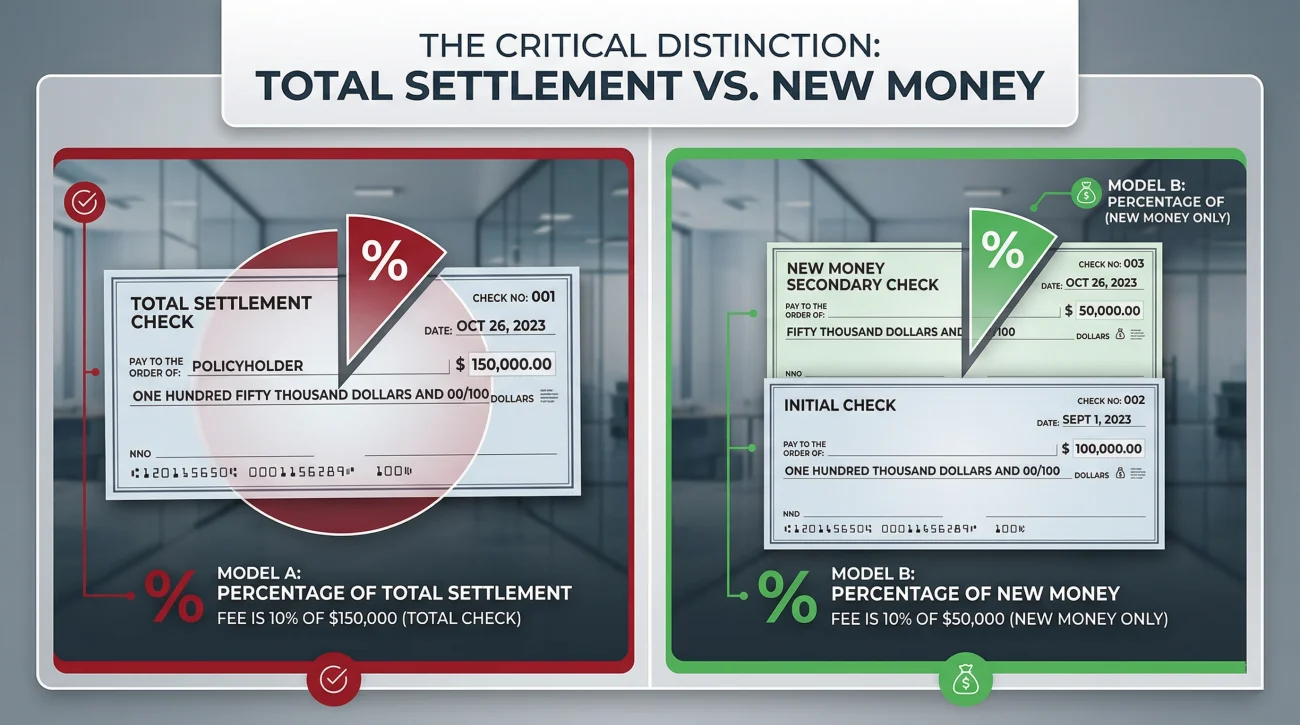

The Critical Distinction: Total Settlement vs. New Money

We now reach the most crucial mechanical detail of public adjuster compensation. This single contract clause will drastically alter how much money actually ends up in your pocket to rebuild your home.

There are two completely different ways a fee percentage can be applied to your claim funds.

Model A: Percentage of the Total Settlement

Under this model, the fee is applied to every single dollar the insurance company pays out for the entire claim. This includes money the insurance company may have already offered you before the adjuster even drove to your property. If the insurance company already cut you a check for $20,000, and the adjuster comes in and finds another $5,000, a “total settlement” contract means the adjuster takes a cut of the entire $25,000.

Model B: Percentage of the Increase (New Money)

Under this model, the fee is only applied to the new recovery. The adjuster takes their percentage exclusively from the funds they successfully negotiated above the insurance company’s prior offer. If you have already received a partial settlement check from your insurer before contacting a professional, that money should be ring-fenced. The fee only applies to the newly recovered funds.

In my field observations, I frequently review cases where a homeowner accepted a total settlement contract without realizing they just agreed to pay thousands of dollars out of an initial payment the insurance company had already approved. The frustration when they realize their adjuster’s fee applies to undisputed money is immense.

The second model inherently aligns the professional’s incentive much more directly with the actual value they add to your situation. You must explicitly ask which calculation model applies before you put your signature on any document.

The Net Gain Math Illustration

To truly understand how these two models behave in the real world, we have to look at the math. Let us assume a concrete scenario.

You file a claim for major kitchen water damage. The insurance company’s initial adjuster inspects the property and issues a settlement offer of $10,000. You know this is entirely too low to replace your custom cabinets. You engage a public adjuster at a 10 percent fee. The public adjuster successfully negotiates an additional $18,000 from the carrier. The final, total settlement is $28,000.

| Calculation Element | Model A (10% of Total) | Model B (10% of Increase) |

|---|---|---|

| Insurance Carrier Initial Offer | $10,000 | $10,000 |

| Public Adjuster Added Recovery | $18,000 | $18,000 |

| Total Gross Settlement | $28,000 | $28,000 |

| Public Adjuster Fee | $2,800 | $1,800 |

| Homeowner Net Funds | $25,200 | $26,200 |

| Net Financial Gain Above Initial Offer | $15,200 | $16,200 |

In both models, hiring the professional was mathematically beneficial. You walked away with significantly more rebuilding funds than the initial $10,000 offer. However, the calculation method changed your final takeaway by a full thousand dollars. The model matters immensely.

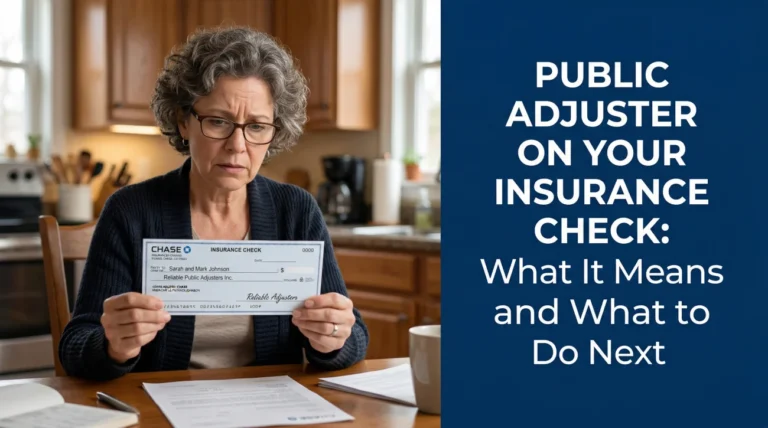

When and How the Adjuster Actually Gets Paid

Understanding the final math is one step. Understanding the physical flow of the money is another. You will not typically write a personal check to your adjuster from your checking account. The fee is deducted from the insurance settlement funds.

When you sign a representation agreement, that document usually includes language granting the adjuster a lien on your settlement proceeds. The adjuster will send a formal letter of representation to your insurance carrier. This legally notifies the carrier that the adjuster has a financial interest in the claim.

When the insurance company finally issues a settlement payment, they will typically print a joint check. This check will have your name, your mortgage company’s name if you have a loan, and the public adjuster’s name all printed on the payee line. This ensures the adjuster’s fee is protected. All parties must endorse the check before the funds can be released and distributed according to the contract. If you want to know more about the protective clauses to look out for during this stage, I recommend reviewing the fine print of the representation agreement in detail.

How Fees Apply to Depreciation Checks

Endorsing the joint check is only part of the cash flow equation. You also have to navigate how that percentage applies to the staggered way insurance companies release funds. Most modern homeowners policies are Replacement Cost Value (RCV) policies. This means the insurance company pays claims in two parts. They issue a first check for the depreciated value of your items, known as Actual Cash Value (ACV). After you complete the repairs and submit the final contractor invoices, the insurer issues a second check for the depreciation holdback.

Your contract will dictate how the fee applies to these split payments. Some adjusters take their full percentage out of the first ACV check, leaving you with less initial cash flow to start repairs. Others take their percentage proportionally as each check is released. You must clarify this cash flow timing before agreeing to terms, as a heavy fee deduction on the first check can make it difficult to afford the initial deposit your construction contractor will demand.

Signs Your Fee Structure Warrants Careful Review

The mechanics of contingency fees are designed to be fair, but poorly drafted contracts can easily tilt the math against you. I regularly sit down with homeowners who are staring at a proposed agreement and feeling uneasy about the financial commitments hidden in the text.

Signs the fee structure in front of you warrants careful review and immediate pushback include:

- 🛑 The contract completely fails to specify whether the percentage is calculated on the total gross settlement or solely on the increase above your prior offer.

- 🛑 The quoted percentage clearly exceeds your specific state’s statutory cap for residential property claims.

- 🛑 The firm demands a non-refundable “retainer” or “administrative setup fee” disguised as a contingency requirement before they will even review your policy.

- 🛑 The percentage is unusually high given the stated size and simplicity of the claim.

If you encounter a professional who becomes defensive when you ask to clarify these calculation methods, that reaction is a massive red flag. A legitimate consultant will gladly walk you through the math and put the specific calculation model in writing.

You can test this simply by sending a direct, written inquiry.

Sample Fee Clarification Question:

“Before I sign the representation agreement, I need to confirm the fee structure in writing. Does your proposed [X]% fee apply to the total gross settlement of the claim, or does it apply exclusively to the new funds you recover above the $[Amount] my insurance carrier has already offered me?”

The Step Before You Sign Any Contract

Do not let the stress of a severely damaged home push you into signing away 15 percent of your rebuilding funds without doing the math first. Engaging professional help only makes sense if there is enough missing money on the table to justify the fee, and that calculation always starts with a thorough review of your specific situation.

If your insurance company’s offer is completely fair and accurate, giving up a percentage of that money will result in a net loss. If the offer is severely lacking due to missed scope or misapplied policy language, the fee is usually a necessary and profitable investment.

A reputable professional will not try to force you into a contract if there is no room to improve your settlement. They will evaluate your initial offer, look at the damage, and give you an honest appraisal of the margins. Before you commit to any fee structure or worry about state caps, you must first determine if there is actually a financial gap to close. While you are weighing the broader public adjuster pros and cons, the most practical next step is getting a free claim review to see if a professional can actually add value to your specific settlement.

❓ FAQ

⚖️ Is a public adjuster the same as an appraiser?

No. A public adjuster advocates for you during the standard claim process. An appraiser is an independent professional hired specifically to value the loss when a claim enters the formal “Appraisal Clause” dispute resolution process.

🤝 Do public adjusters charge more if the claim goes to appraisal?

They might. If your claim escalates to formal appraisal, your PA may serve as your designated appraiser. Depending on your contract, this might be covered under the original contingency fee, or it might trigger a separate hourly rate for the appraisal work. Check your terms carefully.

💰 Do you have to pay a public adjuster if they get nothing?

No. Under a standard contingency fee agreement, if the adjuster fails to recover any additional funds from your insurance company, you do not owe them a fee for their time or effort.

🏦 Does the fee come out of my pocket or the insurance check?

The fee is almost always deducted directly from the insurance settlement check. The check will typically be issued jointly to you and the adjuster, and the funds are distributed upon endorsement.

📝 Can my mortgage company block the public adjuster from getting paid?

No, but they can slow the process down. If your mortgage company is listed on the settlement check, they must endorse it. They generally will not release the funds until they verify repairs are progressing, which delays everyone’s payout.

⏳ Do I owe a fee if I fire my adjuster before the claim settles?

This depends entirely on your contract’s termination clause. Many contracts state that if you fire them after they have already submitted an independent scope of work to the carrier, they are still entitled to a percentage of any future settlement or an hourly rate for work performed.

📉 Does the adjuster take a percentage of my deductible?

No. Your deductible is the amount subtracted by the insurance company before they issue a payout. The adjuster’s fee is calculated based only on the actual money paid out by the insurance company.

🛑 What happens if the state fee cap changes during my claim?

The fee cap that applies is generally the one that was legally in effect on the date you signed the representation contract. Future changes to state statutes typically do not alter existing, signed agreements.

💸 Does the fee apply to my Additional Living Expenses (hotel bills)?

It can, unless you explicitly negotiate it out of the contract. Many homeowners request that the fee percentage only apply to the dwelling and personal property payouts, exempting their temporary housing reimbursements.

🏘️ How are fees calculated on a total loss where the policy is maxed out?

If your home burned to the ground and the insurance company immediately offered the maximum policy limit without a fight, hiring an adjuster for a percentage of that undisputed limit will only reduce your rebuilding funds needlessly.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.