- A denial letter is not just a paperwork issue; it creates immediate financial trauma, often forcing families to drain savings or take on high interest debt to repair their homes.

- Industry data shows the average fire claim is over $88,000, and with large insurer denial rates approaching 47%, the number of families facing this crisis is significant.

- The most exhausting part of a denied claim is the cycle of paperwork and delays that often causes homeowners to give up the fight.

- A denial is not always the end of the road. Understanding your options gives you the power to push back without letting the process overwhelm you.

The Reality Behind the Single Page Denial Letter

When an insurance company denies a claim, they send a formal letter. It is usually just one or two pages long, citing specific policy language, exclusions, and legal definitions. But having sat across from hundreds of homeowners in my career, I know that what that piece of paper represents is not captured in the fine print.

For the family receiving it, a denial letter means displacement. It means unexpected debt, arguments at the kitchen table, and sleepless nights worrying about mold spreading or a roof failing. Many homeowners come into the claims process expecting a safety net, only to feel like they have hit a concrete floor. If you are wondering what happens when a home insurance claim is denied, the answer goes far beyond the boundaries of an insurance contract.

In this guide, I want to walk through the actual financial and emotional consequences of a denied claim. We are going to look at the real numbers, the patterns I see families fall into, and why the exhaustion of the process is often the hardest part to overcome.

The Scope of the Problem

Before diving into the individual financial trauma, it is crucial to understand the sheer scale of this environment. If you are dealing with a denied claim, you might feel like you did something wrong or that you are an isolated case. You are not. The population of families facing this exact situation is growing rapidly.

The III reports that in 2023, approximately 5.3 percent of insured homes filed a claim. While that might sound like a small percentage of the population, the response to those claims is changing. Recent analysis by Weiss Ratings, based on National Association of Insurance Commissioners (NAIC) data, revealed that the denial rate among the 13 largest insurers reached 47.5% in 2023.

This data means nearly half of the homeowners who asked their largest carriers for help last year received a closure without payment. Behind every single one of those statistics is a family trying to figure out how to pay a mitigation contractor.

The Financial Reality That Statistics Do Not Convey

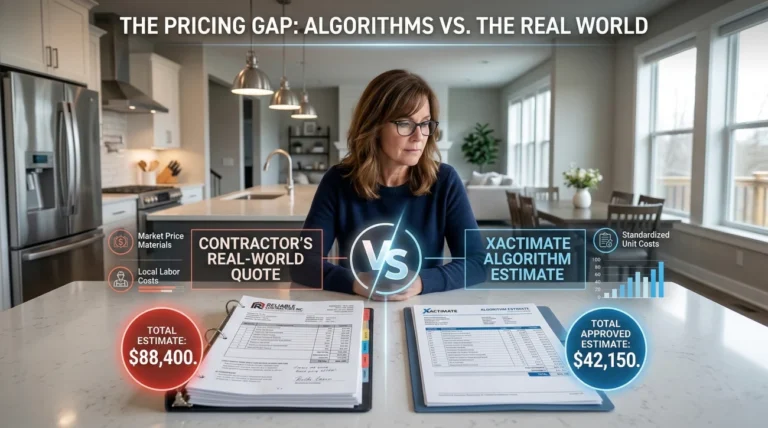

When we talk about insurance claims, it is easy to get lost in abstract numbers. But let us look at what a severe property loss actually costs. According to data from the Insurance Information Institute (III), the average fire and lightning claim between 2019 and 2023 was $88,170.

When a carrier refuses liability for a severe loss, that reconstruction cost does not simply vanish. It becomes an immediate, crushing burden that the family must absorb. I have reviewed countless files where homeowners were forced to make impossible financial choices within days of receiving a denial.

What Denied Families Actually Do

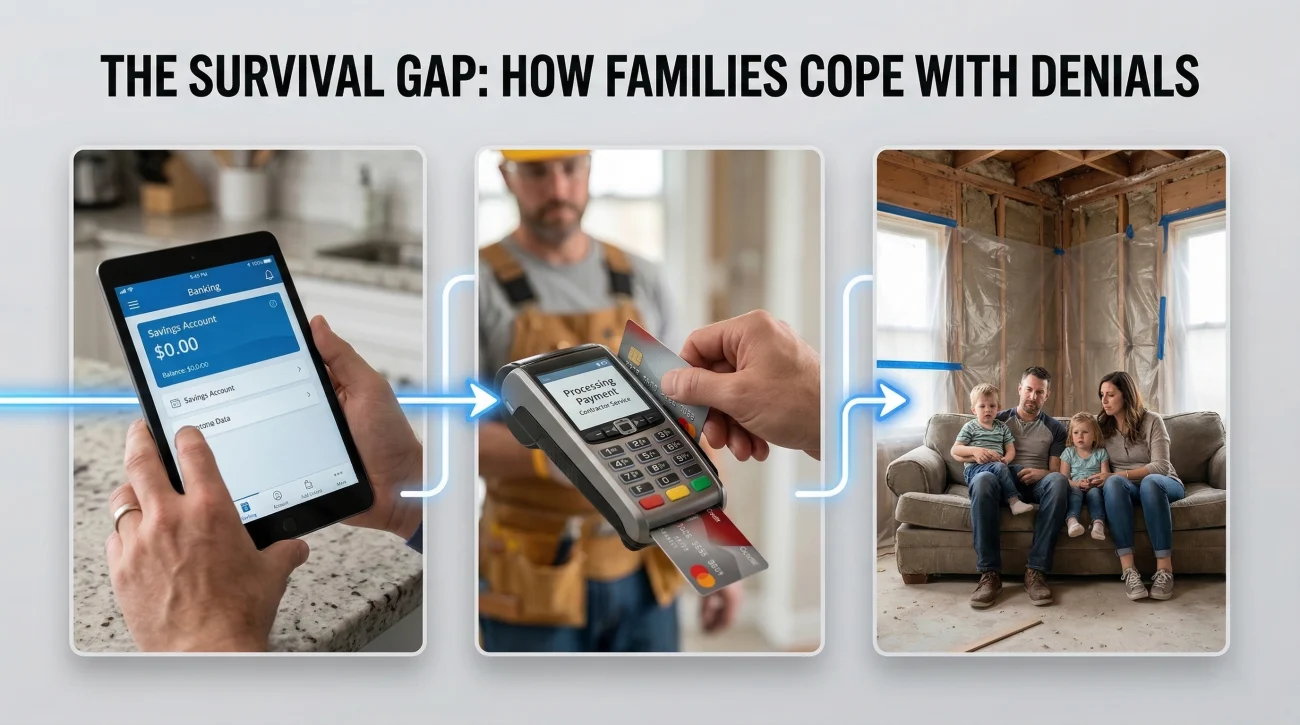

In my experience, when the safety net fails, homeowners generally fall into one of three documented patterns to survive the financial hit:

- Draining emergency savings: Funds meant for retirement, college, or medical emergencies are immediately redirected to basic structural repairs just to make the house livable.

- Taking on high interest debt: Without a lump sum settlement, families turn to credit cards or personal loans to pay mitigation contractors who are threatening to place liens on the property.

- Living in damaged conditions: Perhaps the most difficult scenario I see is when families simply cannot afford the repairs. They live with compromised roofs, torn out drywall, or isolated rooms while trying to figure out how to dispute the carrier’s decision.

The financial trauma often extends far beyond the immediate repair bills. When a homeowner takes on high interest personal loans or maxes out credit cards to fix a roof, their credit utilization spikes. The long term financial impact can last for years, affecting their ability to refinance or secure future loans.

But the cost of physical repairs is only one part of the financial burden. The next immediate challenge is often dealing with the sudden loss of your temporary housing coverage.

The Hidden Crisis of Displacement

One of the most immediate consequences of a denied home insurance claim is the loss of temporary housing support. Most standard policies include Additional Living Expenses (ALE) coverage, which pays for hotel stays or rentals if your home is uninhabitable. However, if the core property damage claim is denied, the ALE coverage is almost always denied right along with it.

I recently spoke with a family who spent two months living in a small hotel room on their own dime after a water loss denial. The financial drain of paying a mortgage on an empty, damaged house while simultaneously paying for temporary lodging is a stress test few budgets can survive.

The timeline makes this even worse. A 2024 J.D. Power study found that overall satisfaction drops significantly when claims stretch beyond 31 days. For a denied claim, the timeline to resolution is rarely measured in days. Disputing a denial can take months or even years, and during that entire period, the family is fully responsible for their own housing costs.

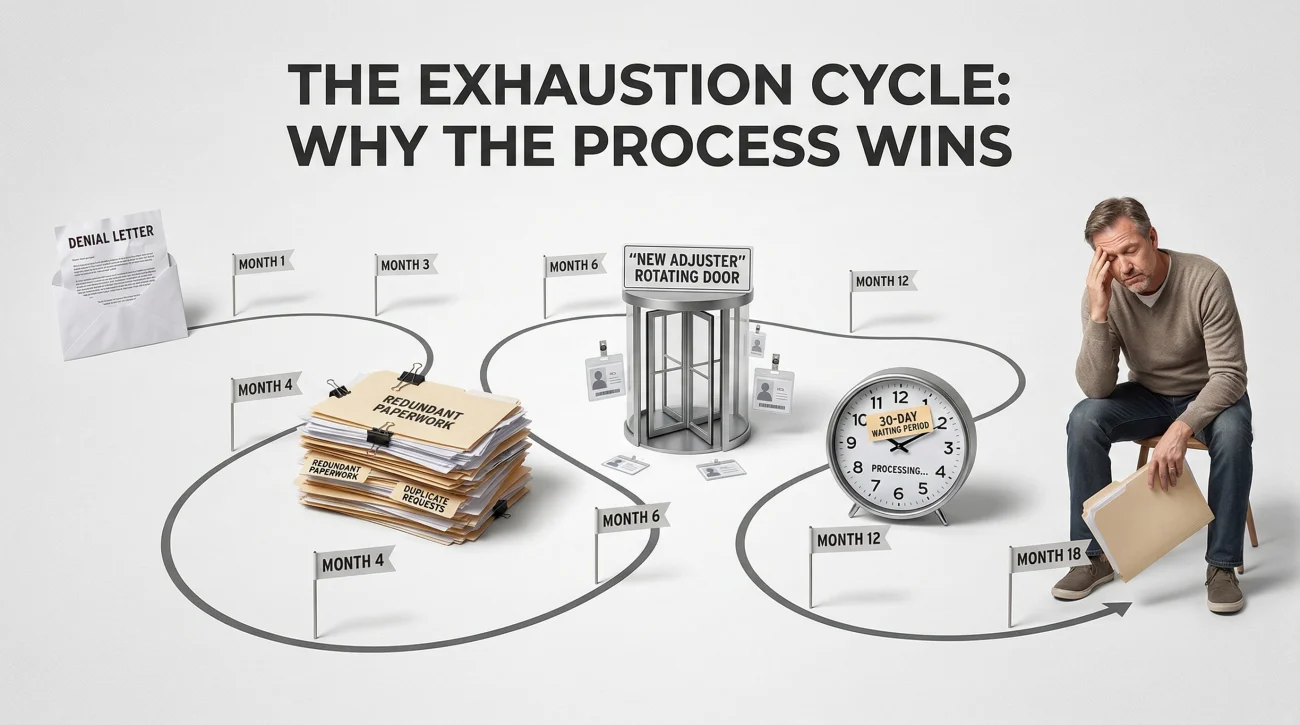

The Exhaustion Cycle: Why Families Stop Fighting

The financial impact of a denied home insurance claim is devastating, but the emotional toll is often what actually breaks a homeowner’s resolve. When I review the history of an abandoned claim, I almost always see a distinct pattern of emotional and bureaucratic exhaustion.

Families describe feeling gaslit by a process that operates like a war of attrition. A denial dispute is rarely a single, definitive conversation. Insurers often use micro tactics that, intentionally or not, wear homeowners down over time. In my experience, these delay tactics are remarkably consistent:

- Rotating adjusters: Homeowners are forced to re-explain their entire claim history to a new desk adjuster every few weeks.

- Redundant paperwork requests: Carriers frequently ask for photos, invoices, or contractor estimates that were already submitted in the first month.

- Asymmetrical deadlines: The homeowner is given 48 hours to reply to a request, but the carrier takes 30 days to review the submission.

The timeline of a denied claim rarely matches the expectations of the policyholder. From the date of the denial letter, a formal dispute, reinspection, and potential appraisal process can easily drag out for six to eighteen months.

Note: The most common reason a family walks away from a legitimate claim dispute is not because they were proven wrong. It is because they simply ran out of time, mental bandwidth, and financial resources to keep fighting the bureaucracy.

The Gap Between the Promise and the Reality

What makes a denied home insurance claim uniquely painful is the fundamental violation of trust. For years, you pay premiums based on a simple promise. The marketing materials sell absolute peace of mind. Commercials promise “comprehensive protection” and assure you that you will be treated like family when disaster strikes.

The reality is that an insurance policy is a highly complex legal contract filled with strict limitations, endorsements, and exclusions. For example, a homeowner might hear “comprehensive water damage coverage” in a commercial and assume their flooded living room is protected. They are shocked to receive a denial letter that legally separates “sudden pipe bursts” from “long term seepage” or “surface water intrusion.”

Broad reassurance built on feelings of safety and community support.

A binding legal contract governed strictly by definitions and exclusion lists.

The gap between the peace of mind you purchased and the strict contract you actually signed is where all the distress lives. When a rejection happens, homeowners are forced to understand their specific denial type and learn how to read policy language at the exact moment they are most vulnerable.

The Escalation Decision: Fighting Alone vs. Hiring Help

Once you decide that a denial is incorrect, you have to choose how to proceed with your dispute. Navigating the exhaustion cycle requires a strategy. Fighting it yourself costs nothing upfront, but it requires massive amounts of time, deep policy knowledge, and the emotional stamina to handle the inevitable delays.

Hiring a professional levels the playing field, but it changes the financial math. Because public adjusters work on a contingency fee basis, it means sharing a percentage of your eventual settlement, though it also means you pay nothing out of pocket if the denial is not overturned. From my experience, understanding this trade off is key to making the right choice for your family.

You take on the full burden of proving the loss, interpreting dense policy language, and managing all exhausting correspondence while trying to maintain your daily life.

A licensed professional takes over the communication, documents the scope with industry standard software, and fights the denial based purely on contract law and claims experience.

Final Thoughts

A denial letter is designed to feel like an absolute final verdict, but in my experience, it is usually just the opening position of a negotiation. The process counts on you walking away out of sheer exhaustion. You do not have to let that happen.

Insurers make mistakes, adjusters misapply policy language, and initial rejections are overturned every day when met with the right documentation. Navigating what comes next is simply a matter of knowing your options and building a strategy to push back.

If you want a professional perspective on whether the carrier’s decision is challengeable, you can schedule a free claim review with a licensed public adjuster. You have already paid years of premiums to protect your family. Taking the next step is about making sure that contract is actually honored.

📚 Data and Sources

- Insurance Information Institute (III): Data regarding the average fire claim cost ($88,170) and the percentage of insured homes filing claims (5.3% in 2023). View Source

- J.D. Power: 2024 U.S. Property Claims Satisfaction Study detailing the timeline of claims and the drop in satisfaction after 31 days. View Source

- NAIC via Weiss Ratings / National Mortgage News: Analysis showing the 47.5% denial rate among the 13 largest homeowners insurers in 2023. View Source

❓ FAQ

🛑 What happens when home insurance claim is denied?

You will receive a formal denial letter explaining the policy reasons for the rejection. At that point, the insurer closes the file, and you become financially responsible for the repairs unless you formally dispute their decision.

💸 Do I have to pay out of pocket if my claim is denied?

Yes. If the insurance company denies liability for the damage, the burden of paying contractors for mitigation and reconstruction falls entirely on you.

🏚️ Can I just live with the damage after a denial?

You can, but it is risky. Unrepaired damage like roof leaks or water intrusion can lead to mold or structural failure, which could cause your insurer to drop your coverage entirely at renewal.

📝 Will a denied claim still make my premium go up?

In many cases, yes. Simply filing the claim puts it on your loss history record. Even if they pay nothing out, the carrier may view you as a higher risk and raise your rates.

🔄 How do I know if my claim denial is final?

A denial is rarely absolute on the first pass. You have the right to request a reinspection, submit new evidence, or hire your own experts to challenge their findings.

⏳ How long do I have to fight a denied property claim?

This depends on your specific policy and state regulations. Most policies have a one to two year window from the date of loss to dispute the claim or file a lawsuit, but you should verify this immediately in your policy documents.

📞 What should I say to my adjuster after a denial?

Keep it strictly professional and in writing. Ask them to provide a detailed explanation of the denial and to point out the exact policy exclusions they are relying on.

⚖️ Is it worth fighting a denied insurance claim?

If the repair costs are significant and you have evidence that the damage should be covered under your specific policy, it is often worth pushing back or getting a professional second opinion.

📉 Does a denial go on my CLUE report?

Yes. Any claim you file, whether it is paid out or denied, is recorded in the Comprehensive Loss Underwriting Exchange (CLUE) database for up to seven years.

🛡️ Who can I call for help with a denied claim?

If you need help disputing a technical denial, you can consult a licensed public adjuster to review your scope, or an insurance claim attorney if the dispute involves bad faith or complex legal interpretation.

From filing to final payment: the parts most homeowners do not learn until something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the most common situations where a second opinion changes the result.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.