- The national average denial rate for property claims has reached 37 percent, meaning the process requires far more rigorous documentation today than it did twenty years ago.

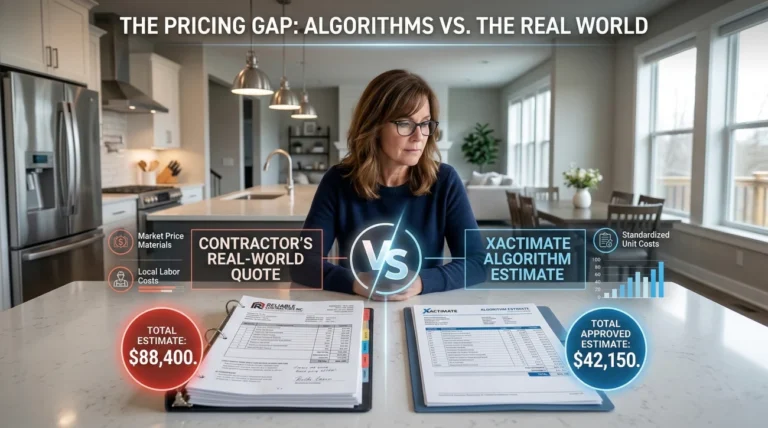

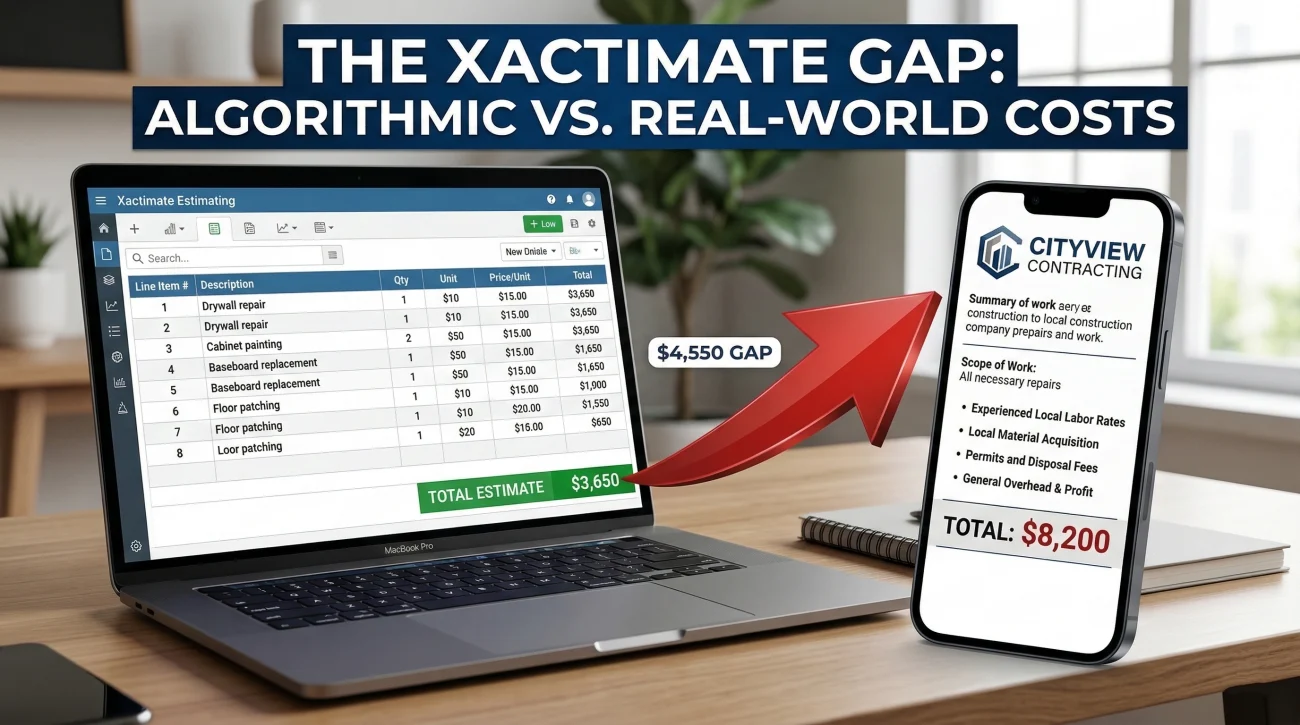

- Algorithmic pricing tools like Xactimate often lag behind actual local contractor rates, frequently resulting in initial settlement offers that fall significantly short of real-world repair costs.

- Relying on outdated expectations of a quick, trust-based payout is a major reason modern claims stall or get denied.

The Shift I See Every Day: Why Old Expectations Fail in a Modern Claim

I started working as a public adjuster in 2019. In those early days, every experienced adjuster I worked with described Hurricane Katrina as the exact moment the property insurance industry fundamentally changed. I did not witness that era firsthand. But when I review a stalled claim file today, I see exactly what that history left behind.

The problem I run into almost daily is a clash of expectations. Most homeowners expect the process to work the way it did in 2004. They believe an adjuster will arrive, inspect the damage, write a fair check, and the repairs will begin smoothly. They approach the situation with the assumption that paying premiums for a decade guarantees a frictionless resolution.

However, the environment they are filing into bears little resemblance to the landscape of two decades ago. The evolution of home insurance claims has transformed a relatively straightforward customer service function into a highly scrutinized, data-driven, and often adversarial documentation process. Understanding how home insurance claims have changed is not just an industry history lesson. It is the absolute prerequisite for getting your home repaired properly today.

The Baseline I Inherited: Before 2005

To understand the current environment, you have to look at the baseline. The history of how insurance claims worked before the mid-2000s is something I inherited from veterans in the field. It was an era characterized by higher trust, shorter settlement timelines, and significantly lower denial rates.

Back then, field adjusters often had the local authority to write checks on the spot for many standard losses. If a kitchen pipe burst, the adjuster evaluated the physical damage, agreed on a reasonable local repair cost, and the claim moved forward. The average homeowner filed a claim maybe once a decade and generally trusted that the outcome would cover their losses.

A senior adjuster I trained under once told me that twenty years ago, his primary job was estimating the repair. Today, he feels the primary job of a carrier adjuster is investigating the policy exclusions first, and estimating the repair second.

This historical context is crucial because it established a culture of trust. A roof claim in 1998 was largely a customer service interaction, and many families still hold onto that generational memory. But applying that 1998 level of casual trust to a modern claim is a nearly guaranteed path to underpayment.

Hurricane Katrina as the Industry Inflection Point

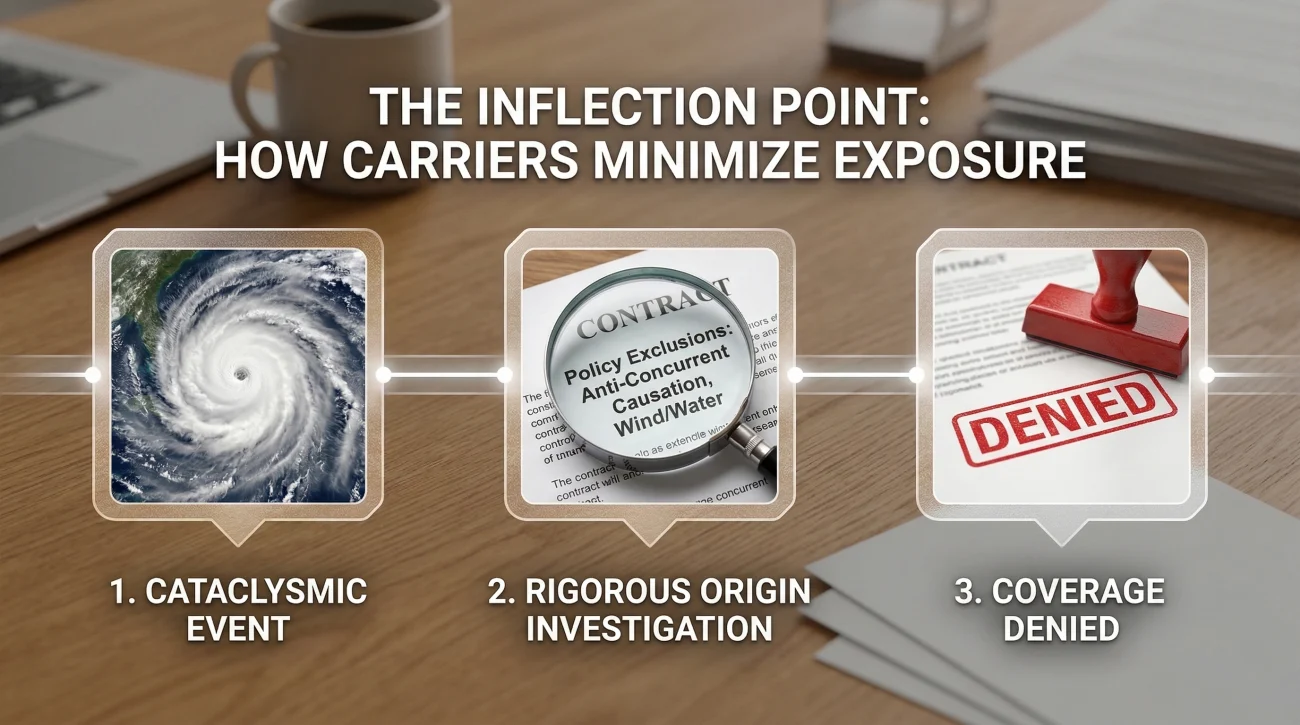

Between 2005 and 2008, the industry experienced a permanent shift. Mass catastrophe claims from hurricane seasons changed carrier behavior on a fundamental level. The sheer volume of losses forced insurance companies to strictly reevaluate their risk exposure and how they managed payouts.

This period marked the first large-scale deployment of aggressive exclusion language. We began to see the widespread enforcement of anti-concurrent causation clauses. These are highly technical policy provisions stating that if damage is caused by two events happening at the same time, and one event is covered (like wind) but the other is excluded (like storm surge flood), the entire claim might be denied. For instance, if hurricane wind tore off your roof and rain subsequently ruined your living room, a carrier might classify the resulting rain intrusion as an excluded flood event and deny the interior damage completely.

Every adjuster who was working the field during that time points to this as the moment the posture shifted. The focus moved heavily toward systematic scope minimization and rigorous origin investigations. Carriers realized that tight policy language could significantly limit their exposure, and that language was written into almost every standard policy renewal from that point forward.

Assuming the adjuster is there solely to calculate how much it will cost to fix your home.

Recognizing the adjuster is there to determine whether the policy language actually requires them to pay for the fix.

The Digital Claims Era: 2010 to 2019

Following the shift in policy language came a massive shift in how repairs were priced. This was the digital claims era, characterized primarily by the introduction and absolute dominance of estimating software, most notably Xactimate. By the time I started in 2019, Xactimate was already the undisputed standard. I had to learn it as the baseline reality, not as a new change.

Xactimate changed the negotiation dynamic entirely. Instead of an adjuster and a local contractor looking at a bathroom and agreeing that a repair would cost a certain amount based on local market rates, the process became algorithmic. The software utilizes a database of labor and material unit costs updated by region.

The core issue is that database pricing frequently lags behind actual local contractor quotes. If the software says drywall installation in your zip code costs a specific amount per square foot, but every reputable contractor in your town charges 20 percent more, you are left with a gap. This algorithmic approach also gave carriers a tool to systematically omit necessary structural costs, like general contractor Overhead and Profit, standardizing underpayment across the board. It removed much of the human discretion from the settlement process.

What I Have Watched Accelerate Since 2019

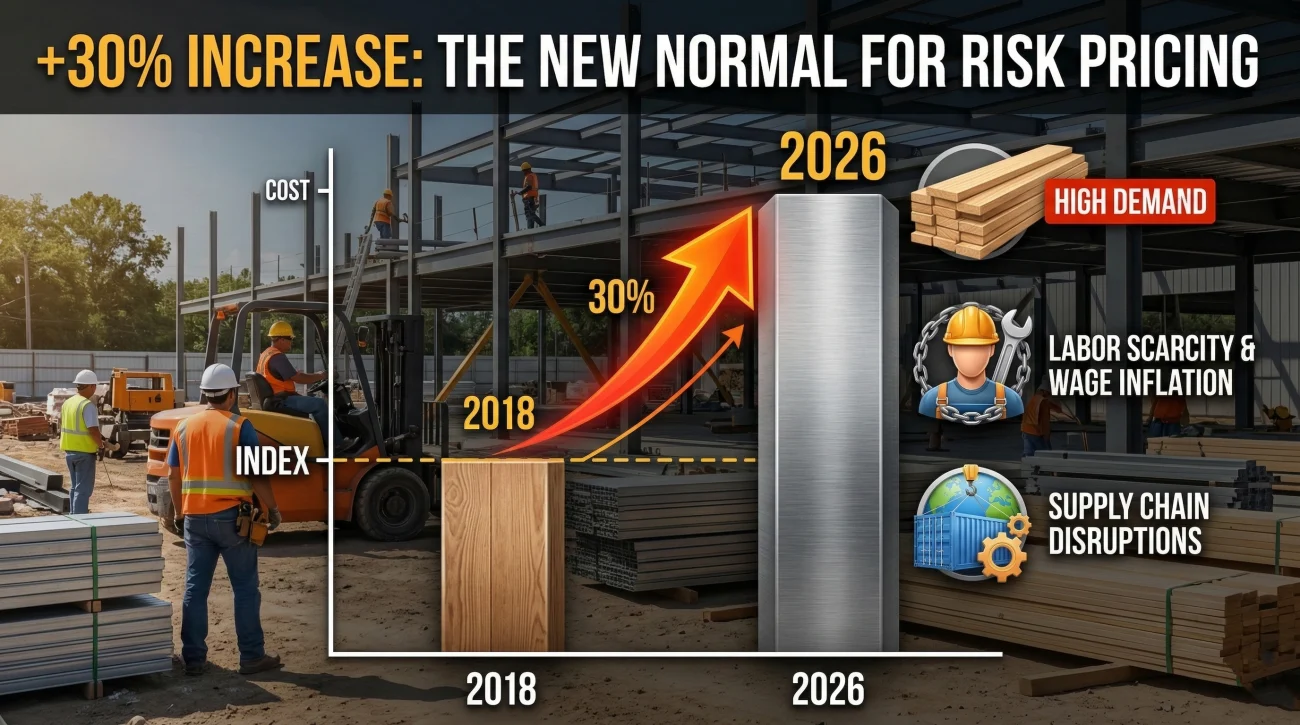

This is where industry history ends and my direct, daily observation begins. What I did not expect when entering this field was how rapidly the environment would accelerate in just a few years. The post-pandemic era introduced an unprecedented level of construction inflation that stressed the entire claims ecosystem.

According to research published by the Insurance Information Institute and Verisk, structural replacement costs rose nearly 30 percent over a five-year period. Material costs skyrocketed, labor became scarce, and supply chain disruptions delayed everything.

I watched this reality hit homeowners hard. Families with Replacement Cost Value policies suddenly found that their coverage limits, which seemed perfectly adequate in 2018, fell completely short of actual rebuild costs in 2022. The claim environment accelerated in ways that even veterans in the field did not fully anticipate, leading to protracted, line-by-line disputes. I see the consequences of this most acutely in complex water damage claims requiring multi-trade scopes. When material prices jump and labor is scarce, an algorithmic estimate that might have been marginally acceptable in 2018 becomes a financial disaster in 2023.

The Pain Point: The Denial Rate Reality Check

All of these historical changes culminate in the single most frustrating aspect of modern insurance claims. You pay your premiums dutifully for years. You finally experience a legitimate loss, perhaps a burst pipe or severe wind damage. You file your claim expecting relief, only to receive a dense, multi-page letter citing policy provisions you have never heard of, ending with a claim denial.

This is not just anecdotal frustration. The statistics reflect a hardening environment. According to NAIC data analyzed by Weiss Ratings, the national average claim denial rate has risen from approximately 25 percent two decades ago to 37 percent today. Even more striking, among the 13 largest insurers in 2023, that figure reached 47.5 percent of claims closed without payment.

⚠️ Warning: The phrase “closed without payment” includes legitimate scenarios, such as claims where the damage amount is below the homeowner’s deductible, or where a strict exclusion like flood damage applies. However, the drastic upward trend indicates a fundamentally stricter review environment.

Furthermore, the timeline to resolution is stretching. A recent J.D. Power 2024 study found that the average claims cycle extends to 23.9 days, with customer satisfaction plummeting to its lowest level in seven years when claims drag beyond a month. It exhausts families, often pushing them to accept inadequate settlements simply to end the ordeal. And what makes navigating this environment so difficult is the one dynamic that has not changed at all.

What Has Not Changed: The Information Asymmetry

While the internal mechanisms of how insurers have changed claims handling are vastly different, some things remain exactly the same. The primary constant is the massive asymmetry of information between the insurance carrier and the homeowner.

When I step in to review a stalled claim today, I almost always trace the problem back to this imbalance. The policy language remains dense, highly technical, and difficult for a layperson to interpret. A homeowner might look at a collapsed ceiling and simply see a leak. The carrier’s team of adjusters, engineers, and legal experts, however, sees a complex matrix of source, duration, and resulting damage.

The most common mistake I witness is a homeowner casually chatting with a desk adjuster over the phone, unaware that every word regarding how and when the damage occurred is being recorded and compared against those exact policy exclusions. Homeowners are still approaching claims with casual conversation, failing to recognize that the modern process is essentially a contract negotiation.

What This Means for Today’s Homeowner

The claim process that exists today requires an entirely different strategy than it did fifteen years ago. You can no longer rely on a handshake and goodwill. You must rely on meticulous, proactive documentation.

If you are stepping into a claim today, you need to adopt a strict documentation discipline. Every phone call must be followed by an email summary. Every piece of damaged property must be photographed before it is moved or mitigated. You have to build a file that proves your loss independently of the carrier’s inspection. Understanding the standard claim process steps from day one is the only way to stay ahead of the adjuster.

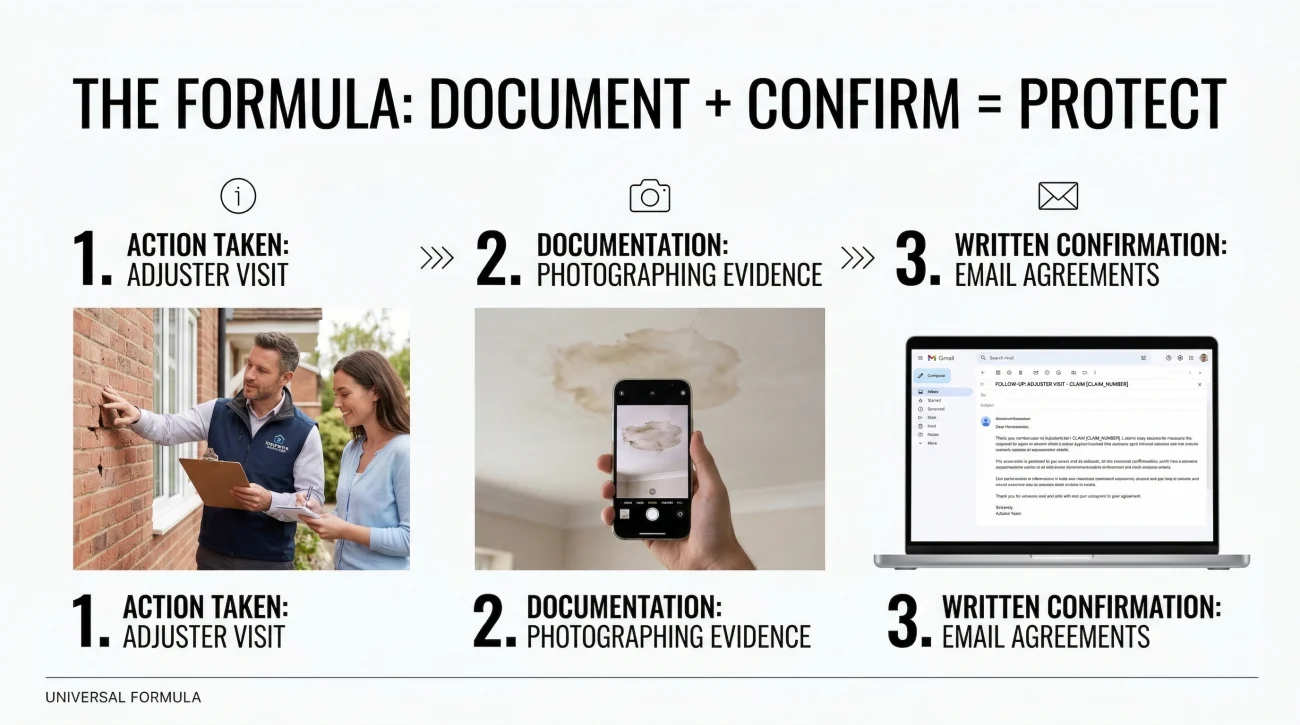

Here is the universal formula I recommend to every homeowner navigating this process:

[Action Taken] + [What was Documented/Discussed] + [Written Confirmation Step]

For example, if the carrier’s adjuster comes to your property, you do not simply wait for their report. You actively shadow them, take your own photos of what they look at, and then send a written confirmation of the visit.

Subject: Confirmation of Adjuster Inspection – Claim #123456

Hello [Adjuster Name],

Thank you for visiting my property today. As discussed during your walkthrough, we reviewed the water damage originating from the upstairs bathroom, which has affected the hallway ceiling, the hardwood floors, and the baseboards.

I am attaching the photos I took alongside you for the claim file. Please let me know when I can expect your preliminary estimate.

Sincerely,

[Your Name]

This simple script establishes a written timeline, confirms the scope of what was viewed, and prevents later disputes about what was actually discussed on site. It sounds formal, but in today’s environment, formality protects your settlement.

Final Thoughts on the Modern Claims Landscape

The reality is that how insurance claims worked before vs now is a study in increased friction. The tools are more advanced, the costs are higher, and the scrutiny is intense. As a homeowner, your best defense is acknowledging this reality early.

Do not let the statistics discourage you, but let them inform your preparation. If you find yourself overwhelmed by the process or facing an estimate that clearly ignores real-world costs, remember that the claims environment has changed significantly; if you have an active claim, a PA who understands the current adjuster environment is worth a free consultation.

📚 Sources and Data Verification

- 🛡️ National Denial Rates: National Association of Insurance Commissioners (NAIC) data, analyzed by Weiss Ratings, showing average denial rates rising to 37%.

- 🏗️ Construction Inflation: Insurance Information Institute (III) and Verisk tracking a near 30% rise in structural replacement costs over five years.

- ⏱️ Claim Timelines: J.D. Power 2024 U.S. Property Claims Satisfaction Study documenting the 23.9-day average cycle and declining satisfaction scores.

❓ FAQ

📈 Has the home insurance claims process changed recently?

Yes, significantly. Over the last two decades, the process has shifted from localized, human-driven estimates to highly centralized, algorithmic pricing models with much stricter investigations into policy exclusions.

💻 What is Xactimate and why does it matter?

Xactimate is the dominant estimating software used by most major property insurers. It uses regional database pricing to calculate repair costs, which frequently lags behind the actual quotes provided by your local contractors.

🏚️ Why are so many property claims being denied now?

Carriers have introduced stricter policy language over the years, enforcing complex exclusions and requiring much higher burdens of proof from the homeowner regarding how and exactly when the damage occurred.

📝 How should I document my damage differently today?

You can no longer rely on the adjuster’s photos. You must take your own comprehensive before-and-after photos, keep a daily log of all communications, and confirm every phone conversation in writing via email.

⏱️ How long does a typical settlement take right now?

While simple claims might resolve quickly, industry data shows the average claims cycle is nearly 24 days. However, complex claims involving disputes over scope or pricing can easily stretch into months.

💰 Why is my payout lower than my contractor’s estimate?

This is often due to the gap between the insurer’s software pricing database and the real-time cost of materials and labor in your specific area, exacerbated by recent construction inflation.

🔍 Do adjusters look at claims more strictly than before?

Yes. Modern field adjusters are heavily trained to look for policy exclusions and pre-existing conditions rather than simply estimating the cost to repair the visible damage.

📄 What should I do if my settlement does not cover replacement costs?

Do not sign a final release. You should immediately ask the adjuster for a line-item breakdown, compare it with your contractor’s bid, and submit a formal supplement request for the missing funds.

🤝 Is it still safe to just trust the insurance company’s initial offer?

In most moderate to large losses, the initial offer is a baseline calculation, not a final verdict. It is standard practice today to review it carefully and negotiate for missed items or inaccurate pricing.

⚖️ At what point should I ask for a second professional opinion?

If you face a complete denial, a massive gap between the payout and your contractor’s quote, or prolonged delays with no clear communication, you should strongly consider consulting a public adjuster.

From filing to final payment: the parts most homeowners do not learn until something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the most common situations where a second opinion changes the result.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.