- Seeing a public adjuster’s name on your insurance check is standard industry practice if you hired one, ensuring their contingency fee is protected.

- Both you and the public adjuster must endorse (sign) the check before it can be deposited or cashed.

- If you have a mortgage, your lender will likely also be on the check, which requires routing the funds through their loss draft department in staggered draws.

- To remove a public adjuster’s name from a check, you typically must resolve any outstanding fee disputes or contract termination requirements first.

The Moment of Confusion: Who Else is on This Check?

I have sat at kitchen tables where homeowners eagerly open their final settlement envelope, expecting to finally pay their contractor and get their house put back together, only to stop and ask: “Who is this other person on the check?” Finding a public adjuster on your insurance check can be confusing, especially if you do not understand why their name was added or, worse, if you do not recognize the name at all.

In my experience reviewing these files, that moment of hesitation is entirely justified. In the claims world, an insurance check that lists multiple parties is known as a joint payee instrument. If you knowingly hired a representative, this is simply the final mechanical step of the claims process. However, if that name is a surprise, it is a massive red flag that requires immediate action before your pen ever touches the paper.

In this guide, I will walk you through exactly what a public adjuster on a check means, the specific steps you must take to endorse and deposit it safely, and what to do if you are stuck in a dispute while the check’s expiration date ticks closer.

Why Does My Insurance Check Say Public Adjuster?

When you hire a professional to represent you during a property claim, they become your authorized representative. As part of that agreement, the insurance company is legally notified of their involvement. Because these professionals work on a contingency model, the insurance company issues the settlement payment jointly. Both your name and the public adjuster’s name will appear on the check, often joined by the word “AND”.

This is not a mistake. It is standard industry practice designed to protect the professional’s contractual right to their fee from the settlement proceeds. Before diving into the check mechanics, if you need a refresher on what a licensed public adjuster’s role entails, understanding their basic function helps clarify why they are tied to your payment.

The insurer does not split the check for you. They send one lump sum, and they leave it to you and your representative to distribute the funds according to your signed agreement. Understanding why their name is there is only the first half of the equation. The second half is knowing exactly how to process that multi-name check without triggering a banking issue.

The Endorsement Process: How to Handle a Joint Check

Because the check is made out to multiple parties, both parties must endorse the back of the check before a bank will accept it. The exact mechanics of how this happens depend heavily on the specific firm you hired and the terms of your contract.

Typically, the process follows one of two paths:

- Path 1: The Meet-up. The adjuster visits you, or you visit their office. You both endorse the check. You then write them a personal check for their fee, and they allow you to deposit the settlement check into your own account.

- Path 2: The Escrow Route. You endorse the check and hand it to the firm. They deposit it into a heavily regulated escrow or trust account, deduct their fee, and issue a new check directly to you for the remainder.

If your claim is taking the escrow route, you need to establish a clear timeline. I always advise homeowners to ask exactly how many business days it will take for the escrow check to clear and for the net payment to be issued. It usually takes 3 to 10 business days for large insurance checks to clear trust accounts. If you are unsure how their contingency fee is calculated, you must review that math before any signatures happen.

Signing the back of the check immediately upon opening the mail, then trying to deposit it into your personal bank account without notifying your representative.

Leaving the check completely unsigned, securing it in a safe place, and immediately emailing your representative to ask for their specific endorsement protocol.

Short field observation from claims experience: I have seen claims stall for an extra month simply because a homeowner tried to use mobile deposit for a joint check without the adjuster’s signature. The bank flagged it for fraud, froze the funds, and required original signature verification from all parties to release the money.

The Modern Alternative: Electronic Payments (ACH)

Increasingly, insurers are offering direct deposit or electronic funds transfer (EFT/ACH) instead of mailing physical checks. If a public adjuster represents you, this changes the mechanics entirely.

In most cases, if there is a signed representation agreement, the insurer will not send the full amount via direct deposit to your personal account, because they cannot physically append the public adjuster’s name to an electronic transfer. Instead, the insurer will either revert to a paper check, or they will deposit the full amount into the public adjuster’s trust account, and the adjuster will then ACH your portion to you.

To avoid delays, email your public adjuster exactly one week before you expect the claim to close and ask for written confirmation of their specific ACH routing protocol.

The Three-Party Check: When Your Mortgage Lender is Included

When the insurer does mail a physical check, the complication can multiply further if you have a mortgage on your home. Your lender has a financial interest in the property, which means the insurer will likely print their name on the settlement check alongside yours and the public adjuster’s.

You cannot simply take a three-party check to your local branch. It must be routed through your mortgage company’s “Loss Draft Department.” This department requires you to endorse the check, have your representative endorse it, and then mail the physical check to them along with a massive packet of contractor estimates, adjuster worksheets, and W-9 forms.

The mortgage company will then deposit the check into their own restricted escrow account. They will not release the full amount to you at once. Instead, they release the funds in smaller increments, known as “draws,” based on the progress of the repairs. Typically, they will release a third of the funds upfront, another third halfway through, and the final amount upon completion. To trigger each draw, the lender will send a third-party inspector to verify the work. This entire process can add weeks to your overall timeline.

💡 Pro Tip: I once worked a file where the homeowner and the PA correctly endorsed a $40,000 check, then mailed it to the mortgage company. The lender rejected it and mailed it back because the PA signed their name slightly outside the designated endorsement box. Always ensure signatures are perfectly placed within the lines on multi-party checks.

What to Do If You Recognize the Public Adjuster

With the lender complication set aside, the more immediate question is whether you actually recognize the name next to yours. If you signed a contract with the firm listed on the check, seeing their name is the expected outcome. Your next step is purely administrative.

Always initiate this coordination in writing. Phone calls are fast, but written records prevent disputes over when the check arrived and how the fee will be handled. Here is a simple template you can use to start the endorsement process safely:

Subject: Settlement Check Received – Claim #[Your Claim Number]

Hello [Adjuster Name],

I am writing to confirm that I received the settlement check from [Insurance Company] today in the amount of [Dollar Amount]. The check is made payable to both of us.

Before we arrange to endorse it, please send me a written breakdown of your calculated fee based on our contract. Once I review the breakdown, we can coordinate the signatures.

Thank you,

[Your Name]

What if they do not reply? If you send this email and the firm ghosts you for more than 3 to 5 business days, you need to escalate. First, call the insurance company’s desk adjuster to verify the firm’s current contact information. If the firm remains unresponsive, send a certified letter requesting instructions. Do not let the check sit indefinitely while you wait for a call back.

The Red Flag: What If the Name is Unfamiliar?

If you open a settlement check and see a name that you do not recognize, the process halts immediately. An unfamiliar name usually indicates one of three scenarios:

Scenario A: Third-Party Filing. A contractor or a restoration company you hired may have filed the claim on your behalf using an affiliated adjuster. Often, this happens in the chaotic days following a storm. You may have signed a stack of digital documents on a tablet, inadvertently signing a representation agreement without realizing it.

Scenario B: Assignment of Benefits (AOB). This is an arrangement where someone was assigned your insurance claim rights. A third party gains the legal right to negotiate and collect insurance money on your behalf. In most states, this practice is heavily restricted or entirely prohibited because of its potential for abuse.

Scenario C: Legally Added Contractors. Sometimes the unfamiliar name is actually your mitigation contractor or roofer. If you signed a “Direction to Pay” document, the insurer is legally obligated to add the contractor’s name to the check. This is different from a public adjuster, but it still requires joint endorsement.

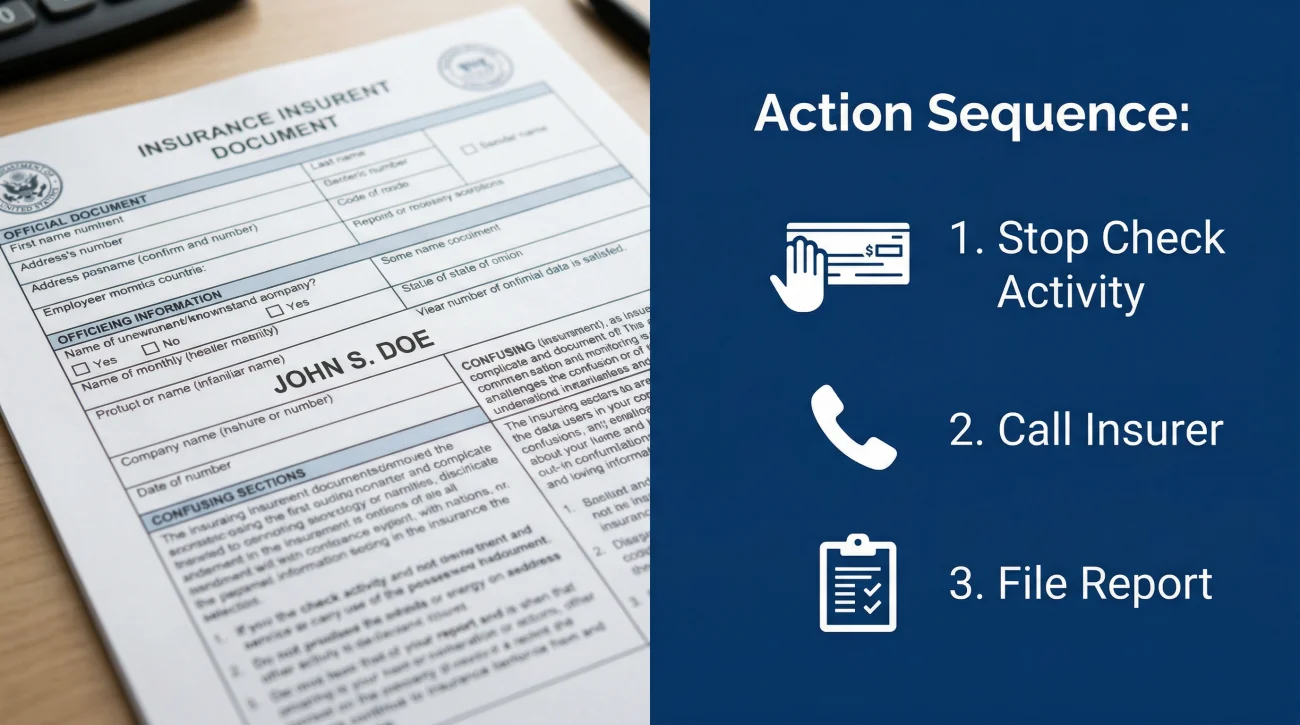

If you find yourself facing an unexpected name, follow this action sequence:

Stop all check activity ➔ Call your insurer for the representation document ➔ File a report with your state Department of Insurance if the representation was unauthorized

You have the right to demand a copy of the exact document the insurance company has on file that authorized them to put that specific name on your settlement check.

Can You Remove a Public Adjuster from an Insurance Check?

Many homeowners ask if they can simply call their insurance desk adjuster and request a new check with only their name on it. The short answer is usually no. The insurance company cannot remove the name just because you ask them to.

The insurer placed that name on the check to protect themselves from liability. If they remove the name and the professional later sues for their unpaid fee, the insurance company could be held responsible for bypassing the contract.

To get a name removed, you typically must resolve the underlying contract. If you fired the firm, or if the engagement was terminated early, you need to review your representation agreement’s termination clause. The clause will dictate what fee, if any, is owed for the work completed prior to termination.

Once you and the firm agree that no further fee is owed, the firm must send a formal “Release of Lien” or a “Letter of Representation Withdrawal” to the insurance company. Only after the insurer receives this official written release will they void the original joint check and reissue a new one solely in your name.

This removal process is where expiration dates become dangerous. Most insurance checks are only valid for 90 to 180 days. If you are locked in a fee dispute and the check expires, you must ask the insurer to reissue it. The insurer will reissue the funds, but they will still print the public adjuster’s name on the new check until that formal lien release is submitted.

Why is the Public Adjuster on My Supplemental Check?

Homeowners are often surprised when they receive a supplemental payment – perhaps for hidden damage discovered during repairs, or a recovered depreciation check – and find the public adjuster’s name on it, even though the main claim was settled months ago.

Unless you formally terminated their representation and submitted a lien release, the public adjuster remains your authorized representative on that specific loss event. Their contract typically entitles them to a percentage of the total recovery for that claim, including all subsequent supplements.

However, if you correctly terminated the contract, paid the cancellation fee, and submitted a formal lien release, their name should not be there. If this happens, you must immediately contact your insurance desk adjuster and provide the dated lien release document to have the check reissued.

⚠️ Signs Your Check Situation is Escalating

Check endorsements should be simple administrative tasks. When they become complicated, it usually means the claim process has derailed. The frustration of holding a large check that you cannot legally use to fix your home is massive. You need to assess if your situation matches any of these high-risk patterns that require immediate escalation.

Your check situation requires intervention if:

- The check is approaching its 90-day expiration date and the firm is refusing to sign until you agree to an unexpected fee increase.

- The firm deposited the check into their escrow account but has missed their own written deadline to issue your net payment.

- Your mortgage lender’s loss draft department rejected the endorsement because the representative altered the check or signed in the wrong designated area.

- You terminated the representation agreement correctly and paid the cancellation fee, but their name is still appearing on newly issued supplemental checks.

If you are stuck holding a check you cannot deposit, or if you are dealing with an escrow dispute that is stalling your recovery, you need an independent set of eyes on the situation. Do not let funds sit indefinitely while your home remains damaged. You can request a free professional claim review to understand your options for untangling the endorsement process.

Final Action Steps Before Proceeding

Handling a joint payee check requires a strict adherence to paper trails. Never hand over an endorsed check to the firm or mail it to your mortgage company without completing these final actions:

- Document the check: Take clear, well-lit photographs of both the front and back of the fully endorsed document.

- Demand a receipt: Require a written acknowledgement from the firm confirming they have taken possession of the check.

- Lock in the timeline: Get written confirmation of the exact date you can expect your net payment to be issued or the exact date the check was mailed to the loss draft department.

If a check is lost in the mail, or if an escrow transfer stretches from days into weeks, those photographs and emails are your only proof that you fulfilled your end of the process.

❓ FAQ

🛑 What does public adjuster on check mean?

It means the insurance company has issued the settlement payment jointly to you and your authorized representative. It is a standard method to ensure the representative’s contingency fee is protected during the payout phase.

✍️ Do both of us have to sign the check?

Yes. When a check is made payable to multiple parties, banking regulations require all listed parties to endorse the back of the check before it can be deposited or cashed.

🏦 Can I just deposit it into my personal bank account?

No, not without the other party’s signature. If you attempt a mobile deposit or ATM deposit without all required endorsements, the bank will likely reject the check or freeze your account for suspected fraud.

📬 My mortgage lender mailed the check back rejected. What do I do?

This usually happens if an endorsement signature is outside the designated box, illegible, or missing paperwork. Contact the loss draft department to identify the exact error, correct the endorsement, and resubmit the packet.

❌ What happens if I cash it without the public adjuster?

Forging a signature or altering the check to bypass a joint payee is bank fraud. Even if a teller accidentally accepts an unsigned joint check, the transaction can be reversed weeks later, causing severe financial and legal problems.

📄 Is there a public adjuster on this check if I didn’t hire one?

If you see an unfamiliar name, you may have unknowingly signed an Assignment of Benefits (AOB) form provided by a contractor. You must contact your insurance company immediately to request the authorization document they have on file.

🚫 How do I get a public adjuster off my settlement check?

You cannot simply ask the insurer to remove the name. The firm must send a formal written release or withdrawal of representation to the insurance company. Once received, the insurer can void the old check and reissue a new one.

💸 Does the public adjuster keep the whole check?

No. They are only entitled to the specific fee percentage outlined in your signed contract. The funds are typically deposited into an escrow account, their fee is deducted, and the remaining balance is paid directly to you.

🤝 Can my contractor cash the check if the PA signed it?

No. The check must be deposited into an account controlled by one of the named payees. Your contractor cannot cash a check made out to you and a public adjuster unless the contractor’s name is legally added to the document via a Direction to Pay form.

⏳ How long does it take for a jointly endorsed check to clear?

Insurance settlement checks are typically large amounts and often subject to bank hold policies. Even with all correct signatures, expect a hold of 3 to 10 business days before the funds are fully available in your account.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.