- The national average for home insurance claims closed without payment has risen to 37 percent, according to recent industry data analysis.

- Not all “denials” mean bad faith; this statistic includes legitimate exclusions, claims withdrawn by the homeowner, and damage that falls below the policy deductible.

- The time it takes to process a claim is extending, leading to heavy homeowner frustration and a higher likelihood of abandoning valid claims.

- Understanding the data allows you to shift your strategy from blindly trusting the process to actively documenting your damage before the adjuster arrives.

The New Statistical Reality of Property Claims

When I sit across the kitchen table from a family holding a denial letter, the first thing I usually hear is a variation of the same question: “Why is this happening to us? We have paid our premiums for fifteen years.” There is a deep, isolating feeling that comes with a rejected claim. You feel like you are the unlucky exception to the rule. But when we look at the home insurance claim denial rates statistics, a much different, much colder picture emerges.

You are not the exception. The environment has fundamentally shifted. According to NAIC data analyzed by Weiss Ratings, the national average home insurance claim denial rate currently sits at 37 percent. To put that in perspective, about two decades ago, that number hovered around 25 percent. If you are filing a claim today, you are walking into an industry posture that is significantly tighter, more heavily scrutinized, and statistically more likely to end without a settlement check than at any point in recent memory.

I got my public adjuster license in 2019, which means I entered this industry just as these trends began to rapidly accelerate. I did not work claims back in 2004, but every veteran adjuster I speak with confirms the same thing: the days of a friendly field adjuster writing a check on the spot for a borderline claim are largely gone. Today, claims are driven by algorithms, strict policy interpretations, and a heavy burden of proof placed directly on the homeowner.

However, before we draw conclusions or assume the entire system is broken, we need to look at what these numbers actually mean. Data without context creates panic, and panic leads to poor decisions when you are trying to rebuild your home.

Decoding “Closed Without Payment”

When you see headlines asking what percentage of home insurance claims are denied, the statistics cited are usually based on a metric called “claims closed without payment.” This is a crucial distinction. Not every claim closed without a check is an unfair denial. In fact, many of them are completely legitimate under the terms of the contract.

If we want to be honest about the data, we have to look at what is baked into that overall figure. It is a catch-all category that includes several different scenarios.

Below-Deductible Claims

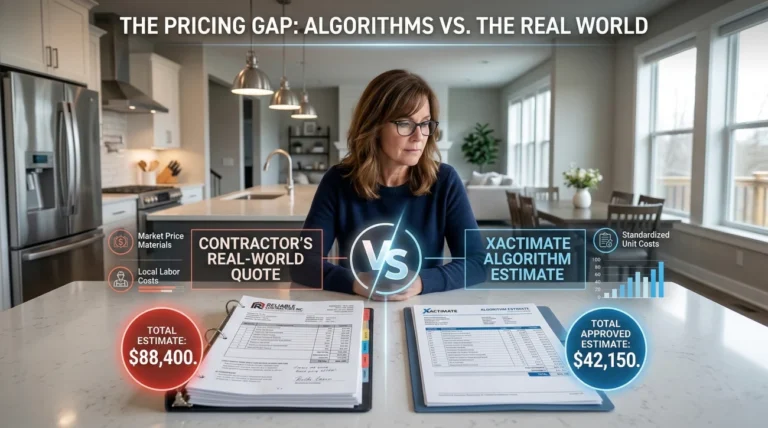

This is arguably the most common reason a claim is closed without payment, and it is entirely preventable. Many homeowners do not fully understand how their deductible works. If a windstorm blows off a section of your shingles, and a contractor quotes you $1,500 for the repair, but your policy carries a $2,500 deductible, the insurance company will process the claim, agree that the damage is covered, and then close it without payment because the repair cost does not exceed your financial responsibility.

I constantly see homeowners file claims before knowing their deductible. They end up with a zero-dollar payout and a claim recorded on their CLUE report, which can impact their future rates. Always know your numbers before you pick up the phone.

Legitimate Policy Exclusions

Standard homeowners insurance policies (typically HO-3 forms) do not cover everything. The most glaring example is flood damage caused by rising exterior water, such as storm surge or an overflowing river. Earth movement, such as sinkholes or landslides, is also typically excluded unless you have specific endorsements. When a homeowner files a claim for groundwater flooding under a standard policy, the carrier will deny it correctly based on the policy language.

Withdrawn Claims

Sometimes, a homeowner files a claim, realizes the damage is minor, and decides they would rather pay out of pocket than risk a premium increase. They call the carrier and withdraw the claim. In the aggregate data, this often gets logged as closed without payment.

While these categories explain a portion of the data, they do not account for the entire spike. To understand the real risk facing a valid claim today, we have to look closely at the behavior of the largest players in the market.

The Trend Line Among Major Carriers

The national average gives us a broad view, but the home insurance denial statistics 2024 reveal an even starker reality when we zoom in. The Weiss Ratings analysis of NAIC data found that among the 13 largest homeowners insurers in the country in 2023, the rate of claims closed without payment reached 47.5 percent.

If you are insured by one of the largest carriers in the United States, nearly half of the claims processed end up with zero dollars paid to the policyholder. This is the environment I work in every day. When I prepare a claim file for a client, I am fully aware that we are walking into a system where a rejection is almost as likely as a settlement check.

This 47.5 percent data point is critical for homeowners because it should fundamentally change your expectations. You are no longer dealing with a system designed to look for ways to pay you; you are dealing with a system heavily optimized for risk mitigation.

Warning: Assuming your carrier will automatically find coverage for your damage is the most dangerous mindset you can have. The data shows that major carriers are actively looking for the boundaries of your policy limits.

Company-Level Variation

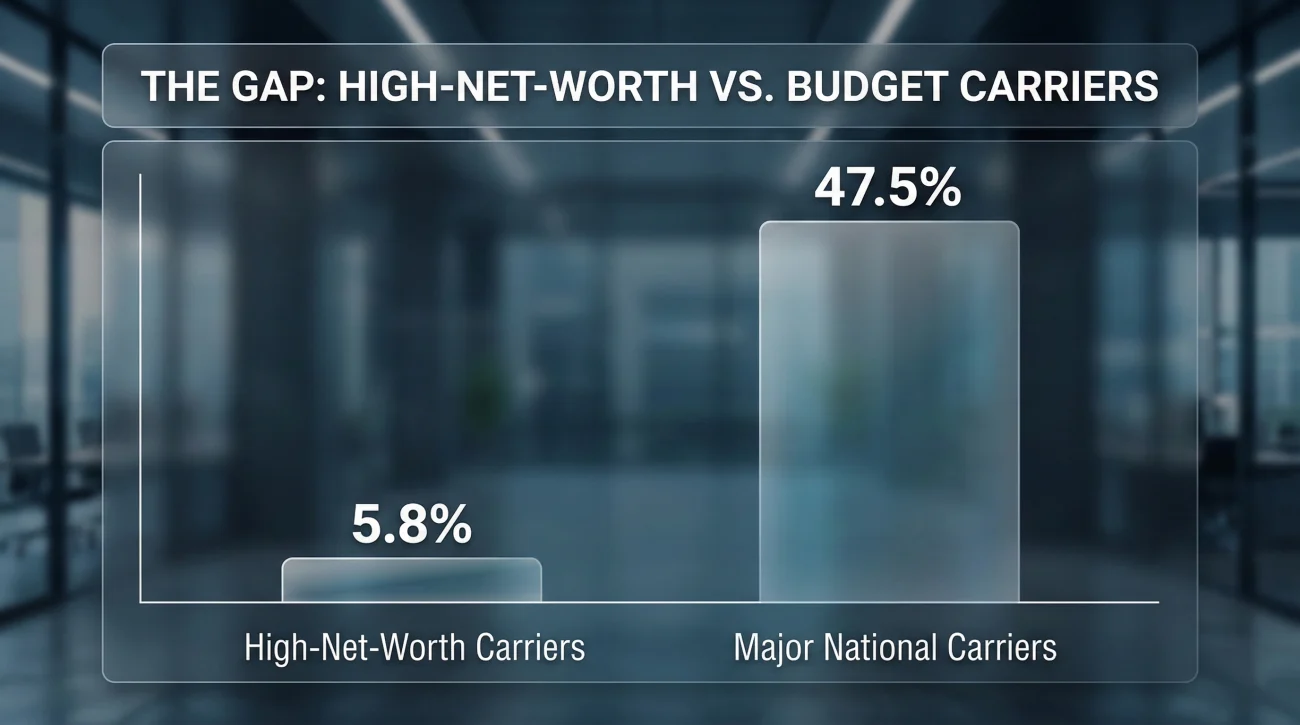

One of the most revealing aspects of the recent data is the massive variance in the home insurance denial rate by company. Not all insurers treat claims the same way, and their internal metrics reflect their different business models, target demographics, and underwriting standards.

According to the Weiss study, some carriers maintain incredibly low rates of claims closed without payment. For example, Chubb was reported at 5.8 percent, Auto-Owners at 15.9 percent, and Nationwide at 16.6 percent. Conversely, other major carriers in the same study closed more than 50 percent of their claims without a payout.

Why does this gap exist? It often comes down to the type of policies written and the underwriting process upfront. High-net-worth carriers like Chubb often require extensive home inspections before writing a policy, meaning they know exactly what they are insuring. Their policies frequently lack the strict depreciation schedules and aggressive exclusions found in more budget-friendly policies.

Before purchasing a policy or filing a marginal claim, you can actually check your carrier’s track record. The NAIC maintains a public consumer complaint database where you can look up your specific insurance company and see how their complaint index compares to the national average. Doing this quick research turns a blind leap of faith into a calculated decision.

The Catastrophe Effect

If we want to be completely fair to the data, we must address the catastrophe effect. Insurers with heavy concentrations of policies in disaster-prone areas like Florida, Louisiana, or California often show inflated denial rates. This is not necessarily proof of bad faith; it is often a reflection of the types of damage occurring.

Consider a major hurricane hitting a coastal town. The storm brings 120 mph winds and a 10-foot storm surge. The wind damage is covered by standard home insurance, but the storm surge is not. A homeowner whose house is destroyed might file a claim with their primary carrier, hoping for help. The carrier sends an adjuster, determines the damage was caused entirely by rising water, and denies the claim. The homeowner must then turn to their National Flood Insurance Program (NFIP) policy.

In the NAIC data, that initial claim is logged as closed without payment. In years with massive coastal flooding, this specific scenario skews the data significantly higher.

For coastal homeowners, knowing how to distinguish the entry point of the water is critical before making that first phone call. If water entered because high winds ripped off your shingles and allowed rain to pour through the ceiling, that is a windstorm claim. If the water rose from the street and entered under your front door, that is a flood claim. Mixing up these terms on a recorded line can derail a valid claim from day one.

Calling the 1-800 number immediately after a hurricane to say your house is flooded, without checking if you actually have flood insurance or if the water came through a wind-damaged roof.

Having a qualified contractor or professional assess whether the water intrusion was caused by a wind-created opening (covered) or rising groundwater (excluded) before filing the specific claim.

The 20-Year Economic Context

Homeowners often ask me, “Are insurance companies denying more claims just to boost their profits?” The answer requires looking at the broader economic picture. According to research from the Insurance Research Council (IRC), the cost of homeowners insurance claims has been rising faster than the rate of general inflation for over two decades.

The severity of claims has skyrocketed. According to data from the Insurance Information Institute (III) covering 2019 to 2023, the average claim severity for fire and lightning damage reached an astonishing $88,170. When you combine the rising costs of construction materials, severe labor shortages in the skilled trades, and the increasing frequency of billion-dollar weather events, the financial pressure on the insurance industry is immense.

Insurance companies are not charities; they are highly regulated financial institutions. When their payout severity increases dramatically, their defense mechanisms engage. They tighten underwriting guidelines, add new exclusions for roofs over 15 years old, implement mandatory cosmetic damage waivers, and scrutinize every single estimate submitted by a contractor. The rising denial rate is a direct symptom of this economic pressure.

The Exhaustion Metric: What the Numbers Feel Like

While the data explains the economic pressure on insurance companies, it does not capture what it actually feels like for a homeowner caught in the gears of a stalling claim. The reality of a rising denial rate is not just that more claims get rejected; it is that the process of getting to a decision has become a grueling marathon.

The 2024 U.S. Property Claims Satisfaction Study by J.D. Power highlights this perfectly. They found that overall customer satisfaction has dropped to its lowest level in seven years. A massive driver of this dissatisfaction is time. The average claims cycle has extended to 23.9 days. Furthermore, the study notes that when a claim drags on past 31 days, customer satisfaction scores plummet.

I see the human cost of this delay constantly. A family with a kitchen destroyed by a burst pipe is asked to submit photos. A week later, a desk adjuster asks for a plumber’s cause-of-loss report. Another week passes, and a different adjuster takes over the file, asking for the original purchase receipts for the cabinets.

By this point, the family is cooking on a hotplate in the living room, completely exhausted by the administrative burden. Eventually, they get a letter stating the claim is denied due to “long-term seepage”, a decision made by an adjuster who never stepped foot on the property.

The system often feels designed to wear you down. Homeowners give up on valid claims not because they lack coverage, but because they run out of energy and resources to keep fighting. If you are trapped in this cycle of endless requests and shifting explanations, getting a free claim review from a licensed public adjuster who knows how to break the stall tactics is often the smartest next step. You need someone who speaks the language of the policy to step in before you abandon a legitimate payout.

What These Statistics Mean for Your Strategy

Knowing that the odds have shifted is only useful if you change how you play the game. If you are filing a claim today, you must assume from the very first phone call that your file is being evaluated for potential denial.

Part of this strategy is knowing when not to file. If a contractor estimates your repair at $1,200 and your deductible is $1,000, do not file the claim. You will receive no money, but the claim will sit on your CLUE report and potentially raise your future premiums. Only file when the damage significantly exceeds your deductible.

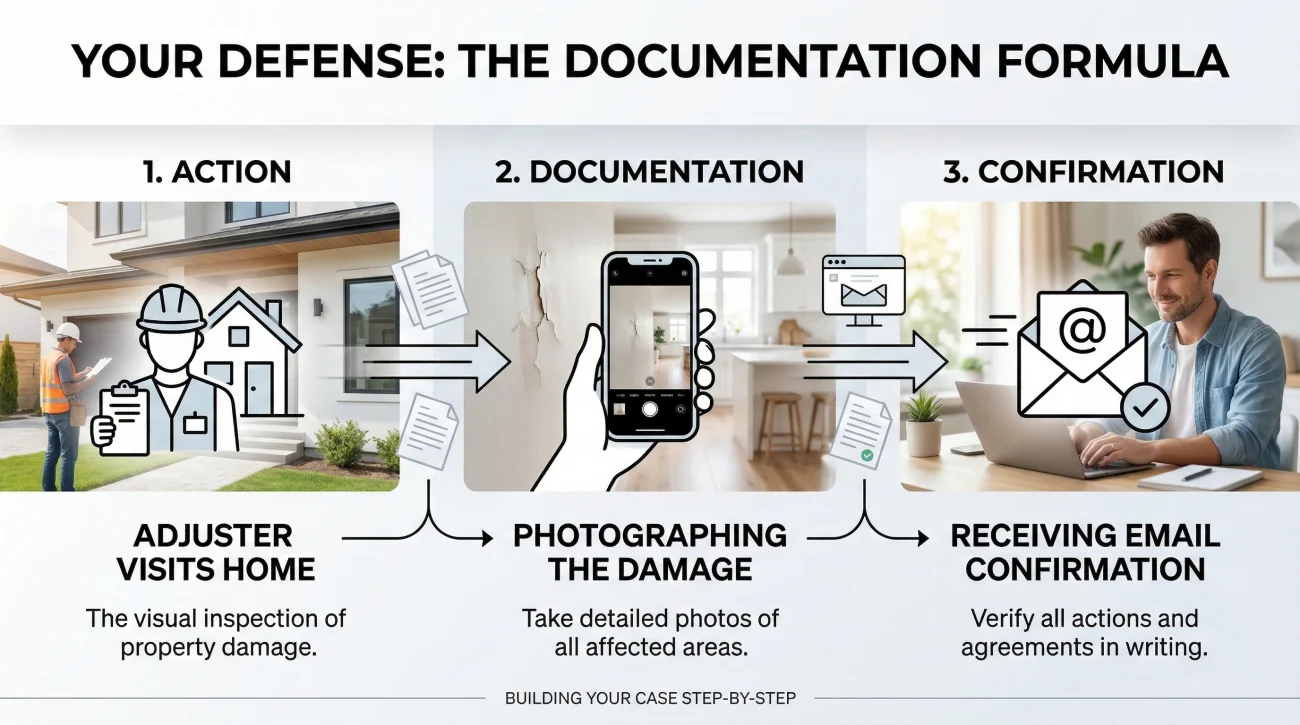

When you do file, the burden of proof rests entirely on your shoulders. Your documentation discipline must be flawless. You cannot rely on the insurance company’s field adjuster to find and document all your damage. They are carrying heavy caseloads and are tasked with reporting the visible scope, not looking for hidden moisture behind your baseboards.

This is exactly why documentation is your only real defense. I saw this play out last spring with a roof claim. A severe hail storm rolled through a neighborhood, but a homeowner’s claim was rapidly denied for “wear and tear and thermal blistering.” The carrier’s denial leaned entirely on vague language that most homeowners would not know how to challenge. It was not until we stepped in, pulled the historical weather data, and submitted photos of the physical hail spatter on the soft metals that the carrier reversed the denial and paid for a full roof replacement.

I advise every homeowner to adopt a strict habit of creating a paper trail. Use this simple formula for every interaction:

[Action Taken] + [What was discussed or documented] + [Written Confirmation sent to the adjuster]

If an adjuster visits your property and verbally tells you the roof is totaled, do not celebrate until it is in writing. Send an email that same day:

Subject: Confirmation of site visit – Claim #123456

Hello [Adjuster Name],

Thank you for coming out today. As we discussed on site, you observed severe wind tearing on the western slope and indicated the damage warrants a full replacement. Please let me know when I should expect the official estimate.

If they later try to deny the claim for wear and tear, you have contemporaneous written documentation of their initial field assessment.

Most importantly, before you even think about accepting a rejection letter as the final word, you need to understand exactly what a denial looks like and how to challenge it by understanding the rules on our guide to navigating a denied home insurance claim. The statistics show they will try to close the file; your job is to know when to pry it back open.

Final Thoughts

The home insurance claim denial rates statistics can look incredibly intimidating. Seeing that nearly half of claims at major carriers might close without payment is enough to make anyone second-guess paying their premiums. However, data is just a reflection of the landscape. It is not a prediction of your specific outcome.

The environment has permanently changed, but your policy is still an enforceable contract. If you have sudden, accidental damage that falls within the four corners of your policy language, you are entitled to a settlement. By understanding the data, knowing your deductibles, and documenting your damage with clinical precision, you protect yourself from becoming just another negative statistic in next year’s industry report.

📚 Sources

- National Association of Insurance Commissioners (NAIC) data via Weiss Ratings, reported by National Mortgage News (September 2024): 13 largest homeowners insurers denied nearly half of claims last year.

- Insurance Information Institute (III), Facts + Statistics: Homeowners and renters insurance (2023 claim frequency and severity data): III Facts & Statistics.

- J.D. Power 2024 U.S. Property Claims Satisfaction Study: Claims satisfaction study and timeline data.

- Insurance Research Council (IRC), research on rising claim costs outpacing inflation: IRC Research Reports.

❓ FAQ

📞 Is it normal for an insurance company to deny a claim right away?

If your claim clearly falls under a standard exclusion (like flood water on a standard HO-3 policy) or the damage is visibly less than your deductible, insurers can and often will close the claim rapidly over the phone or after a very brief initial review.

📈 Will my insurance rates go up if they close my claim without paying?

In many cases, yes. Simply filing the claim puts a zero-dollar loss on your C.L.U.E. (Comprehensive Loss Underwriting Exchange) report. Some carriers remove claim-free discounts or raise rates based on claim frequency, regardless of whether they actually paid out a settlement.

⚖️ Can I appeal if my claim falls into that 37 percent denial statistic?

Yes. A denial letter is the insurance company’s position, not a court order. You have the right to request a reinspection, submit new evidence from a contractor, or invoke the appraisal clause if the dispute is over the scope of the damage.

🌧️ Why did they deny my roof claim after a major storm?

Adjusters frequently deny roof claims by categorizing the damage as long-term wear and tear, thermal blistering, or poor initial installation rather than sudden storm damage. Proving the damage was sudden and accidental is often the hardest part of a roof claim.

🔍 Does the company check my past claims before deciding to deny?

Absolutely. Adjusters pull your property’s claim history immediately. If they see you previously filed a claim for similar damage, or if you have a history of frequent small claims, your new file will face significantly tighter scrutiny.

🛑 How do I know if an adjuster’s denial is totally final?

A denial is rarely the end of the road. If you receive a denial letter, you must read the specific policy language they cite. If you can provide documentation showing their interpretation is incorrect, the claim can often be reopened.

💵 What happens if the repair cost is slightly less than my deductible?

The insurance company will acknowledge the damage but will close the file without issuing a check, as you must meet your financial deductible before their coverage kicks in. This is counted as a claim closed without payment in industry statistics.

🛡️ Can I hire someone to help me fight a closed claim?

Yes. You can hire a licensed public adjuster to review the denial, re-document the damage, and negotiate with the carrier on your behalf. They work for you, not the insurance company, and typically charge a percentage of the recovered settlement.

🏢 Do big insurance companies deny more claims than smaller regional ones?

According to recent data analysis, some of the largest national carriers do have higher rates of claims closed without payment compared to certain specialized or regional carriers, though rates vary wildly depending on the specific company’s underwriting standards.

⏳ How long do I have to fight a claim after they close it?

This depends entirely on your state laws and your specific policy language. You should carefully review your policy documents and consider contacting your state’s Department of Insurance to confirm the exact deadline. Do not assume you have unlimited time to reopen a closed file.

From filing to final payment: the parts most homeowners do not learn until something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the most common situations where a second opinion changes the result.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.