- Not everyone claiming to handle insurance claims is a licensed public adjuster; verifying their state license is the single most important step before hiring.

- Always check their license through your state Department of Insurance (DOI) portal to confirm their active status and check for any disciplinary history.

- Be highly skeptical of “storm chasers” (individuals who show up uninvited immediately after a disaster and use high-pressure tactics).

- A legitimate public adjuster will gladly provide references, explain their fee structure clearly, and respect your right to review the contract without pressure.

The Reality of Finding a Public Adjuster

If you have recently suffered a major property loss, your mind is probably spinning. You know you need help navigating the insurance claim, and you have heard that a public adjuster can level the playing field. But here is the hard truth I have seen play out too many times: not everyone who knocks on your door or claims to “handle insurance claims” is actually a licensed, ethical professional.

Finding a public adjuster is easy. Finding a legitimate, experienced one requires active vetting. The person who shows up uninvited the day after a storm might be a godsend, or they might be an unlicensed operator looking to lock up your claim before you understand your rights.

This guide is not a directory. Instead, it is the exact process I recommend homeowners use to verify that the person they are considering handing their claim over to is legitimate, licensed, and operating ethically.

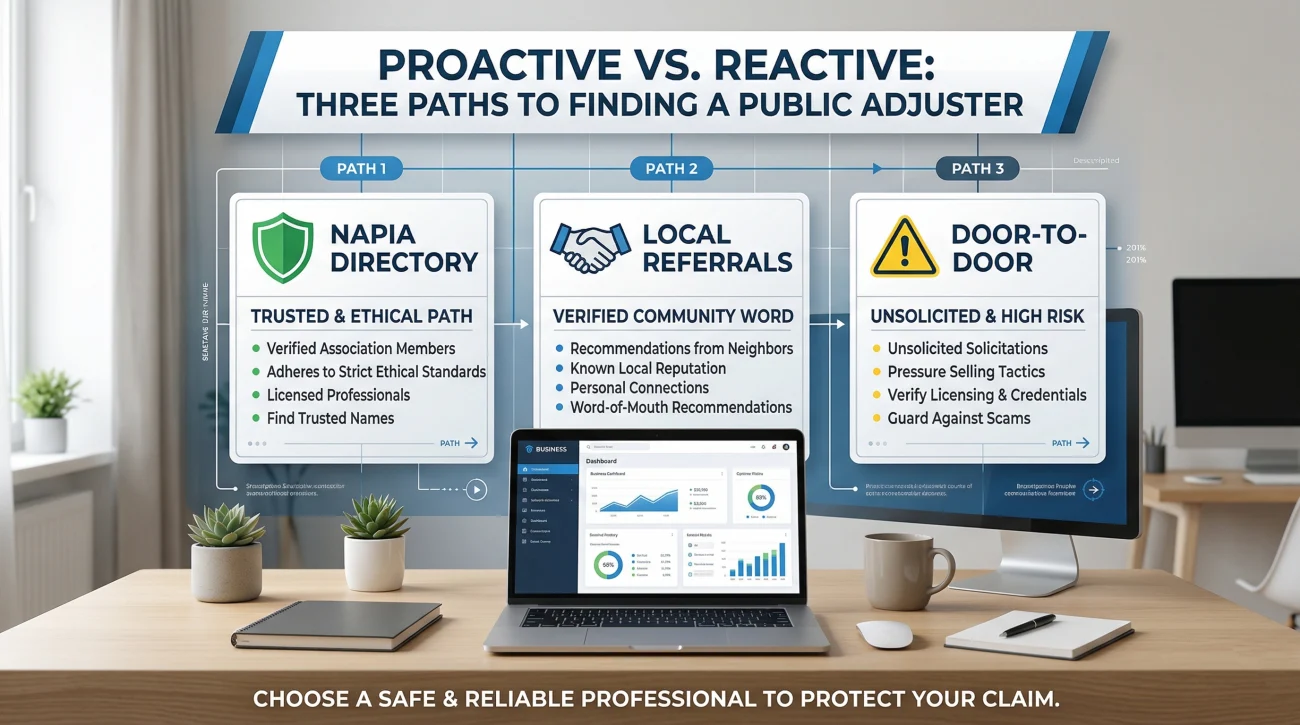

How to Find a PA: Three Paths Compared

Most homeowners encounter a public adjuster through one of three paths. Understanding the difference between proactive and reactive searches is your first line of defense.

- The NAPIA Directory (Proactive): The National Association of Public Insurance Adjusters (NAPIA) maintains a directory of members. Searching here ensures you are starting with professionals who have committed to an industry code of ethics. This is the safest starting point.

- Professional Referrals (Proactive): Getting a recommendation from a local real estate attorney or a trusted contractor can be excellent. However, you must still verify their independent state license.

- Door-to-Door Solicitation (Reactive): Being approached immediately following a fire or severe storm is common. While some local firms do canvas neighborhoods, this is also the primary tactic of bad actors. If you take this path, your vetting process must be absolute.

The License Requirement: Accept No Substitutes

Public adjusters are heavily regulated. They are licensed at the state level by the state’s Department of Insurance (DOI). This is a highly specific, professional credential.

A public adjuster license is entirely separate from a contractor’s license or an independent adjuster’s license (an independent adjuster works for the insurance company, not you). If a roofing contractor tells you, “Don’t worry, we’ll handle the insurance claim for you,” you need to stop and ask for their public adjuster license. When a contractor attempts to act as a public adjuster on a claim where they are also doing the repair work, it creates a direct conflict of interest that most state regulators treat as a serious licensing violation.

The Golden Rule: If they are negotiating your settlement with the insurance company on your behalf, they must hold an active public adjuster license in the state where the property is located.

How to Verify the License

Never take a piece of paper or a business card as proof. You must verify the license independently.

- 🔍 Step 1: Ask the individual directly for their Public Adjuster License Number and the specific state they are licensed in.

- 💻 Step 2: Go to your state’s Department of Insurance website and find the “License Lookup” or “Licensee Search” tool.

- 📑 Step 3: Enter the license number or their name. Verify that the license is currently active, that the license type specifically says “Public Adjuster,” and check if there is any history of disciplinary action.

If you cannot find them in the state database, do not sign anything.

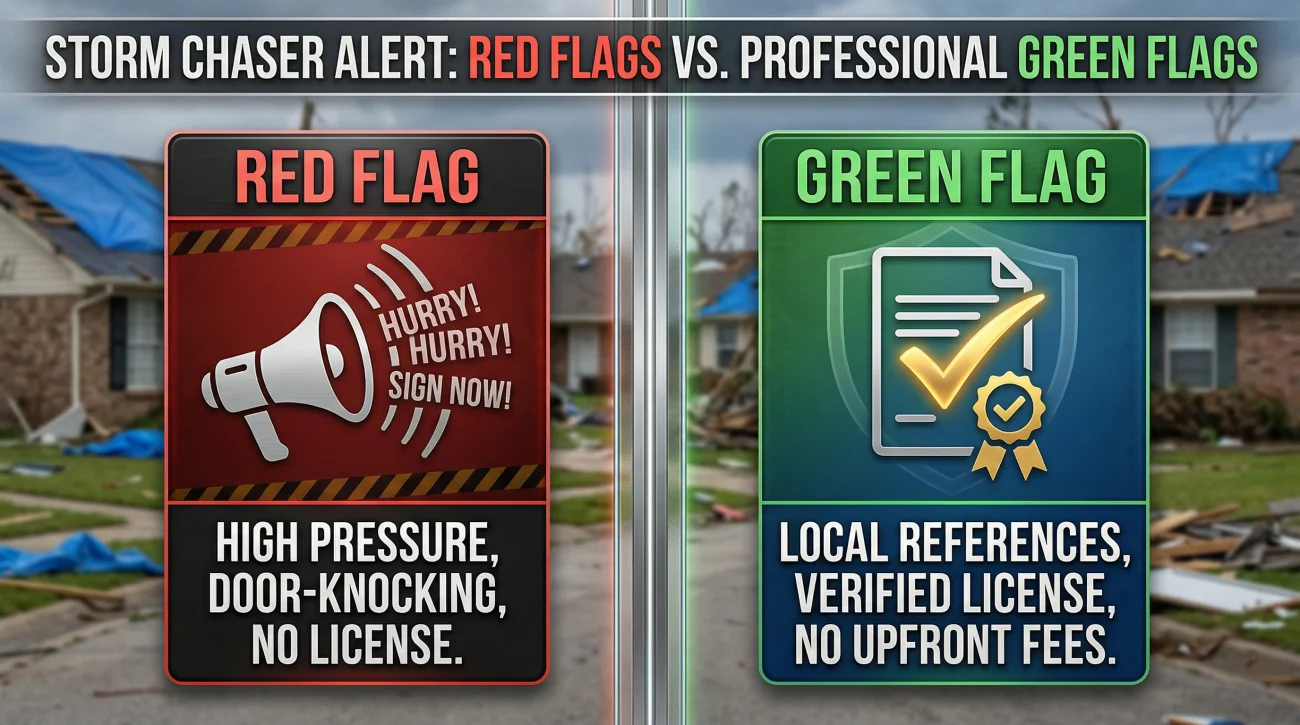

The “Storm Chaser” Problem: Understanding the Context

After a major weather event, such as a hurricane, a massive hail storm, or widespread wildfires, neighborhoods are often flooded with individuals offering to help. Many are “storm chasers”: operators who travel from state to state following disasters, often lacking local licensing and prioritizing claim volume over claim quality.

The difference between a local professional and an unethical chaser usually comes down to behavior and pressure.

Unsolicited door-to-door contact immediately after the disaster coupled with high-pressure tactics demanding you sign a contract “before the insurance company lowballs you.”

Providing a license number immediately upon introduction, leaving a business card, encouraging you to do your own research, and offering local references without hesitation.

If you have been approached by someone and their behavior leans toward pressure rather than professionalism, it is time to ask hard questions to quickly filter out the bad actors.

The 5 Questions You Must Ask Before Hiring

Treat this like a job interview, because that is exactly what it is. Ask these specific questions:

- “What is your public adjuster license number and are you licensed in this specific state?” (This should be answered immediately, no hesitation.)

- “What is your fee structure?” (Specifically ask: Is it a percentage of the total settlement, or a percentage of the new money you recover above what the insurer already offered? For a full breakdown of how legitimate contingency fees work, read our guide on how much a public adjuster costs.)

- “Do you carry Errors and Omissions (E&O) insurance?” (This protects you if the PA makes a professional mistake that harms your claim.)

- “Can you provide three references from local homeowners with claims similar to mine?” (A seasoned PA will have references ready. Call them.)

- “What is your cancellation and rescission policy?” (Most regulated states require a specific rescission window where you can cancel the contract without penalty. They should explain this clearly.)

How to Review the Contract Before Signing

If the adjuster answers your questions well, the next step is reviewing their contract. Never sign on a tablet on your front porch without reading the terms. You need to verify that what they promised verbally is documented in writing.

Look specifically for the fee structure—ensure it clearly states whether the fee is calculated on the total settlement or just the increase. Locate the rescission window (your right to cancel within a set timeframe after signing). If you are unsure what standard terms look like, take the time to review our dedicated guide on understanding the public adjuster contract before you put pen to paper. One clause in particular deserves its own attention before you sign anything.

The Danger of Assignment of Benefits (AOB)

One of the most critical things to look for in any paperwork is “Assignment of Benefits” (AOB) language.

An AOB legally transfers your insurance rights (and the right to receive claim checks directly) to a third party, usually a contractor or a shady claim handler.

If you sign an AOB, you lose control of your claim. The insurance company will only communicate with the assignee, and the settlement checks will go to them, not you. If there is a dispute over the repair work, they can hold your settlement hostage. Because of rampant abuse, many states have moved to limit or severely restrict AOB practices. A legitimate public adjuster will never ask you to sign an Assignment of Benefits form.

Warning Signs You Are Already in Trouble

If you have already engaged with someone and you are starting to feel uneasy, trust your gut. You might be dealing with an unlicensed operator masquerading as a professional.

Here are the definitive signs that the person managing your claim is not operating legitimately:

- Refusal to provide credentials: They dodge the question or claim they “operate under a master license” but cannot provide a state-issued PA license number with their name on it.

- Demanding upfront money: Legitimate public adjusters work strictly on contingency. If they request an upfront “retainer” or inspection fee before any work is done, walk away.

- Guaranteed outcomes: They make absolute guarantees about specific settlement amounts or timelines. No legitimate professional can guarantee what an insurance company will ultimately approve.

- Interfering with your choice of contractor: They insist you must use “their” specific repair crew as a condition of them handling the claim.

If you are experiencing these red flags, you may need a legitimate professional to step in. You can get a free claim review from a vetted, licensed public adjuster here.

What to Do If You Discover Your PA Is Unlicensed Mid-Claim

This is a painful, but unfortunately common, scenario. You signed paperwork days ago, the process feels wrong, and a quick check on the state portal reveals the person handling your claim has no active license.

I have reviewed hundreds of claim files where homeowners unknowingly signed away their rights to aggressive ‘claim handlers’ who were not actually licensed public adjusters. By the time the homeowner realized the mistake, their claim was stalled, and the contractor was holding their settlement hostage.

If you find yourself in this situation, you must act immediately to protect your claim:

- Document everything: Save all texts, emails, and copies of any documents you signed.

- Notify your insurance company: Call your assigned insurance adjuster immediately. State clearly that the individual does not have your authorization to act on your behalf and request that all future communication and payments be directed only to you.

- Contact your State DOI: Report the unlicensed activity to your state’s Department of Insurance. Operating as an unlicensed adjuster is a serious regulatory violation, and the DOI can provide guidance on invalidating the unauthorized contract.

Final Thoughts

Hiring a public adjuster is one of the most important decisions you will make during a property claim. They will take control of negotiations for what might be the largest financial transaction of your life. The ten minutes it takes to ask hard questions, check the state database, and read the contract thoroughly is the best investment you can make. The minor delay caused by proper vetting will save you from months of anxiety and financial exposure.

❓ FAQ

📍 How do I find a reputable public adjuster near me?

Start by checking the NAPIA directory for members in your state, ask for professional local referrals, and always verify their active license through your state’s Department of Insurance website.

🔍 How can I check if a public adjuster is licensed?

Ask for their license number, then go to your state Department of Insurance (DOI) website and use their public license lookup tool to confirm it is active and free of disciplinary actions.

🤔 Are public adjusters actually legitimate?

Yes, licensed public adjusters are highly regulated, legitimate professionals who advocate exclusively for the policyholder. However, unlicensed “storm chasers” are a real problem, which is why vetting is crucial.

🚫 Can a contractor also act as my public adjuster?

In most states, a contractor acting as your public adjuster while also performing the repairs creates a direct conflict of interest that regulators treat as a licensing violation.

🚩 What are the biggest red flags when hiring a PA?

Major red flags include unsolicited door-knocking after storms, demanding upfront fees, guaranteeing specific payouts, and refusing to provide a state license number.

📋 What questions should I ask before hiring one?

Always ask for their license number, a clear explanation of their fee structure, proof of Errors and Omissions (E&O) insurance, local references, and their cancellation policy.

📝 Should I sign an Assignment of Benefits (AOB) form?

No. An AOB transfers your claim rights entirely to a third party. This is a common tactic used by bad actors and many states have moved to severely restrict or limit this practice.

💰 Do I have to pay a public adjuster upfront?

No. Legitimate public adjusters work on a contingency fee basis, meaning they only get paid a percentage after they successfully secure a settlement for you.

🤝 Is a NAPIA membership mandatory?

No, a state license is the only legal requirement. However, NAPIA membership is a strong indicator of professionalism and adherence to an industry code of ethics.

⏳ Can I cancel if I hire the wrong public adjuster?

Most regulated states mandate a specific rescission period that allows you to cancel the contract without penalty shortly after signing. Review the termination clause carefully before signing.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.