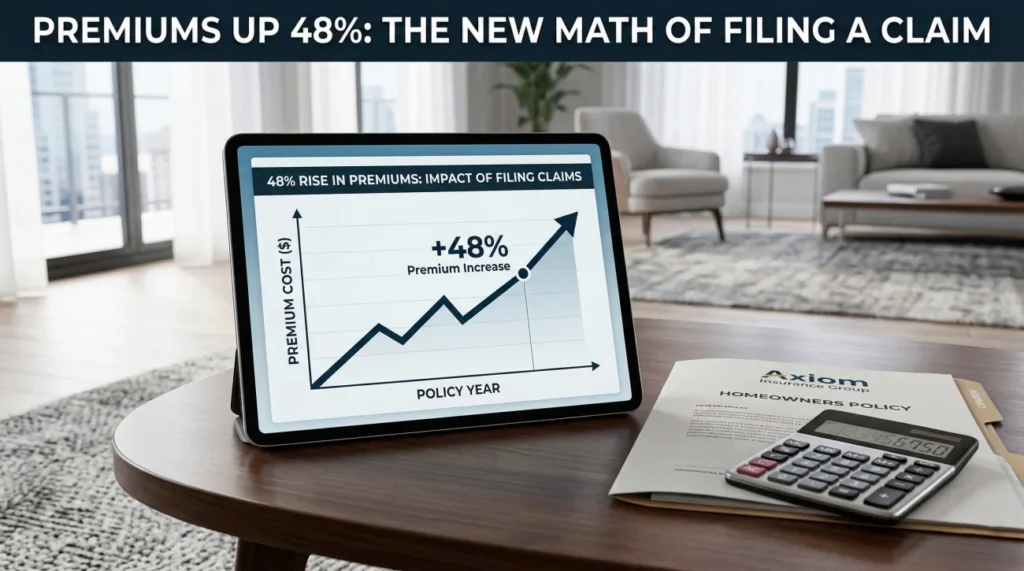

- Home insurance premiums have surged by 48% over the past five years, fundamentally changing how homeowners must approach the claims process.

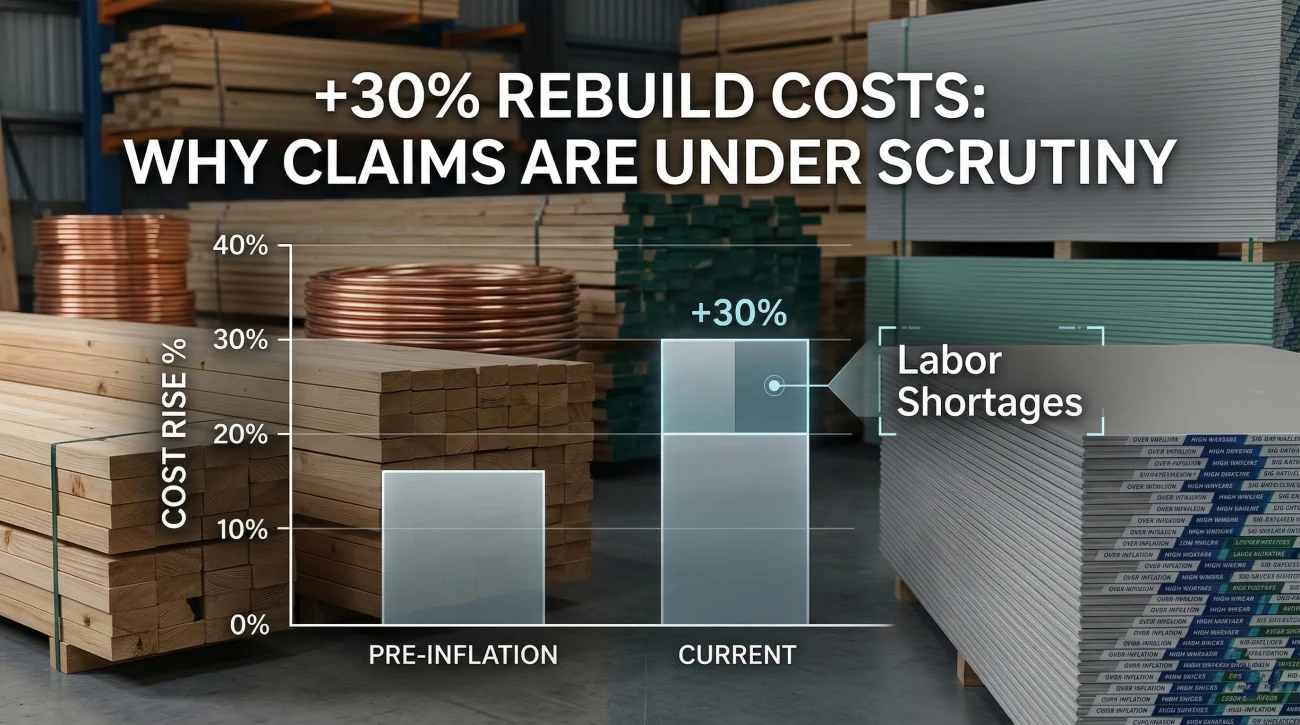

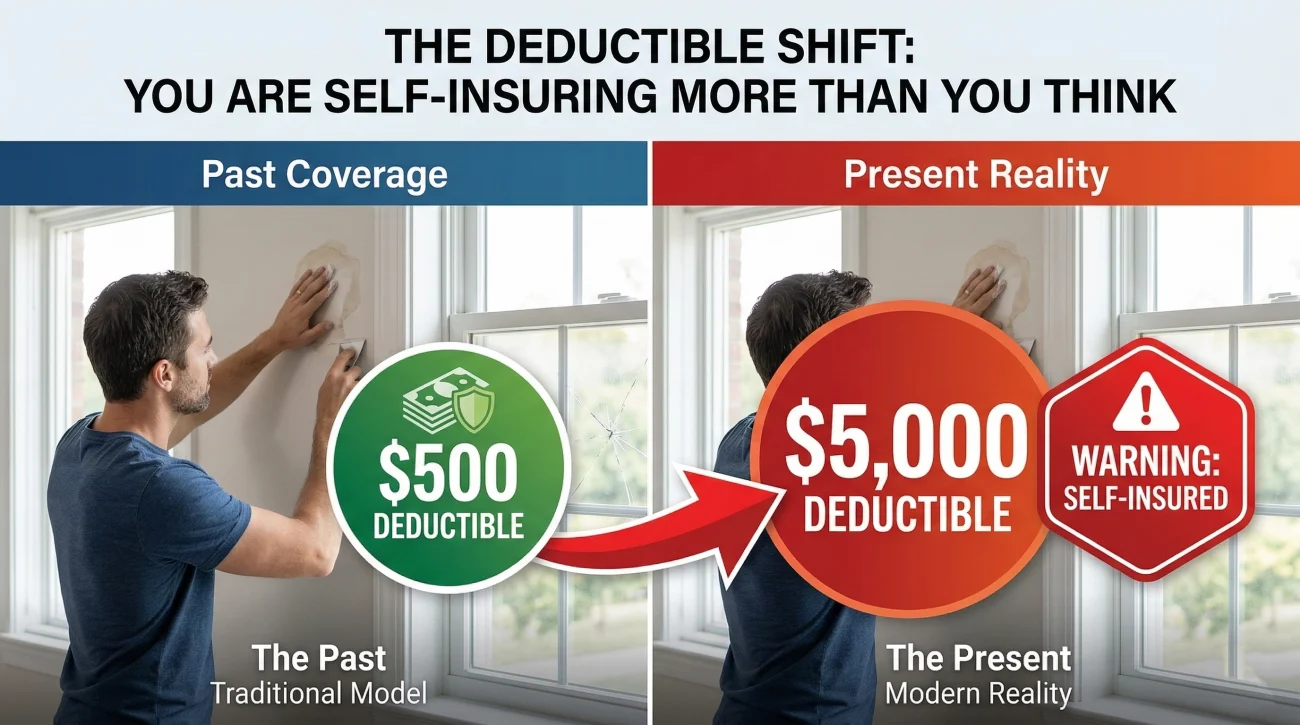

- With structural replacement costs up nearly 30% and deductibles shifting heavily toward the $5,000+ range, you are likely absorbing more upfront risk than you realize.

- Filing a claim today is no longer a default action for moderate damage; it requires calculating your new, higher deductible against a national denial rate averaging 37%.

- Reviewing your current coverage limits is critical. Policies written before 2020 are frequently under-insured for today’s post-inflation rebuild costs.

The New Reality of the Homeowner’s Premium

If you have opened your home insurance renewal notice recently, you already know the numbers have shifted drastically. According to industry data analyzed by ValuePenguin, home insurance premiums have risen 48% over the past five years. Most homeowners I speak with are intensely focused on why their bill is so high, but as a property claims writer, I look at that number differently.

The question most homeowners are not asking is what that 48% increase actually means for the decision to file a claim. Because the reality I see on my desk every day is that the math of filing a property claim has completely changed.

When I review claim files today, I am not looking at the same landscape I saw a decade ago. We are operating in an environment where premiums are higher, deductibles are steeper, and the scrutiny applied to every loss is more intense. If you are still operating under the old rules, assuming you should just call your carrier the moment you see a water stain is no longer safe. You might be setting yourself up for a frustrating financial shock.

“The most expensive mistake a homeowner can make today is treating their hazard policy like a maintenance plan. A claim that pays out $500 today can easily cost you $3,000 in premium hikes over the next three years.”

The Core Cost Drivers Changing the Claims Landscape

To understand why the claims process feels so much more rigid today, you have to understand what the insurance carriers are reacting to. The rising premiums are a symptom of a much larger shift in the cost of physical property recovery.

The primary factor altering how claims are paid is the staggering cost of construction materials and labor. Data released by Triple-I and Verisk indicates that structural replacement costs rose nearly 30% in just a five-year window. This isn’t abstract economic data; this is the price of drywall, 2x4s, copper piping, and the skilled labor required to install them.

When structural costs rise 30%, the insurance company’s exposure rises right alongside it. In response, adjusters are instructed to document everything meticulously, verify the cause of loss rigorously, and ensure that no scope is overpaid. The margin for error has vanished.

Add to this the impact of catastrophic weather events. With 28 separate billion-dollar weather and climate disasters documented in 2023 alone (according to NOAA data cited in recent J.D. Power studies), carriers are managing massive, geographically concentrated losses. This strains both the insurance workforce and the local contractor networks, leading to longer claim lifecycles and stricter adherence to policy exclusions.

The Hidden Shift: Why Your Deductible Matters More Now

This is the pain point I navigate with families almost every week. The frustration rarely starts with the premium increase itself; the true frustration hits when the homeowner suffers a loss, files a claim, and realizes their deductible has quietly shifted.

To offset rising premium costs, many homeowners (and their agents) have raised their deductibles. We are seeing a massive drop in standard $500 or $1,000 deductibles. Today, deductibles in the $2,500, $5,000, or even $10,000 range are becoming the new standard. What this means in practice is that you are unknowingly self-insuring against most common, mid-sized household damage.

You suffered a $3,500 water loss from a burst pipe. With a $500 deductible, the insurance company paid out $3,000. Filing was the obvious choice.

You suffer that same $3,500 water loss today. With a newly adjusted $5,000 deductible, the claim is closed without payment, but the loss is still permanently recorded on your C.L.U.E. report, potentially impacting your future rates.

The shock of discovering that a legitimate, sudden, and accidental water loss will yield zero dollars because it falls below the deductible threshold is devastating. It is a fundamental shift from relying on insurance for recovery to using insurance strictly for catastrophic, home-destroying events.

How the Filing Calculus Has Completely Changed

When you combine higher premiums with higher deductibles, the very act of calling your insurance company becomes a high-stakes decision. You are no longer just asking for repair money; you are triggering an investigation that has a real chance of ending in a denial.

Recent industry data shows that the national average home insurance claim denial rate has reached approximately 37%. When you are deciding whether to file a claim, you must look at the whole board: you have a nearly 4-in-10 chance of being denied, making the decision to involve your carrier riskier than ever. And even if your claim is approved, the final settlement must significantly exceed your high deductible to justify the premium hike that will inevitably follow.

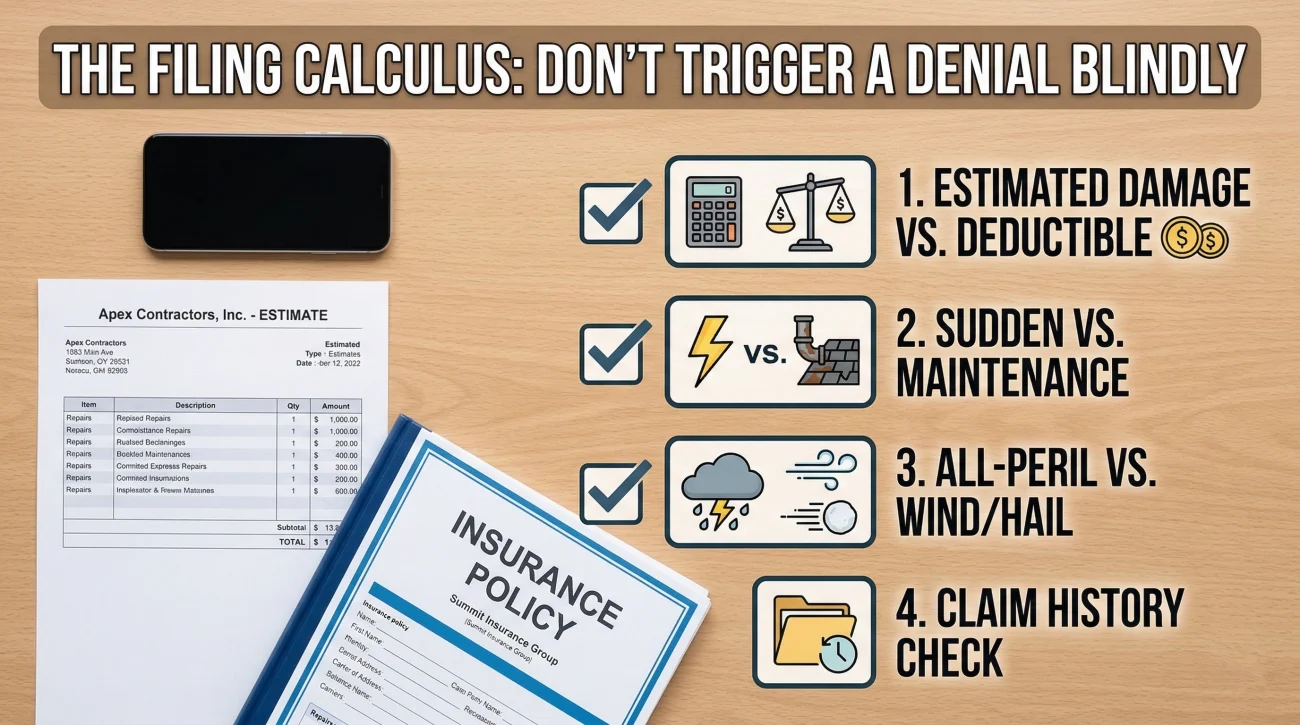

Here is the practical framework I suggest homeowners use before making that initial First Notice of Loss (FNOL) call:

| The Claim Variable | What You Need to Confirm First |

|---|---|

| Estimated Damage | Get an independent contractor out immediately. Does the repair cost exceed your deductible by at least $2,000 to $3,000? |

| Cause of Loss | Is the damage sudden and accidental (like a burst pipe), or is it a long-term maintenance issue (like a slow, hidden rot)? The latter will almost certainly be denied. |

| Policy Deductible | Check your declarations page today. Do you have a standard all-peril deductible, or a separate, much higher percentage-based wind/hail deductible? |

| Claim History | Have you filed another claim in the last 3 to 5 years? Multiple claims can lead to policy non-renewal in today’s hard market. |

The Under-Insurance Problem You Don’t Know You Have

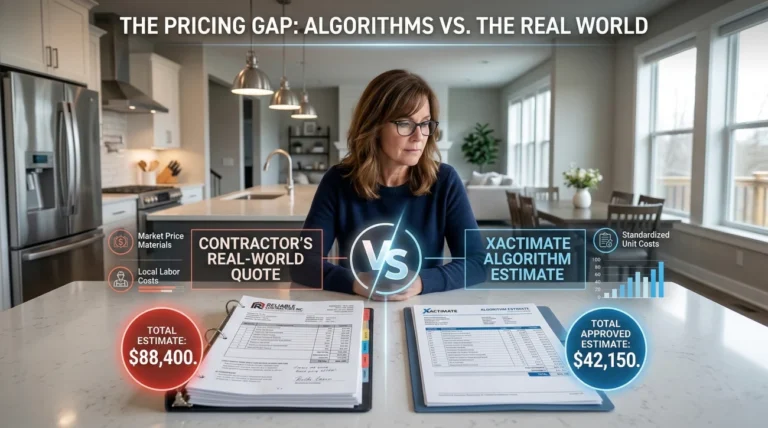

Perhaps the most dangerous byproduct of the rising premium environment is the widening gap in settlement adequacy. Because premiums have spiked, many homeowners have been reluctant to touch their coverage limits, afraid that increasing their limits will cause their bills to skyrocket further.

However, if your Coverage A (Dwelling) limits were set prior to 2020, you are almost certainly under-insured based on today’s construction costs. I frequently review files where a home suffers a total loss from a fire, and the policy limit is capped at $350,000, but the actual cost to rebuild that exact home with 2024 labor and material rates is closer to $480,000.

Warning: An insurance policy will never pay out more than your policy limits, regardless of what inflation has done to the cost of lumber or roofing materials.

It is crucial to understand the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV). You want to ensure your policy guarantees RCV, meaning the carrier pays the cost to buy a new item or rebuild without deducting for depreciation. If you only have ACV coverage on your roof, for instance, a 15-year-old roof destroyed by hail might yield a settlement so deeply depreciated that it barely covers the cost of the dumpster.

If you have suffered a major loss and suspect that the insurance adjuster’s estimate is not aligning with reality due to these inflated costs, getting a professional claim review to compare your current coverage limits against actual rebuild costs can often identify where the structural pricing gap is occurring before you accept a lowball settlement.

Your Strategy Moving Forward: Documentation Before Damage

Because the claim environment has become so strictly regulated and expensive, your best defense is proactive documentation. When an adjuster arrives at your property, their job is to determine the scope of the loss based on verifiable evidence. If you cannot prove the condition of your home before the loss, you are fighting an uphill battle.

- ✅ Take photos of every room annually.

- ✅ Email the photos to yourself with a date stamp.

- ✅ Store your current policy declarations page offline.

If damage does occur, your first 24 hours should focus on mitigating further loss and getting an independent assessment, not immediately dialing your carrier’s 1-800 number. Bring in a trusted local contractor to diagnose the exact cause of loss and estimate the repair cost. Only after you have those hard numbers should you review your declarations page. Look closely at the “Deductibles” section to verify if a separate 2% or 5% wind and hail deductible applies to your specific scenario.

Subject: Clarification on Policy Deductibles and Limits

Hello [Agent Name],

I am reviewing my upcoming renewal. Could you please provide a written breakdown of my current deductibles? Specifically, I need to know if I have a separate percentage deductible for wind and hail, and what that equates to in actual dollar amounts based on my current dwelling coverage.

I also want to verify if any specific items, such as the roof, are currently scheduled for Actual Cash Value (ACV) depreciation upon payout rather than full replacement cost.

Thank you.

Understanding these variables ahead of time removes the panic from the equation. If you are currently looking at a damaged ceiling or a flooded basement and trying to figure out if your specific situation warrants involving your carrier, I strongly recommend evaluating the decision to file so you can weigh the immediate repair costs against the long-term impact on your premiums.

Final Thoughts

Paying significantly more for coverage while watching deductibles climb is a frustrating reality of the current property market. The most critical takeaway is that your approach to using your policy must adapt alongside these costs. Home insurance is no longer a tool for mitigating minor household inconveniences; it is a financial firewall meant exclusively for catastrophic loss.

By understanding how inflation, rising deductibles, and higher denial rates intersect, you take the power back. You can make informed, data-driven decisions about when to absorb a repair out of pocket, and when to engage your carrier. The rules of the game have changed, and protecting your financial future means playing by the new ones. Stop treating your policy like a safety net for every leak, and start treating it like the catastrophic shield it was built to be.

📚 Data & Sources

The statistical data and industry trends cited in this article regarding the current state of home insurance premiums and construction costs are sourced directly from the following industry reports:

- ValuePenguin Home Insurance Statistics: Data confirming the 48% rise in homeowners insurance premiums over the past five years.

- Triple-I (Insurance Information Institute) and Verisk Analytics: Press release data documenting that structural replacement costs have risen by nearly 30% over a five-year period.

❓ FAQ

📈 Why are my home insurance premiums going up with no claims?

Insurance companies base rates on regional risk, not just individual history. If your area has experienced severe weather events, or if the overall cost of construction materials in your state has skyrocketed, your premiums will rise to reflect the carrier’s increased exposure, even if your specific home has never had a loss.

🛑 Will my home insurance drop me if I file a claim?

Filing a single, legitimate catastrophic claim usually will not cause a non-renewal. However, filing multiple claims within a 3 to 5 year period, or filing a claim for issues deemed to be lack of maintenance, significantly increases the risk that your carrier will drop your coverage at renewal time.

💰 How much does home insurance go up after a claim?

While it varies by state and carrier, industry averages suggest a single weather-related claim might raise your premium by 10% to 20%, whereas a liability or non-weather water damage claim can increase your rates by 20% to 30% or more for several years.

🏠 Should I file a claim for roof damage if my deductible is high?

You should only file if the repair estimate from an independent roofer significantly exceeds your deductible. If you have a $5,000 wind/hail deductible and the repair is quoted at $6,000, filing a claim to receive $1,000 is often not worth the subsequent premium increase.

📉 Is it worth filing a claim for $3,000 in water damage?

In most modern policy environments, no. If your deductible is $2,500, the insurance will only pay out $500. You will have a water damage claim on your permanent record, which will likely cost you more in premium hikes over the next three years than the $500 payout you received.

📊 Why did my deductible change without me asking?

Many carriers have automatically shifted policyholders from flat-rate deductibles (e.g., $1,000) to percentage-based deductibles (e.g., 2% of the dwelling coverage) for specific perils like wind and hail upon renewal. You must review your declarations page annually to catch these structural changes.

📝 What happens if my insurance estimate is lower than my repair cost?

This is extremely common. You do not have to accept the initial payout as final. You or your contractor can submit a “supplement,” which is a request for additional funds backed by documentation and line-item estimates proving the carrier’s original scope was insufficient.

🔎 Do insurance companies check past claims when I switch?

Yes. All major insurance carriers use the C.L.U.E. (Comprehensive Loss Underwriting Exchange) database. This report shows your property’s claim history, including claims you filed and claims filed by previous owners, typically looking back five to seven years.

⏱️ How long does a home insurance claim stay on my record?

A home insurance claim typically remains on your C.L.U.E. report for five to seven years. During this time, it can impact your ability to get competitive rates or switch to a new insurance carrier.

⚖️ Can I dispute a premium increase after a claim?

You cannot directly dispute a standard rate hike, as these rates are filed and approved by your state’s Department of Insurance. However, you can combat it by shopping around for new quotes, increasing your deductible to lower the premium, or asking your agent to re-run your profile for new discounts.

From filing to final payment: the parts most homeowners do not learn until something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the most common situations where a second opinion changes the result.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.