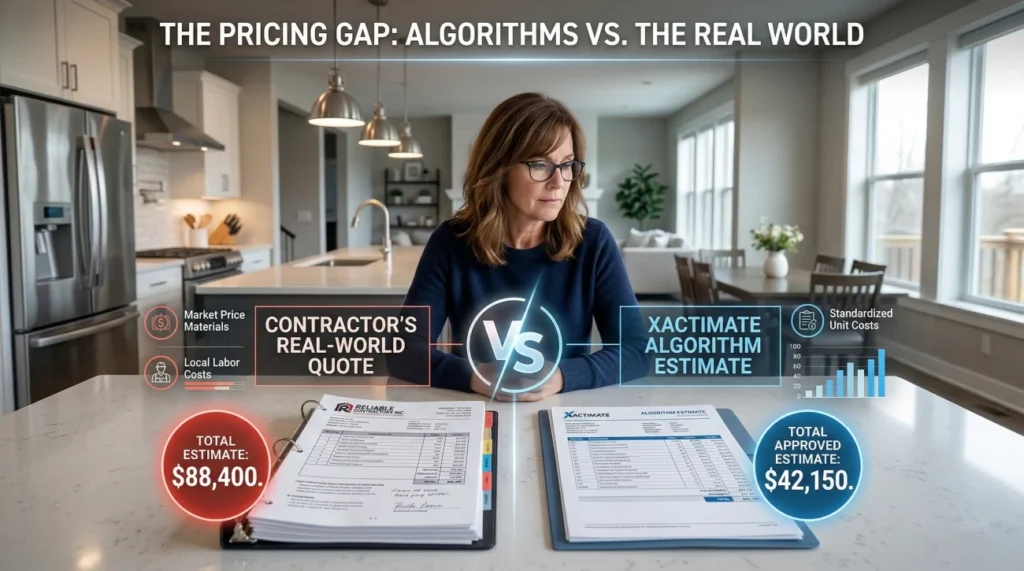

- Your insurance settlement is often lower than your contractor’s quote because adjusters use a pricing software called Xactimate, which relies on regional database averages rather than real-time local market rates.

- During periods of inflation or high demand, Xactimate’s database significantly lags behind what local contractors actually charge for labor and materials.

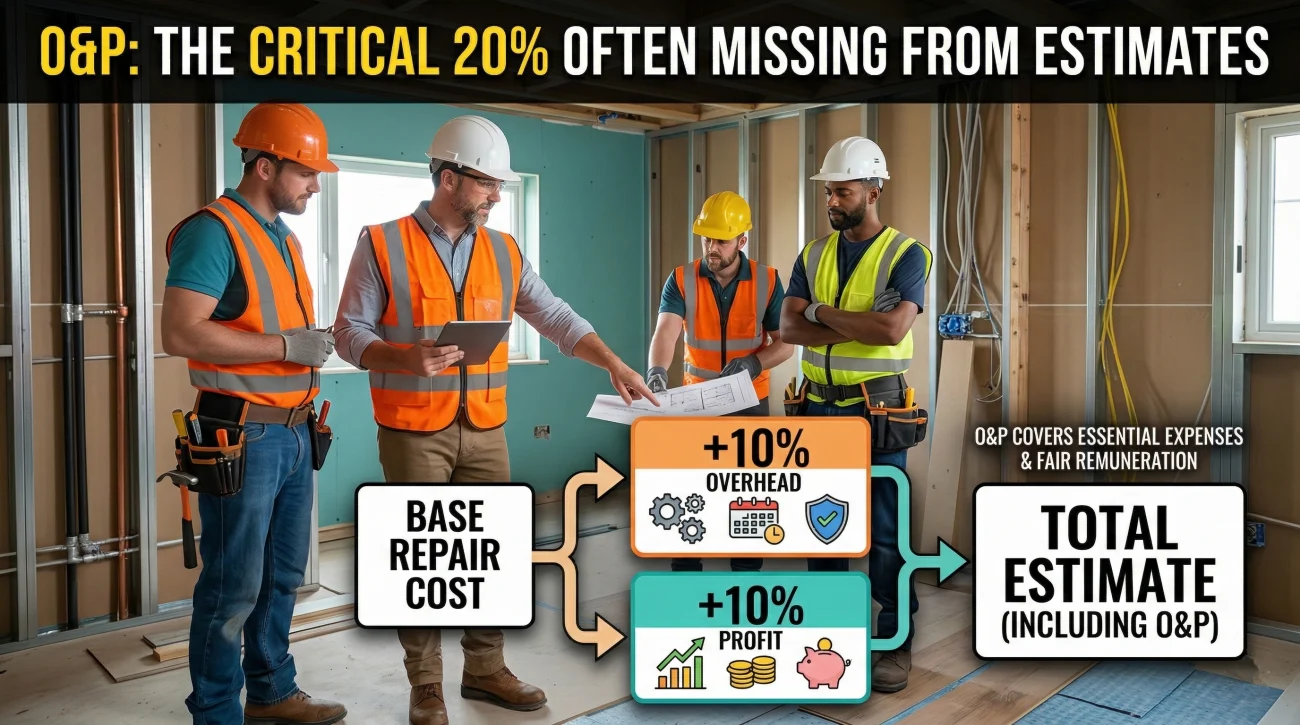

- A major source of the discrepancy is the frequent exclusion of General Contractor Overhead and Profit (O&P), a standard 20% charge that adjusters often remove from estimates even when multi-trade coordination is required.

- Supplements and the Appraisal Clause are your two primary tools to formally challenge an underpaid estimate and force a real-world market valuation.

The Shock of the First Settlement Offer

I have sat at hundreds of kitchen tables across from homeowners who are staring at two pieces of paper. In one hand, they hold a detailed repair quote from a reputable, local general contractor. In the other hand, they hold the settlement estimate from their insurance company. Almost inevitably, the homeowner looks up at me with the exact same question: Why is the insurance estimate so much lower than my contractor’s quote?

Often, the gap isn’t just a few hundred dollars. We are regularly talking about discrepancies of 20%, 30%, or even 50%. The immediate reaction from the homeowner is usually anger, followed quickly by the assumption that the insurance company is intentionally trying to scam them. While I completely understand that frustration, the reality of why insurance estimate lower than contractor quotes is usually less about a personal vendetta against your claim, and more about a systemic, structural pricing tool.

That tool has a name. It is called Xactimate. If you want to understand why your settlement is falling short, and more importantly, how to fight back and bridge that gap, you have to understand the software that generated your insurance adjuster’s numbers.

“When you are arguing with an insurance desk adjuster over the cost of drywall or roofing shingles, you usually aren’t arguing with a construction expert. You are arguing with a software algorithm that tells the adjuster what things ‘should’ cost.”

What Exactly is Xactimate?

Xactimate is the dominant claims estimating software used by the vast majority of major property insurance companies in the United States. It is developed and owned by a data analytics company called Verisk. When a field adjuster walks through your damaged living room, they take measurements, snap photos, and write down notes. But they do not sit down and call local suppliers to see what a sheet of plywood costs today.

Instead, they plug your room dimensions and the required repair tasks into Xactimate. The software then generates a line-by-line breakdown of the repair costs. It calculates everything: how many hours of labor it takes to paint a square foot of wall, the cost of the baseboards, the price of the nails, and the regional tax rates.

In theory, this creates standardization. It prevents an adjuster from arbitrarily deciding that a roof costs $2,000 when it should cost $15,000. However, the system has a fatal flaw when it comes to keeping up with reality: it relies on a database of historical averages, not real-time local market quotes.

Warning: The insurance company will present the Xactimate estimate to you as if it is an objective, undeniable fact. It is not. It is simply the insurance company’s opening bid based on a standardized software platform.

The Pricing Gap: Why the Database Fails the Real World

The primary reason Xactimate numbers fail to match your contractor’s quote is the fundamental difference between historical data and present-day reality. Xactimate updates its pricing lists periodically (usually monthly), relying on surveys and aggregated data to determine the “going rate” for a plumber or a framer in your specific zip code.

But local construction markets do not move in neat, predictable monthly averages. If a severe storm hits your county, the local demand for roofers skyrockets instantly. Contractors raise their rates due to high demand and supply chain shortages. A local contractor’s quote reflects the reality of what it costs to buy materials today and hire labor today. Xactimate’s database reflects what things cost weeks or months ago, averaged out over a broad geographic area.

This lag becomes disastrous for homeowners during periods of inflation. Over the past few years, the gap has widened significantly. In fact, Verisk’s own research (yes, the parent company of Xactimate) reported that structural replacement costs rose nearly 30% over a five-year period. Furthermore, data from the Insurance Research Council confirms that rising homeowners insurance claim costs continue to outpace general economic inflation.

This creates an incredible irony: the company that owns the software dictating your lower settlement payout is the exact same company publishing data showing that construction costs have exploded. The software simply struggles to keep up with the volatility of the real-world market.

When Xactimate Gets It Right (and When It Fails Miserably)

It is important to understand that Xactimate is not inherently evil; it is just a tool. In a stable economy, for a standard claim, like a single room of carpet replacement or a basic wind-damaged fence, the software’s pricing is often reasonably close to local market averages. If you have a simple, straight-forward claim with no structural damage, Xactimate might actually get it right.

Where the software fails miserably is during times of high volatility or complexity. If you are dealing with a post-catastrophe environment (where every roofer in the state is booked out for six months), high inflation markets, or labor-intensive repairs that require specialized craftsmanship, Xactimate will almost always drastically underestimate the true cost. Understanding this helps you assess whether your claim is genuinely worth fighting or if the carrier’s numbers are actually fair for a minor fix.

The “Minimum Trip Charge” Disconnect

Beyond broad inflation, there is a practical, micro-level reason the software fails. Xactimate loves to calculate materials and labor down to the decimal point based on volume. If you have a small leak that damages a three-foot section of drywall, Xactimate will calculate the precise cost of three square feet of drywall, a fraction of a bucket of mud, and 45 minutes of a drywaller’s hourly rate. The software might output a repair cost of $85.

I constantly review estimates where the software allocates $85 to patch drywall. But try calling a professional drywall contractor to drive their truck to your house, set up their equipment, do the patch, wait for it to dry, sand it, and clean up for $85. They will laugh and hang up the phone.

Real-world contractors have minimum trip charges. A reputable professional might not take any job for less than $350 or $500, simply because it isn’t worth their time to dispatch a crew otherwise. Xactimate, when used rigidly by an inexperienced desk adjuster, often completely ignores these practical minimums, leaving the homeowner to pay the difference out of pocket.

The Missing 20%: The Overhead and Profit Dispute

If you are looking at your estimate and noticing a massive, glaring gap, you need to check for the presence of three letters: O&P. This stands for Overhead and Profit.

When you hire a General Contractor (GC) to manage a complex repair, they do not just charge you for the raw materials and the hourly wages of the workers. They charge “Overhead” (the cost of running their business, insurance, trucks, office staff) and “Profit” (the margin that allows their business to survive). The industry standard for this is typically 10% for Overhead and 10% for Profit, known in the claims world as “10 and 10.”

Insurance companies frequently and systematically strip this 20% right off the top of the Xactimate estimate. The carrier’s justification is usually that your specific claim is “too simple” to require a General Contractor to coordinate the trades. Therefore, they argue, they only owe you the raw cost of the individual workers.

“This is just a kitchen leak. You just need someone to fix the pipe, replace the floor, and paint the wall. You don’t need a General Contractor, so we are omitting O&P.”

You need a licensed plumber, a specialized flooring installer, a drywall hanger, and a painter. Finding, vetting, scheduling, and coordinating four different specialized trades in sequence is the exact definition of acting as a General Contractor. Therefore, O&P is warranted.

In many cases I’ve reviewed, simply successfully arguing that the complexity of the job warrants the inclusion of O&P instantly bridges a massive portion of the gap between the insurance estimate and the contractor’s quote.

Signs Your Settlement is Trapped in the Xactimate Gap

Before you accept defeat and either take out a loan or hire a cheaper, unvetted handyman to make the insurance money stretch, you need to verify if the low offer is structural. Look for these tell-tale signs that your claim is suffering from a systemic Xactimate gap:

- 📍 The insurance company agreed that all the damage was covered, but their total is still 20% to 30% lower than your lowest local bid.

- 📍 The estimate uses unit prices that local professionals flatly tell you are impossible to meet in the current market.

- 📍 The O&P (Overhead and Profit) line items are completely absent from the final summary page, despite multiple trades being involved.

- 📍 The estimate fails to account for necessary building code upgrades required by your local municipality.

If you are staring at a massive discrepancy and feel completely stuck, you do not have to fight the algorithm alone. Assessing whether the gap is worth a professional second opinion is a critical step. Often, having a public adjuster review the scope before you accept can help identify exactly which Xactimate line items were manipulated or omitted, leveling the playing field against the carrier’s software.

Another Gap Factor: Actual Cash Value vs. Replacement Cost

Even if you successfully argue the Xactimate pricing, there is another reason your initial check might induce panic: Depreciation. If you have a Replacement Cost Value (RCV) policy, your insurance carrier owes you the cost to buy new materials at today’s prices. However, they do not pay it all upfront.

The first check you receive is almost always for the Actual Cash Value (ACV). The adjuster’s software automatically calculates the lifespan of your damaged property and deducts value for its age. For example, if your 10-year-old roof was destroyed, the initial estimate will show the full replacement cost, minus 10 years of depreciation, leaving you with a surprisingly small ACV check. This is standard procedure. You must actually complete the repairs and submit the final contractor invoices to “unlock” those withheld funds (known as Recoverable Depreciation). This applies if your policy is a Replacement Cost Value policy. Check your declarations page to confirm which type you have (if you carry an ACV-only policy, there is no depreciation to recover).

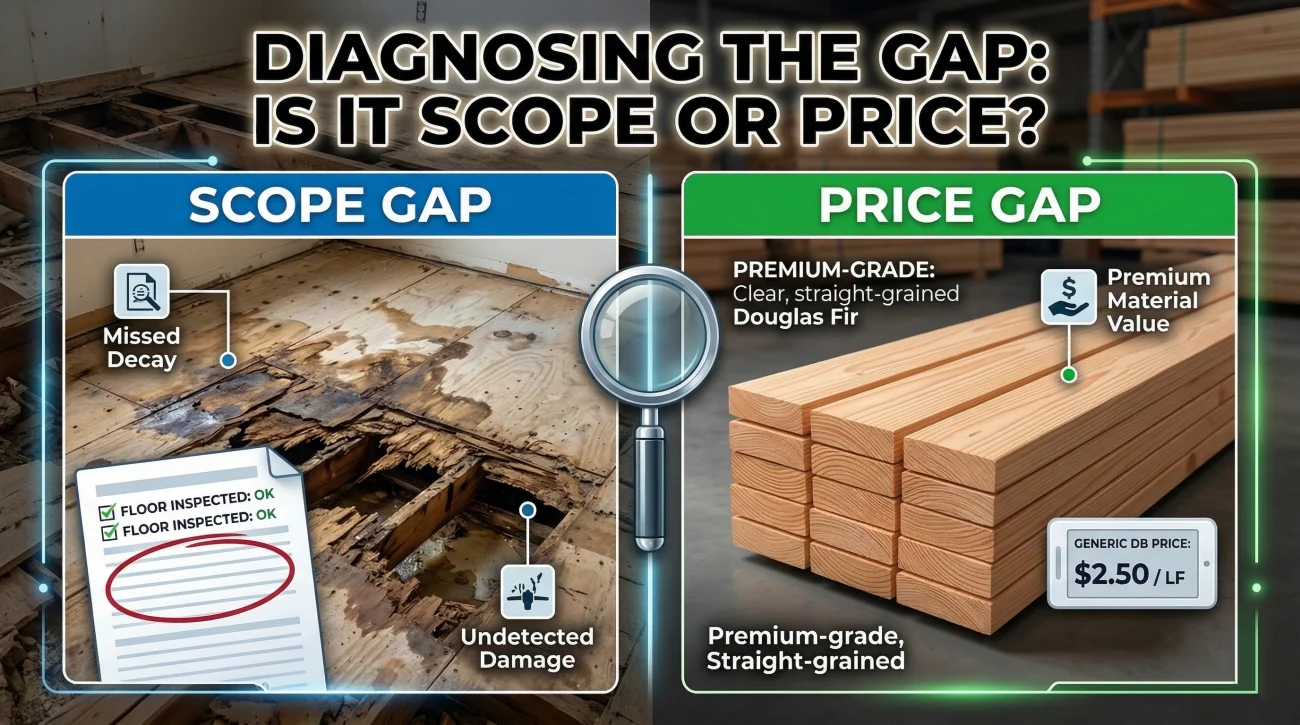

Scope vs. Price: Diagnosing the Shortfall

To successfully fight an underpaid estimate, you must first diagnose exactly *why* the number is low. In the claims industry, the gap between what you need and what they offered always falls into one of two categories: a Scope Gap or a Price Gap. Sometimes, it’s a combination of both.

| The Scope Gap | The Price Gap |

|---|---|

| The adjuster completely missed or omitted necessary repair items (e.g., they paid to replace the carpet, but ignored the water-damaged subfloor underneath). | The adjuster included the correct item, but the software assigned an artificially low dollar value to it (e.g., they paid for the subfloor, but allocated only $1.10 per square foot when the local rate is $2.50). |

| The Fix: Provide photographic evidence, contractor statements, and building code documentation proving the item physically exists and must be repaired. | The Fix: Provide localized bids, material invoices, and independent estimates proving that the Xactimate unit price is not viable in your current market. |

Understanding this distinction is vital. If you yell at an adjuster because the overall price is too low, you won’t get far. But if you can explicitly state, “Your estimate fails to include line items for debris removal and baseboard sealing (Scope), and your unit price for roofing felt is 40% below current supplier invoices (Price),” you force them to address the specific mechanics of the software.

How to Bridge the Gap: The Supplement Process

The most important thing I can tell you is this: the initial estimate is not the final word. It is simply the opening of the negotiation. The mechanism to correct an inaccurate Xactimate estimate is called a “Supplement.”

A supplement is a formal request asking the insurance company to add additional funds to the claim to cover items that were either omitted from the original scope or underpriced by the software. Your contractor will usually be the one to draft the supplement, but you, the homeowner, must drive the communication.

Identify the specific missing line item + Provide local contractor bid/invoice as proof + Request a revised estimate in writing

When you submit a supplement, you cannot simply say, “My guy costs more.” You must speak the language of the system. Here is a generic, copy-paste safe framework you can use when emailing your desk adjuster to initiate a supplement conversation:

Subject: Supplement Request – Claim #[Your Claim Number] – Inadequate Estimate Pricing

Hello [Adjuster Name],

I have received the initial repair estimate generated by your office for my property. After reviewing this document with my licensed general contractor, it is clear that the provided estimate does not reflect the actual local market costs to return my home to its pre-loss condition.

Specifically, the estimate omits General Contractor Overhead and Profit, despite this repair requiring the coordination of [Trade 1, e.g., plumbing], [Trade 2, e.g., drywall], and [Trade 3, e.g., flooring]. Furthermore, the unit pricing allocated for [Specific Material, e.g., lumber/roofing] falls significantly below current local supplier rates.

Attached please find the detailed, itemized quote from my contractor, along with material invoices proving current market rates. Please review these documents and issue a revised, supplemental estimate that reflects the actual cost of repairs. Let me know when this has been processed.

Sincerely,

[Your Name]

💡 Pro Tip: Build a Supplement Tracking System. Do not just send an email and wait. Keep a rigorous log of when you submit supplement requests. Create a simple folder or spreadsheet: log the date you submitted the supplement, the specific line items requested, the version number of the insurance estimate (e.g., “Estimate v1,” “Estimate v2”), and the date of every follow-up. According to J.D. Power’s 2024 Property Claims Satisfaction Study, resources have become severely strained for both insurers and contractors, extending average claim cycle times. Following up in writing every 3 to 5 business days prevents your supplement from being ignored in a busy adjuster’s inbox.

Navigating the Next Steps: The Appraisal Clause

If the insurance company stubbornly refuses to update their Xactimate pricing even after you have provided overwhelming proof of local market costs, exchanging endless emails with a desk adjuster becomes a waste of time. You need a mechanism that shifts the power away from the carrier’s software.

At this stage, homeowners typically invoke the Appraisal Clause found in most standard homeowner policies. This is a binding dispute resolution process designed exactly for this situation: a disagreement over the cost of repairs. When you invoke Appraisal, both you and the insurance company hire independent appraisers to evaluate the damage and determine the true cost of repair. If the two appraisers cannot agree, an impartial umpire makes the final decision.

Why is this so powerful? Because it takes the claim out of the hands of the desk adjuster and their rigid adherence to Xactimate. Independent appraisers evaluate real-world, localized costs rather than relying solely on a lagging database. The gap between what you expected and what you received is structural, but it is entirely challengeable. If you are currently looking at a settlement that won’t even cover the cost of materials, you need a specific strategy. For a deeper dive into exactly how to respond, read our comprehensive guide on what to do when your home insurance estimate is too low.

Final

The most dangerous thing you can do during a property claim is assume the insurance adjuster’s estimate is a meticulously researched, highly accurate reflection of your specific home. It isn’t. It is a mass-produced output from a software database designed for averages, not exceptions. When you start treating Xactimate as an opening algorithmic bid rather than a final verdict, your entire strategy changes. You stop arguing about fairness and start arguing about line items, local market data, and documented scope. Stay calm, document everything meticulously, and remember: the database does not rebuild your house, real contractors do, and your settlement must reflect the reality of those costs.

📚 Data and Sources

The industry trends and statistical data referenced in this article regarding construction inflation, pricing gaps, and claim cycle times are sourced from the following independent reports and industry monitors:

- Triple-I / Verisk Analytics (2025): Data regarding the nearly 30% rise in structural replacement costs over a five-year period. Available via the Insurance Information Institute Press Release.

- Insurance Research Council (IRC): Research documenting that homeowners insurance claim costs continue to outpace general inflation. Available via IRC News Releases.

- J.D. Power (2024): U.S. Property Claims Satisfaction Study detailing strained resources, extended claim cycle times, and the resulting impact on homeowner satisfaction. Available via J.D. Power Press Releases.

❓ FAQ

📉 Why is the insurance check so much lower than my roofing quote?

Insurance companies use pricing software that relies on historical regional averages. If there has been a recent storm or sudden inflation, local roofers will charge higher real-time rates, creating a gap between the software’s estimate and actual market costs.

🛠️ Do I have to use a contractor that accepts Xactimate prices?

No. In most standard policies, you have the right to choose your own contractor. You are not obligated to use the insurance company’s “preferred vendor” just because they agree to work for the lower software pricing.

🛑 What happens if my contractor refuses the insurance estimate?

This is very common. Your contractor should provide a detailed, itemized quote outlining exactly why the insurance estimate is insufficient. You will use this quote to file a “supplement” requesting additional funds from the carrier.

⏱️ How often are Xactimate prices updated?

The software typically releases updated price lists on a monthly basis. However, in highly volatile markets or post-catastrophe environments, even a one-month lag can result in estimates that are thousands of dollars below reality.

📄 Can I ask the insurance company to see their Xactimate breakdown?

Yes, absolutely. You should always request the full, line-by-line itemized estimate, not just the summary page. You need the itemized list to see exactly which materials and labor rates they are underpaying.

💼 What does O&P mean on an insurance estimate?

O&P stands for Overhead and Profit. It is a standard industry charge (usually 20% total) applied by General Contractors to cover the costs of managing the business and coordinating multiple trades on a complex repair job.

⚖️ Is the insurance company allowed to dictate how much a contractor charges?

No. The insurance company only determines what they believe the “fair market value” of the repair is based on their software. They cannot force an independent contractor to lower their rates to match that software.

📸 How do I prove the insurance estimate is too low?

You prove it by submitting written, itemized bids from licensed local contractors, along with actual material invoices from local supply houses, demonstrating that the repair cannot be completed for the price the software generated.

🚫 Will my insurance drop me if I fight their repair estimate?

Disputing an estimate through the proper supplemental or appraisal process is a standard part of resolving a claim. While carriers can non-renew policies for various risk-based reasons, simply asking for a fair market settlement based on documentation is a normal operational procedure.

🤝 Can I hire a public adjuster just to dispute the Xactimate pricing?

Yes. Many homeowners hire public adjusters specifically because these professionals use the same software and know exactly how to document the scope and price gaps to negotiate a settlement that reflects actual market costs.

From filing to final payment: the parts most homeowners do not learn until something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the most common situations where a second opinion changes the result.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.