- A denied insurance claim is not automatically a dead end for a public adjuster, but their ability to help depends entirely on why the claim was denied.

- Public adjusters are highly effective at overturning “scope or valuation” denials where the insurer mischaracterizes the cause of the damage (e.g., calling storm damage “wear and tear”).

- Public adjusters cannot practice law and cannot overturn “full coverage” denials based on strict policy exclusions. Those situations require an attorney.

- Many denial letters mix these two issues, making a professional review of the actual damage and the letter itself critical before you give up.

The Reality of Denial Letters

Getting a denial letter in the mail is one of the most sinking feelings a homeowner can experience. The language is usually dense, filled with policy citations, and designed to make the decision look final. Your first instinct might be to call a lawyer, or you might wonder if hiring a public adjuster is a better path.

I have sat across from insurance adjusters and reviewed hundreds of denial letters with stressed homeowners. I can tell you that a denied insurance claim is not automatically out of a public adjuster’s reach. However, whether a public adjuster can actually help you depends entirely on the specific reason the insurer gave for saying no.

To understand your options, you have to understand the fundamental role of a public adjuster. A public adjuster works in the space between what you were paid and what the damage actually cost. Their primary leverage is documentation, physical evidence, and scope expertise. Their leverage is not legal authority. This means public adjuster involvement is incredibly effective for certain types of denials and essentially powerless for others.

If you are trying to understand the baseline of what these professionals do, reviewing what a licensed public adjuster actually is will give you the right context. In this guide, we are going to break down exactly which denial letters a public adjuster can fight and which ones require a completely different approach.

Denial Type 1: Scope or Valuation Denials

Imagine your contractor says your kitchen needs $30,000 in repairs after a fire, but your insurance company sends a check for $8,000 and a letter refusing to pay for the rest of the work. This is the territory where a public adjuster thrives. In what the industry calls a scope or valuation denial, the insurance company acknowledges that your policy covers the event, but they aggressively dispute the extent or the cost of the damage.

Many homeowners do not realize that a heavily underpaid claim is actually a form of partial denial. The insurer is effectively denying the remaining scope of work. Because this dispute centers on physical damage and local repair costs, it is the perfect scenario for a public adjuster.

When you hire a public adjuster for a scope denial, they will conduct an independent re-inspection. They will measure the rooms, take their own moisture readings, and build a highly detailed scope of loss using the exact same software the insurance company uses. They use this hard evidence to negotiate the difference. They are not arguing the law; they are arguing the facts of the damage.

Denial Type 2: Full Coverage Denials

A full coverage denial is a completely different hurdle. This happens when the insurance company states that the loss itself is simply not covered under your contract. They might cite a specific policy exclusion, claim your policy lapsed, or state that the peril (like an earth movement or a flood) is strictly forbidden in your paperwork.

A public adjuster cannot change a coverage determination. If your policy explicitly excludes flood damage and a river overflowed into your living room, no amount of careful documentation will force the insurer to pay. More importantly, public adjusters cannot practice law. They cannot provide legal advice or force an insurance company to change its legal interpretation of a policy clause.

If you receive a legitimate full coverage denial, your options typically involve filing a formal internal appeal or hiring an insurance claim attorney. If you are struggling to decipher which kind of letter you received, our guide on identifying a partial home insurance claim denial can help you break down the jargon. But what happens when the line between a physical fact and a policy exclusion gets blurred?

The Grey Area: Misapplied Coverage and Characterization

This is the grey area, and it is where homeowners often throw away thousands of dollars by giving up too early. You will frequently see this in a mixed denial letter, where the insurer pays for some minor items but denies the rest under an exclusion. What looks like a strict legal denial on paper is often based entirely on a flawed physical inspection.

For example, standard policies exclude “gradual” water damage but cover “sudden and accidental” pipe bursts. If a pipe bursts suddenly behind your wall, but the adjuster writes a report claiming the leak has been happening for six months, the insurance company will send you a coverage denial based on the gradual damage exclusion.

This pattern repeats across different types of damage. Consider a severe windstorm that tears shingles off your roof. The adjuster might write a report calling the damage “pre-existing wear and tear”, triggering an age-related exclusion. Similarly, mold resulting from a sudden appliance failure might be denied as “long-term neglect” rather than recognized as the direct result of a covered water event.

“In my field experience, the most common ‘denial’ that a public adjuster successfully overturns is the mischaracterization of damage. When an adjuster calls sudden water damage ‘gradual’ or labels fresh wind damage as ‘pre-existing wear and tear’, they are making a physical characterization, not a legal ruling. A rigorous independent inspection can produce the counter-documentation needed to challenge that label.”

In these grey areas, a public adjuster’s re-inspection is invaluable. They can document the clean edges of a broken pipe, the uplift patterns on a roof, or the distinct lack of long-term rot, proving the event was sudden. By challenging the physical facts, they effectively dismantle the insurer’s reason for applying the exclusion.

What to Do in the First 48 Hours After a Denial

Before you decide between a public adjuster and an attorney, your immediate actions dictate how much leverage you will have later. The very first thing you should do is read the letter carefully to isolate the exact reason given for the rejection. Look for words like “excluded peril” (a coverage issue) versus “pricing guidelines” or “pre-existing condition” (a physical scope issue).

Crucially, do not sign any final release documents or cash checks that have “full and final settlement” printed on them until you have had a professional review your case. Doing so may significantly limit your ability to pursue additional recovery.

If you are unsure why your claim was denied, you should always ask the insurance company to point to the exact contract language and the physical evidence they used. Here is a simple, professional way to request that clarity:

Subject: Request for Specific Policy Language Regarding Claim #[Your Claim Number]

Hello [Adjuster Name],

I have received the denial letter for my recent claim. To help me fully understand this decision, please provide a written explanation that cites the exact page, section, and specific exclusion language in my policy that you are relying on for this denial.

Additionally, please provide a copy of all inspection reports and photographs used to make this determination.

Thank you,

[Your Name]

Working in Sequence: Using Both Professionals

Homeowners often think they have to choose between a public adjuster and a lawyer and stick with that choice forever. The truth is that these two professionals can operate in series, and they often complement each other.

When should a homeowner actually plan for this two-step approach? You should consider this route if you have suffered a massive loss, like a total home fire, and the insurer denies the entire claim based on a technicality (for example, a disputed vacancy clause). An attorney has the legal teeth to fight that vacancy dispute in court or through formal appeals.

However, once the attorney wins that battle and coverage is restored, they are not going to climb onto your burnt roof to count rafters or price out drywall. That is when bringing in a public adjuster ensures the actual rebuild check covers your real-world costs. In complex cases, one professional forces the door open, and the other ensures you get what you are owed once you walk through it.

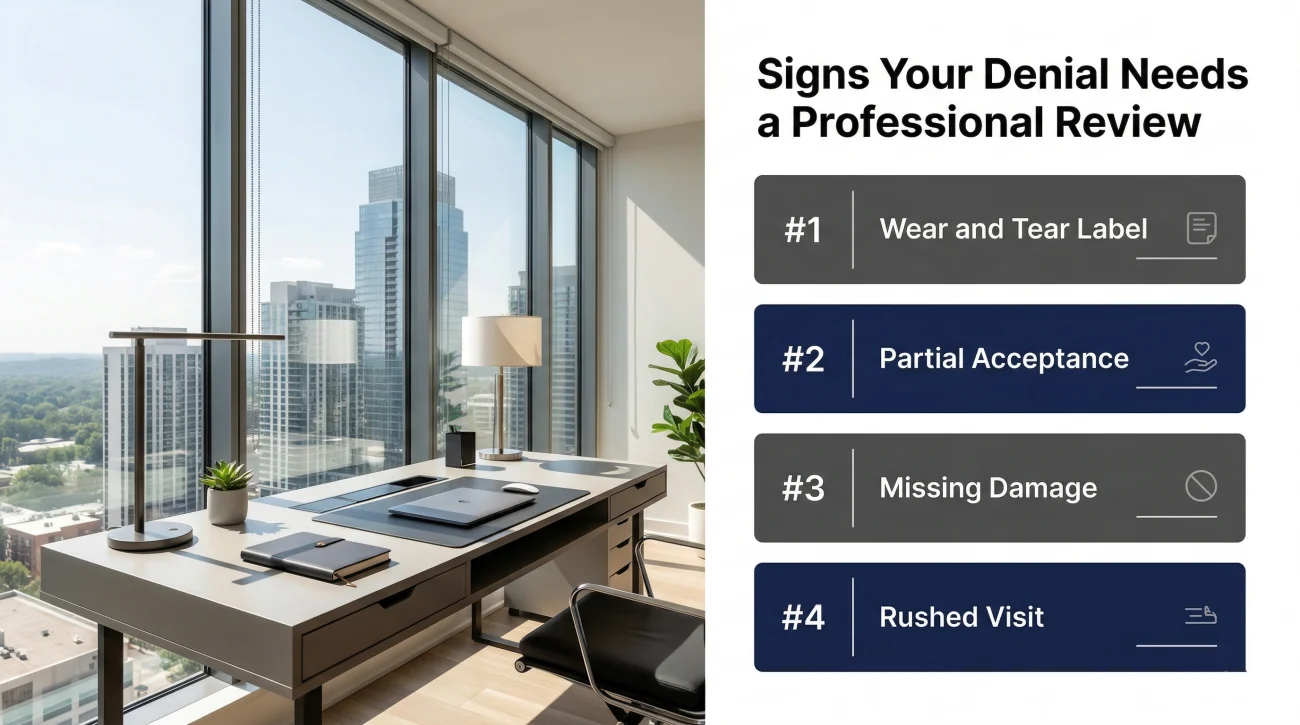

Signs Your Denial Needs a Professional Review

Reading a denial letter is frustrating, especially when the reasons listed do not match the reality of your damaged home. Before you decide to accept the loss, you need to verify if the insurer’s decision is actually airtight.

If you recognize any of the following patterns in your correspondence, the insurer’s decision might be based on a flawed inspection rather than a solid contract exclusion, putting you squarely in public adjuster territory:

- The “wear and tear” label: The denial letter cites pre-existing damage or gradual wear for an event you know for a fact was sudden, like a severe windstorm.

- The partial acceptance: The insurer acknowledged that a covered event happened and paid for minor cleanup, but disputed the full scope of your contractor’s repair estimate.

- Missing damage: Your contractor identified significant structural or secondary damage that is completely missing from the insurance adjuster’s written report and the subsequent denial letter.

- The rushed visit: The denial arrived shortly after an adjuster visit that felt rushed, incomplete, or involved someone who did not even get on your roof or look behind your walls.

When you recognize these patterns, your next step becomes clear. If the dispute centers on the physical reality of your damage – what broke, how it broke, and what it costs to fix – a free review from a licensed public adjuster is the most logical starting point. They can look at the physical evidence and tell you if the adjuster’s documentation was skewed.

However, if the insurer is wielding your contract like a weapon to deny coverage entirely, you need legal leverage. In that scenario, getting a free consultation from an insurance claim attorney is the proper route to pursue. To understand the full landscape of these options, you can also review our comprehensive guide on how to fight a denied home insurance claim.

Final Thoughts on Fighting Back

Do not simply throw your denial letter in a drawer and absorb a massive repair bill. Insurance companies make mistakes, and adjusters are human beings who sometimes rush inspections or mischaracterize complex damage.

A denial letter is a financial defense mechanism, not a final verdict. If you walk away without challenging a flawed physical inspection or a misapplied exclusion, the only party that benefits is the insurer’s bottom line. Get a professional set of eyes on the problem, understand your specific type of denial, and force the insurance company to honor the actual terms of the safety net you have been paying for. If you need a refresher on the basics, reviewing the main reasons why home insurance claims get denied will help you spot the weaknesses in the insurance company’s initial argument.

❓ FAQ

📝 Can a public adjuster reverse a denied claim?

Yes, but typically only if the denial is based on the scope or characterization of the damage. They generally cannot reverse a denial based on a strict legal exclusion in your policy.

💰 Do I have to pay a public adjuster if my claim stays denied?

No. Public adjusters work on a contingency fee basis. If they cannot overturn the denial and recover a settlement for you, they do not get paid.

🏚️ What if my roof claim was denied for wear and tear?

This is a common characterization dispute. A public adjuster can conduct an independent inspection to prove the damage was caused by a sudden storm rather than age.

💧 Can a PA help if my water damage was called gradual?

Yes. If you know the pipe burst suddenly, a public adjuster can gather physical evidence to challenge the insurance company’s claim that the leak was a long-term maintenance issue.

📜 Will a public adjuster read my denial letter for free?

Most reputable public adjusters will offer a free initial consultation to review your denial letter and policy to determine if they can genuinely help your case.

⚖️ Should I hire a lawyer or a public adjuster first?

It depends entirely on the rejection reason. If the dispute is about repair costs or the cause of damage, a public adjuster is usually your best first step. If the insurer completely denies coverage based on contract law, consult an attorney.

⏱️ How long do I have to appeal a denied claim with a PA?

The window varies significantly depending on your policy and your location. Act as quickly as possible rather than assuming you have time.

🛑 Can a PA help if my policy was cancelled?

If your policy was active on the date the damage occurred, you still have rights. However, if the insurer claims the policy was cancelled prior to the event, this is a legal dispute requiring an attorney.

🤝 Do public adjusters and attorneys ever work together?

Yes. In complex denials, an attorney may handle the legal battle to force coverage, while a public adjuster handles the detailed documentation of the repair costs.

📞 Will the insurance company get mad if I hire a PA after a denial?

The claims process is strictly a business transaction. Engaging a licensed professional to represent your financial interests is your right and is a standard part of the industry.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.